China's benchmark stainless steel futures surged to their highest level since 2023 in the final trading week before the May Day holiday, driven by a cluster of supply-side disruptions in key raw materials. But the rally has yet to find convincing support from physical demand, setting up a potentially volatile reopening.

The most-traded SHFE stainless steel contract (SS2606) closed at approximately $2,278/mt (RMB 15,585/mt) on April 30, gaining around $61/mt (RMB 420/mt) over the week. The move was fueled almost entirely by cost-push factors — sudden disruptions to scrap supply and a major nickel-cobalt producer's output cut — rather than any improvement in downstream consumption.

Macro backdrop: domestic strength, overseas caution

The macro environment offered a mixed picture. On the domestic side, China's National Bureau of Statistics reported that profits at large-scale industrial enterprises rose 15.5% year-on-year in the first quarter, reinforcing the narrative of a resilient manufacturing recovery. Tax revenue data from the Ministry of Finance echoed that tone.

Offshore, the picture was less supportive. The U.S. Federal Reserve held rates steady as expected, but hawkish dissent from three voting members — signaling resistance to near-term cuts — and ongoing geopolitical uncertainty weighed on the forward valuation of commodities broadly. For now, though, China's domestic supply-side story is overriding external headwinds.

Futures rally outpaces physical market

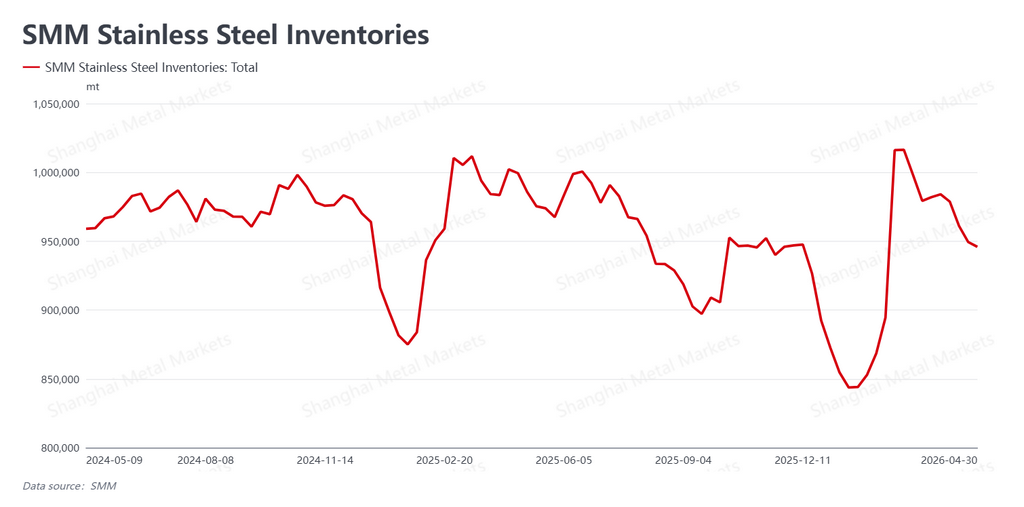

Despite the strong move on the futures board, the spot market told a more cautious story. According to SMM (Shanghai Metals Market), total market inventory edged down to 945,900 mt this week, a modest decline of 3,500 mt. Destocking continued, but at a sluggish pace.

More notably, physical transactions were weak. Futures prices ran ahead too quickly for spot to follow, and with the price gap widening, downstream buyers largely chose to sit on the sidelines. Apart from a brief burst of buying early in the week, transaction volumes faded. Processing operations — slitting, leveling, and other service centers — reported subdued business, with no sign of the pre-holiday restocking that typically characterizes late April. The spot liquidity that did exist was largely driven by basis-trade arbitrage rather than genuine end-user demand.

In short, futures have priced in a bullish raw material narrative that the physical market hasn't yet validated.

The real driver: raw material supply shocks

The week's price action was anchored by two developments on the cost side.

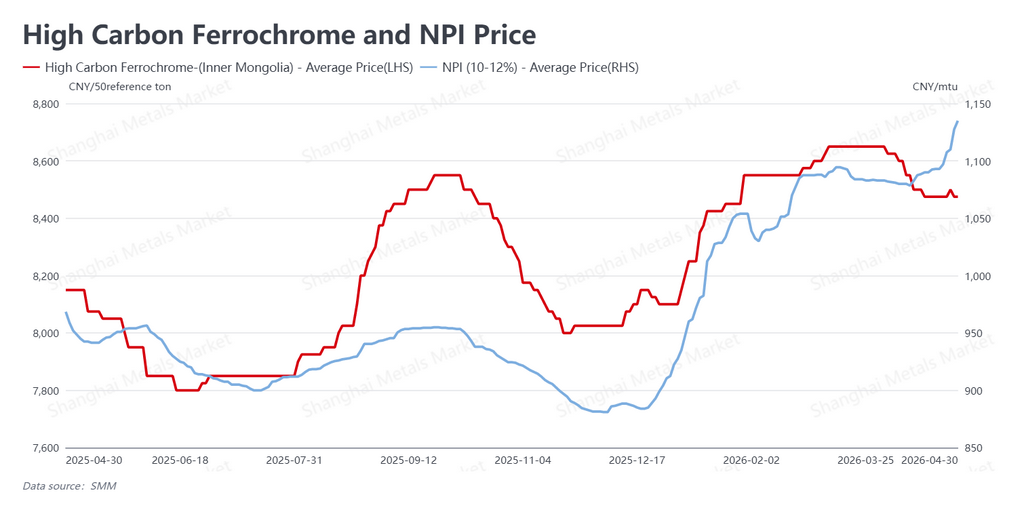

First, a deepening tightening in China's stainless steel scrap market. Stricter invoicing and tax compliance controls on scrap transactions are raising medium-to-long-term concerns about scrap availability, pushing Chinese mills to increase their reliance on Nickel Pig Iron (NPI) as a substitute feedstock.

Second — and more immediately impactful — a leading Chinese nickel-cobalt producer announced a temporary production halt on parts of its operations starting May 1, citing rising auxiliary material costs and the strain of sustained high utilization rates. The shutdown is expected to affect roughly 50% of the company's output. This sent a clear supply-contraction signal through the raw material complex.

In response, NPI offers rose to approximately $166 per nickel point (RMB 1,135/Ni point) over the week. High-carbon ferrochrome held steady at around $1,239 per 50 base tons (RMB 8,475/50 base tons). The upward shift in the cost floor gave the futures rally a fundamental anchor, even as spot demand lagged behind.

Outlook: cost expectations vs. demand reality

China's stainless steel market closed the traditionally strong "Silver April" on a firm note, buoyed by the convergence of scrap supply constraints and production curtailments at a major upstream player. Together, these factors have meaningfully lifted short-term cost expectations.

But the disconnect between elevated futures prices and tepid spot demand creates a tension that will need to resolve. As trading resumes after the May Day break, the market faces a straightforward test: can physical buyers absorb material at these higher price levels, or will the lack of downstream follow-through force a correction?

For industry participants, the key risk heading into May is elevated price volatility at current highs. Close attention should be paid to how quickly — or slowly — end users begin to engage with higher-priced material in the physical market. Until that happens, the rally remains a cost-driven move searching for demand-side confirmation.

Written by Bruce Chew

Nickel & Stainless Steel Analyst, Shanghai Metals Market

Email: bruce.chew@metal.com

Tel: +601167087088

![[SMM Analysis] Month-End Buying Sentiment Saw No Rebound; Nickel Salt Prices Slightly Rose This Week](https://imgqn.smm.cn/usercenter/LNpBh20251217171732.jpeg)

![[SMM Nickel Sulphate Daily Review] July 30: Downstream purchasing sentiment weak, nickel sulphate prices stable.](https://imgqn.smm.cn/usercenter/Btmsv20251217171733.jpg)

![[SMM Nickel Midday Review] On July 30, nickel prices shot up and pulled back, and the July US Fed FOMC meeting kept interest rates unchanged.](https://imgqn.smm.cn/usercenter/CWsEw20251217171732.jpeg)