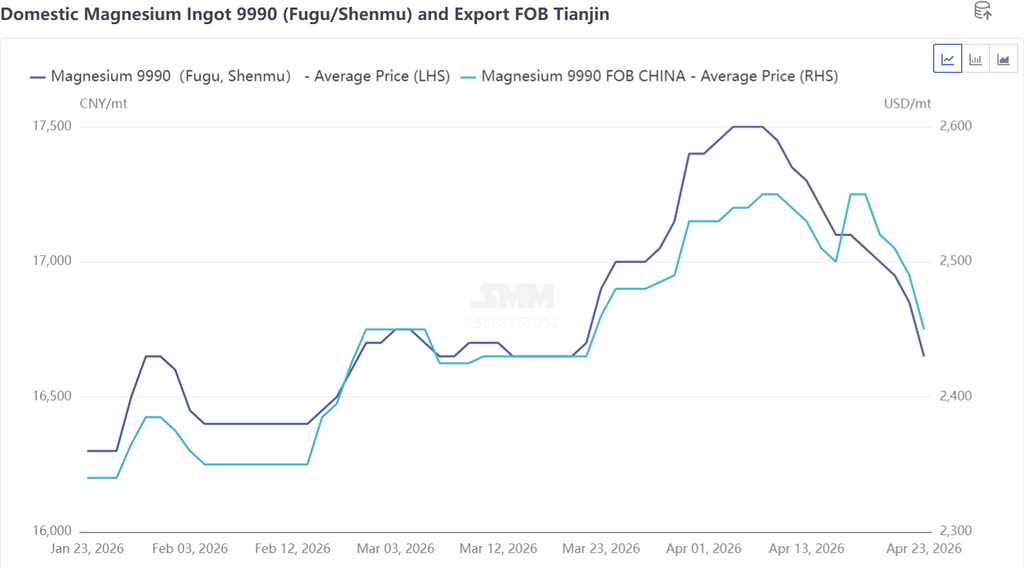

In early April, the industry chain held strong bullish sentiment, with manufacturers showing obvious reluctance to sell. Market available supplies remained tight, end‑use enterprises stocked up in advance, and overall market transactions were robust. Coupled with rising speculative demand and growing willingness among traders to hoard goods, magnesium prices trended upward step by step.In mid-to-late April, driven by height aversion, end‑use procurement slowed down. Meanwhile, manufacturers engaged in panic selling, leading to continuous gradual declines in market prices.

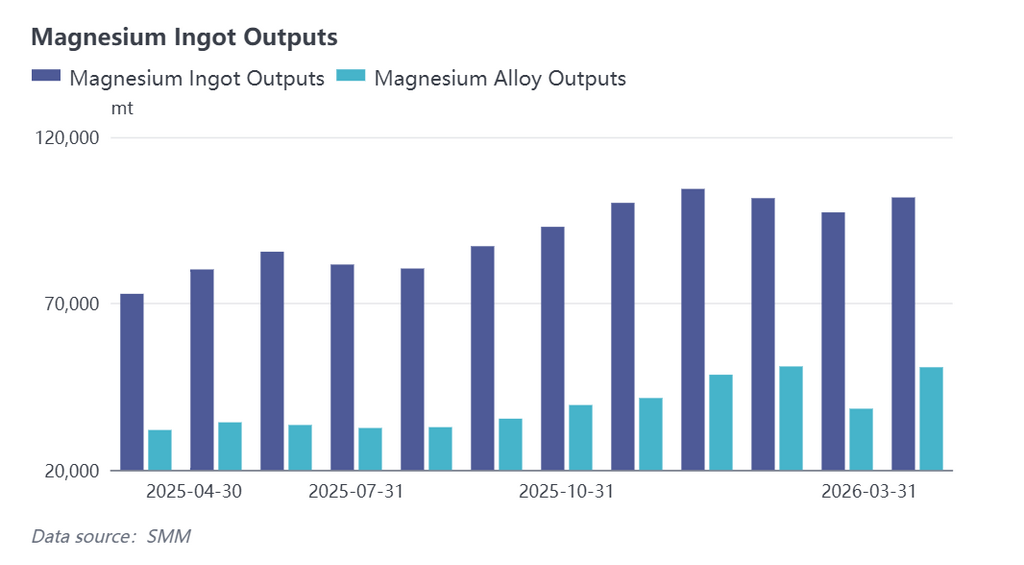

Simultaneous Rise in Primary Magnesium and Magnesium Alloy Output – Supply Growth Far Outpaces Demand Analysis of Pressures on Magnesium Price Upside

Taking primary magnesium and magnesium alloy output in March 2026 as an example:

- Primary magnesium output in March 2026 increased by 25,100 tonnes year-on-year.

- Magnesium alloy output in March 2026 rose by 22,900 tonnes year-on-year.

Based on an average scrap addition ratio of 29.3% and alloying element addition ratio of 10% for magnesium alloys, demand for primary magnesium from the magnesium alloy sector in March 2026 is estimated at 13,900 tonnes.The supply–demand mismatch and blind mutual expansion on both supply and demand sides created an estimated demand gap of 11,200 tonnes. Affected by this, magnesium prices saw repeated upward spurts driven by speculative sentiment and end‑use restocking, yet struggled to hold high levels, resulting in a narrow range‑bound trend.

Traditional Export Demand for Primary Magnesium Blocked in Short Term Magnesium Alloy Demand Alone Unable to Support the Market

Since 2026, customs has continuously strengthened crackdowns on non‑compliant export practices involving magnesium products. Meanwhile, supervision over magnesium‑containing substances potentially subject to dual‑use item export controls, as mentioned in relevant 2024 policies, has also tightened.

Recently, all vessels carrying magnesium‑containing substances have been required to provide quality inspection certificates proving the goods do not fall into the dual‑use item category specified in policy documents before being cleared. This measure has sent a clear tightening signal to the magnesium export market, and supervision is expected to intensify further going forward.

In the current magnesium ingot market, exports remain the main consumption pillar for primary magnesium. However, ongoing tighter customs supervision has significantly increased export risks for foreign trade traders. Out of caution, some merchants have slowed the pace of export order fulfillment.Coupled with the market psychology of “buying on rises, not on declines”, traders have generally delayed purchasing plans, leading to weak short‑term external demand.

Speculative Sentiment Amplifies Magnesium Price Volatility Market Awaits Return to Rationality

As magnesium alloy projects come on stream one after another, social capital has accelerated its entry into the sector.In early April, strong bullish sentiment and active transactions drove a rapid rise in magnesium prices. But after hitting highs, upward momentum faded. Previously accumulated low‑cost inventories were sold off in bulk at lower prices, pushing magnesium prices into a downward spiral and spreading panic.

In addition, smelters faced dual pressures of funding and inventories, causing market quotations to keep falling and locking the sector in a vicious cycle of price competition.

Supply‑Strong–Demand‑Weak Pattern Established in Magnesium Market Where Will Magnesium Prices Head Next?

Driven by profit margins, operating rates of primary magnesium smelters continued to rise in April. National primary magnesium output in April is expected to hit another historical high, with a month-on-month increase of more than 4,000 tonnes compared to March, further reinforcing the supply‑strong–demand‑weak pattern.A meaningful boom in magnesium alloy demand has yet to materialize.

Overall, the market is expected to remain weak in the short term. However, current price levels are gradually approaching the break‑even point for primary magnesium smelters, which may choose to conduct maintenance or suspend production. SMM will closely track operating rates of primary magnesium smelters in major production areas in a timely manner.

![[SMM Analysis] May Magnesium Exports Down 4% MoM, Q2 Market Under Pressure Amid Geopolitical Risks](https://imgqn.smm.cn/usercenter/tjmLW20251217171722.jpeg)