May Magnesium Exports Pull Back MoM, Q2 Export Market Under Pressure

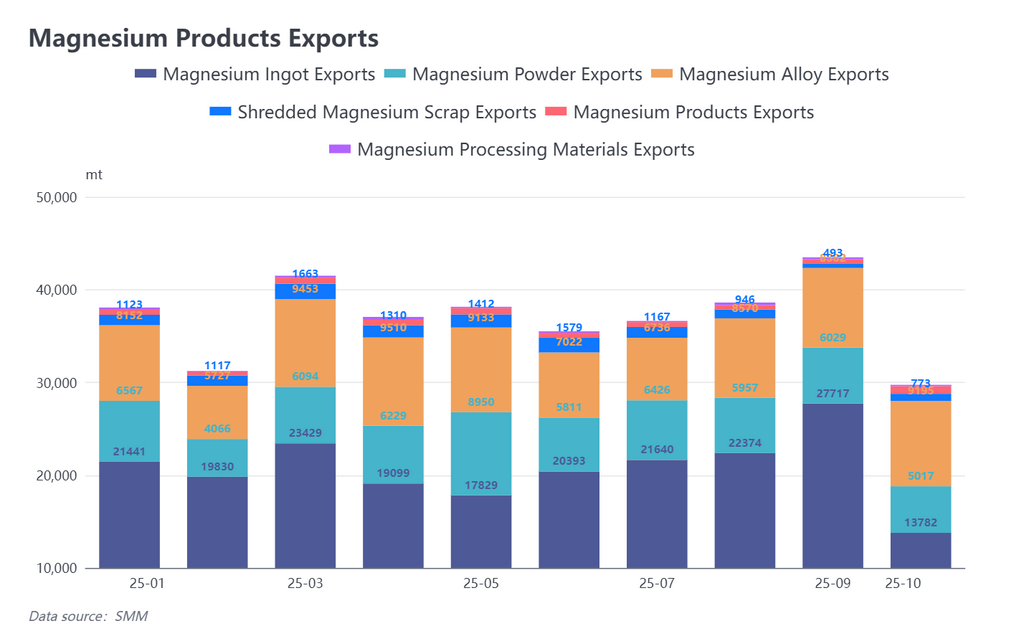

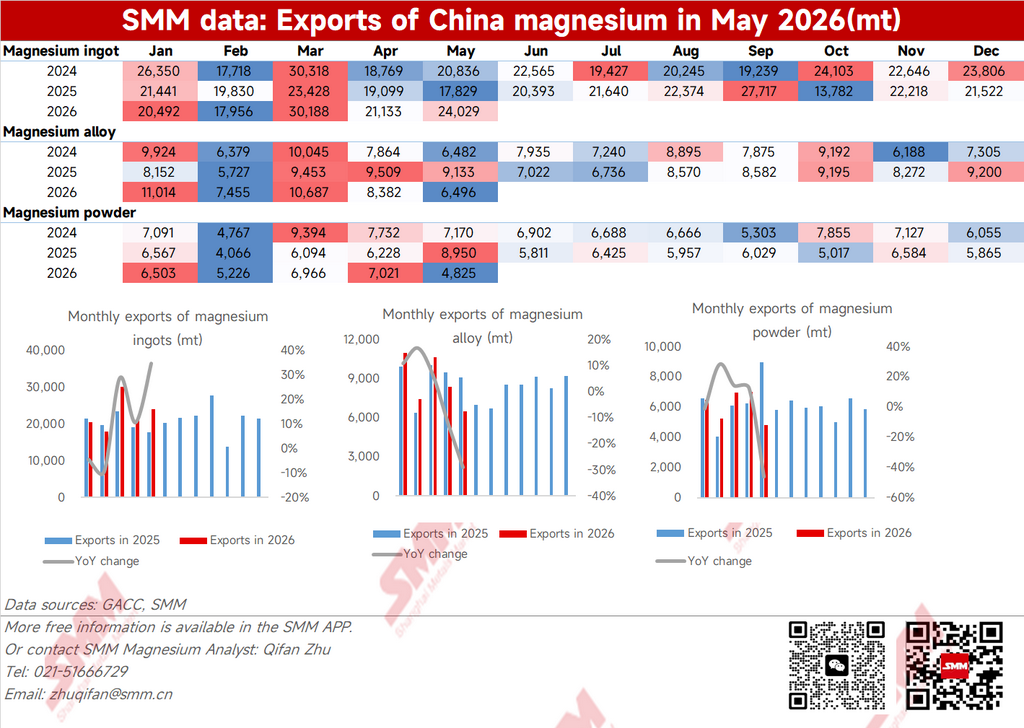

In May 2026, China's magnesium product exports stood at 37,600 mt, down 4% MoM and 1.5% YoY.

From January to May, cumulative exports reached 199,700 mt, up 7.4% YoY.

In Q2 this year, magnesium exports overall were in the doldrums, mainly due to persistently weak export orders. The US-Iran war has been escalating repeatedly since March, exacerbating uncertainty in the shipping market. High ocean freight rates put sellers under pressure and made buyers more cautious in procurement. Meanwhile, the Middle East lacked new purchases and tenders, and geopolitical risks continued to weigh on export market sentiment. Furthermore, the export growth this year was mainly concentrated in a concentrated release in March, which to some extent pre-empted export demand for April and May.

The export weakness was simultaneously transmitted to the domestic primary magnesium market. Demand-side support continued to weaken and magnesium prices fell under pressure. As of June 25, the SMM FOB Tianjin port quotation was $2,310/mt, down a cumulative 5% from early May. A new round of export orders may remain on the sidelines.

May Magnesium Exports Diverge: Magnesium Ingot Steady Rise, Magnesium Powder and Magnesium Alloy Pull Back

By product, magnesium ingot export performance remained stable, while magnesium powder and magnesium alloy exports pulled back sharply.

In May 2026, magnesium ingot exports were 24,000 mt, up 13.7% MoM, and cumulative growth was 11.98% YoY. The good export performance of magnesium ingot reflected that downstream demand for magnesium ingot had increased since 2026, especially as end-user automotive and traditional aluminum industries showed signs of a concentrated recovery. However, exports in May remained dominated by shipments of earlier orders, coupled with a slight pullback in ocean freight rates and the resumption of smooth navigation on some Middle East shipping routes, pushing a batch of front-loaded orders to be shipped in a concentrated manner. After June, high ocean freight rates may again drive up costs.

In May 2026, magnesium powder exports were 4,825 mt, down 31.28% MoM, and cumulative YoY decreased by 4.28%. Since the beginning of this year, magnesium powder export orders showed a brief surge before quickly pulling back, with significant reductions in demand from key markets such as Canada and Europe. In the short term, high magnesium prices may exert some restraint on orders, and attention should be paid to the pace of the release of a new round of purchasing once magnesium prices pull back.

In May 2026, magnesium alloy exports were 6,496 mt, down 22.5% MoM but up 4.91% cumulatively YoY. The magnesium alloy foreign trade market has ended its earlier supply-demand mismatch phase, with actual demand weakening again. As the European market gradually enters the summer break off-season in July and August, magnesium alloy export demand may continue to slow down.

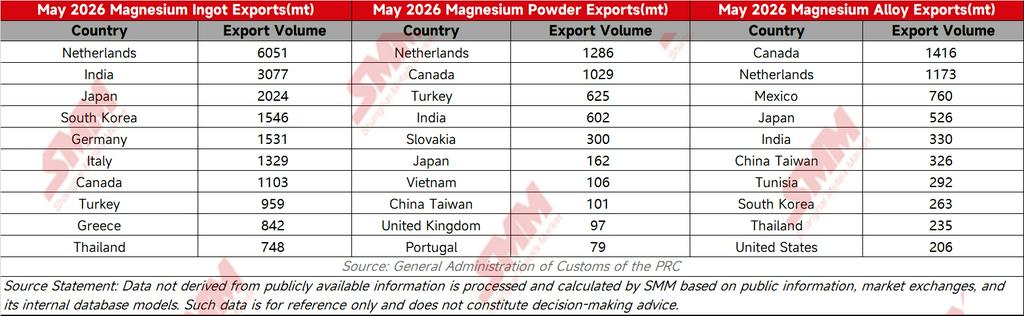

Magnesium Exports in May: Netherlands, India Demand Steady; Japan Surges with Pullback Risk Ahead

From the export data by destination, for magnesium ingot, the Netherlands maintained steady demand and the Indian market remained robust throughout the year. Notably, China's cumulative magnesium ingot exports to Japan reached 12,000 mt in January-May 2026, up 76.6% YoY. The possibility of front-load orders cannot be ruled out, and exports to Japan in H2 could pull back sharply. In the Middle East, aside from 1,500 mt exported to the UAE in April, there were almost no new orders this month.

For magnesium alloy and magnesium powder, Canada and the Netherlands remained the main export destinations, though orders edged down MoM.

H2 Magnesium Export Outlook: Multiple Risks Intertwined; Full-Year Exports Still Expected to Edge Up

Key risks facing H2 exports: fluctuating ocean freight rates continue to push up costs; expectations of primary magnesium maintenance in July could trigger a price rebound, heightening raw material procurement loss risks; sluggish foreign trade orders, declining market activity, and intensifying industry competition.

For buyers, the recent price pullback provides a favorable purchasing window ahead of the summer break, but budget pressure from potential ocean freight rate increases should be watched. Overall, magnesium prices are expected to be higher than last year's levels.

For full-year 2026, magnesium product exports are expected to edge up, but geopolitical risks will still exert some restraint on exports.

![Magnesium Plant Maintenance Drags Weekly Output; Strong Supply and Weak Demand Sustain Inventory Buildup [SMM Magnesium Weekly Data]](https://imgqn.smm.cn/usercenter/hSSxt20251217171722.jpeg)