SMM April 13 News

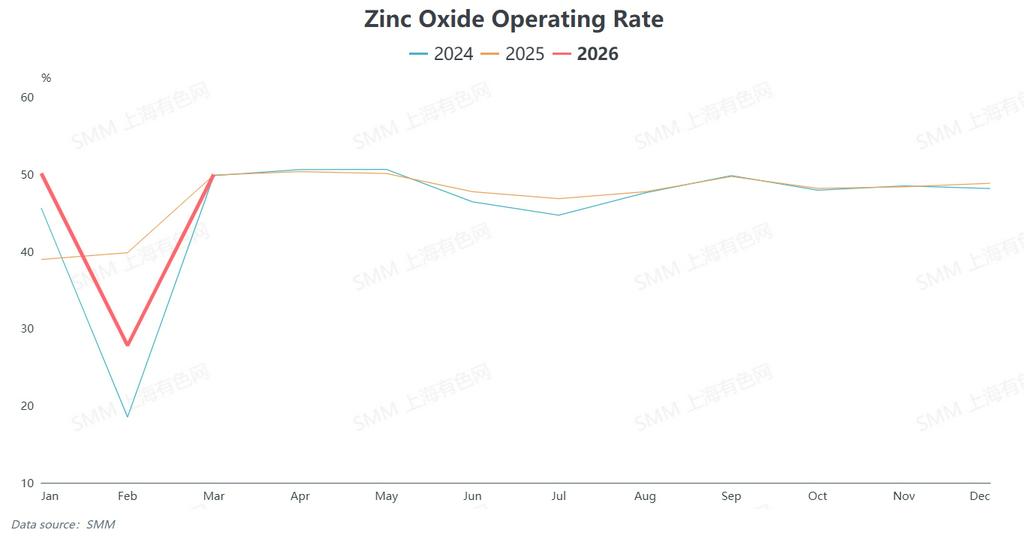

According to SMM data, China’s average operating rate of zinc oxide stood at 38.88% in Q1 2026, down 3.98 percentage points year-on-year.What are the reasons behind this?

Key Reasons

- Geopolitical risks persisted in late January, bringing high macro uncertainty and rising zinc prices above 25,000 yuan/tonne. End-users curbed orders under price pressure, dragging down operating rates.

- The 2026 Spring Festival fell in mid-February, later than last year. High zinc prices disrupted pre-holiday restocking, leaving strong wait-and-see sentiment. Many small and medium-sized enterprises suspended production early due to capital and order strains.

- Some zinc oxide producers extended shutdowns and maintenance over the holiday, further lowering Q1 output.

Current Dilemmas & Outlook

- Rising costs, squeezed margins

Turmoil in the Middle East has disrupted sulfur and sulfuric acid supplies, pushing up sulfuric acid prices and raising production costs for active zinc oxide producers. Intense competition has made price pass-through difficult, severely compressing profits.

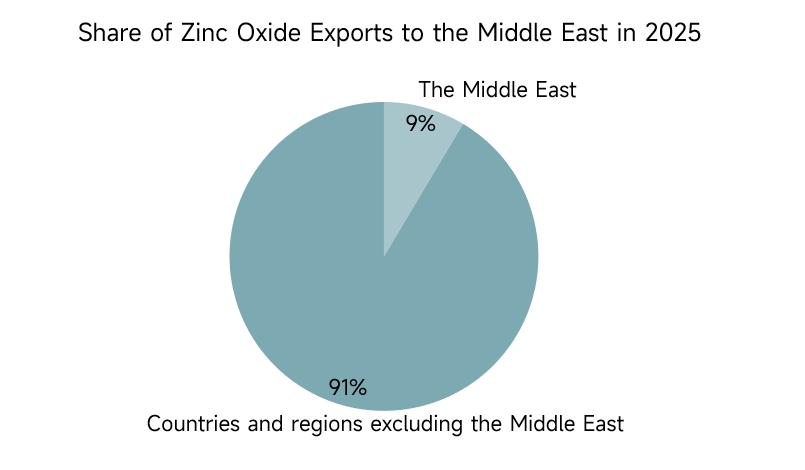

- Exports under two-way geopolitical pressure

As a net exporter, China’s annual zinc oxide exports stay below 20,000 tonnes. In 2025, 9% (1,464 tonnes) of zinc oxide was shipped to the Middle East.

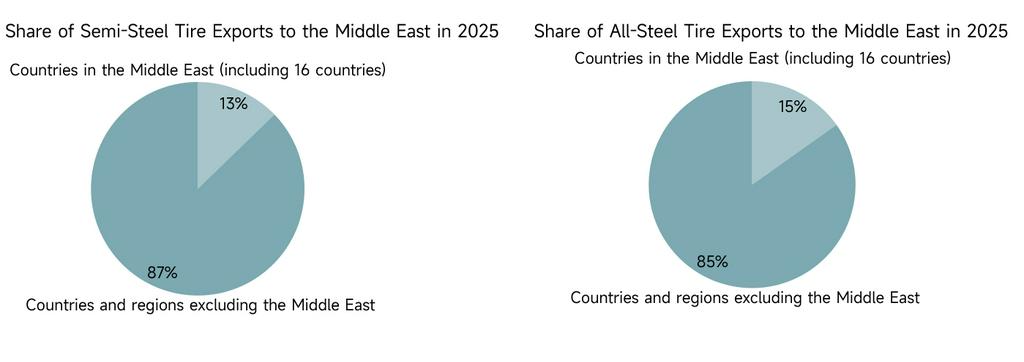

Rubber-grade zinc oxide is widely used in tires: 15% of China’s TBR tires and 13% of PCR tires were exported to the Middle East in 2025.

Further escalation in the Middle East would hit zinc oxide and tire exports via logistics disruptions, settlement risks and weaker demand.

(Note: Tire statistics include retreaded tires.)

Overall, the current zinc oxide market presents both opportunities and challenges.

On the challenges side:

Geopolitical risks in the Middle East have not fundamentally eased; zinc prices and sulfuric acid costs remain highly volatile. The stability of export channels to the Middle East is in doubt. Intense low-price competition within the industry shows no sign of self-adjustment in the short term, further increasing cost and pricing pressure on enterprises.

On the opportunities side:

First, if signs of de-escalation emerge in the Middle East, suppressed export demand may see concentrated release, triggering a phased restocking market. Second, in Q1, fixed-asset investments by State Grid and China Southern Power Grid rose 37% and 49.5% year-on-year respectively. In addition, China’s “trade-in” policies continue to support the automotive and power grid sectors, which are expected to maintain sound growth and provide solid support for the zinc oxide industry.

![Macro sentiment is weak, SHFE zinc records a four-day losing streak [SMM Zinc Morning Comment]](https://imgqn.smm.cn/usercenter/qTzTI20251217171754.jpg)

![LME Zinc Center Shifts Down amid Expectations for US Fed Interest Rate Hikes [SMM Morning Meeting Minutes]](https://imgqn.smm.cn/usercenter/VPThK20251217171754.jpg)