SMM News, 22 janvier :

En 2025, le marché chinois de l'import-export des produits au tungstène a été marqué par une hausse du volume et des prix à l'importation, une pression sur le volume total des exportations et une différenciation structurelle qui s'accentue. Ces caractéristiques reflètent non seulement la contradiction entre les contraintes de ressources et la demande haut de gamme dans la chaîne industrielle nationale du tungstène, mais aussi l'impact profond de l'ajustement du paysage manufacturier mondial sur cette industrie.

Comparaison des volumes d'import-export : L'écart croissant entre importations et exportations souligne le décalage structurel entre ressources et demande

Côté exportations : Contraction persistante

Le volume total annuel des exportations de produits au tungstène a atteint 15 514,7 tonnes (en quantité physique) en 2025, en baisse de 19,7 % sur un an ; converti en quantité de métal, il s'est établi à 13 095,7 tonnes, reculant de 20,0 % en glissement annuel. Le volume exporté en décembre seul s'est élevé à 1 264,1 tonnes, affichant une légère hausse mensuelle de 0,8 %, mais une forte baisse annuelle de 40,1 %, indiquant que la tendance faible de l'année est restée inchangée.

Côté importations : Expansion substantielle

Le volume total annuel des importations de produits au tungstène a atteint 23 210,9 tonnes (en quantité physique) en 2025, bondissant de 39,5 % sur un an ; le volume importé en décembre a atteint 2 907,3 tonnes, en forte croissance mensuelle de 29,5 % et en hausse annuelle de 58,1 %, montrant que l'intensité des achats a nettement augmenté en fin d'année.

Marché à l'exportation des matières premières et produits intermédiaires au tungstène : Une reprise en dents de scie incapable d'inverser la tendance à la baisse

Les données mensuelles d'exportation tout au long de 2025 montrent qu'après la publication des politiques chinoises de contrôle des exportations de produits liés au tungstène en février 2025, le volume exporté de produits contrôlés comme le paratungstate de sodium et le carbure de tungstène a chuté significativement. Selon les statistiques douanières, le volume total annuel des exportations de paratungstate d'ammonium, de poudre de tungstène et de produits en poudre de carbure de tungstène en 2025 était d'environ 3 877 tonnes, en baisse d'environ 41,7 % sur un an.

Étant donné que certaines entreprises étrangères sont fortement dépendantes de la Chine pour les matières premières en amont du tungstène, les primes à l'étranger ont augmenté après la mise en œuvre des contrôles à l'exportation, ce qui a également contraint certaines entreprises étrangères à se tourner vers l'achat de métatungstate d'ammonium et d'autres produits tungstiques. Le volume annuel total des exportations de ces produits a augmenté de 44,2 % en glissement annuel pour atteindre environ 2 837 tonnes, tandis que le volume annuel des exportations de produits à base de tungstate de sodium a atteint 306 tonnes, bondissant de 915,7 % sur un an.

De plus, le volume d'exportation des produits en tungstène nationaux a affiché une croissance soutenue en 2025. Parmi eux, le volume total d'exportation de tungstène non ouvré, de barres et de tiges a atteint environ 2 112 tonnes, en hausse de 84,3 % sur un an, ce qui reflète également que certaines entreprises terminales étrangères se sont tournées vers l'achat de produits en tungstène aval comme substituts plutôt que de produits intermédiaires.

Du point de vue de la période d'exportation, la baisse en glissement annuel du volume total des exportations de tungstène national au cours des trois premiers trimestres de 2025 a été relativement faible. Cependant, les prix du tungstène national ont augmenté rapidement au quatrième trimestre, entraînant un écart de prix significatif avec les marchés étrangers. Cela a conduit à des marges d'exportation négatives pour certains produits, freinant l'enthousiasme des exportateurs nationaux. Parallèlement, la volonté des entreprises terminales étrangères d'acheter des produits en tungstène à prix élevé a diminué. Le volume total des exportations de produits en tungstène nationaux au quatrième trimestre était d'environ 3 559 tonnes, en baisse de 24,2 % sur un mois et de 34,8 % sur un an.

Destinations des exportations

En 2025, les produits en tungstène chinois étaient principalement exportés vers le Japon, l'Union européenne, les États-Unis et d'autres pays et régions. Parmi eux, les exportations vers le Japon ont atteint 3 879 tonnes (en quantité de métal), en baisse de 13,3 % sur un an, représentant environ 28 % des exportations totales de produits en tungstène de la Chine, se classant au premier rang.

Le 6 janvier 2026, le ministère du Commerce a publié l'Annonce sur le renforcement du contrôle des exportations de biens à double usage vers le Japon, stipulant que : l'exportation de tous les biens à double usage vers des utilisateurs militaires japonais à des fins militaires, ainsi qu'à d'autres fins d'utilisateurs finaux qui contribuent à renforcer les capacités militaires du Japon, est interdite. Toute organisation ou individu dans tout pays ou région qui transfère ou fournit des biens à double usage originaires de la République populaire de Chine à des organisations ou individus au Japon en violation des dispositions ci-dessus sera tenu responsable légalement. On prévoit que le volume ultérieur des exportations de produits liés au tungstène vers le Japon affichera une tendance à la baisse.

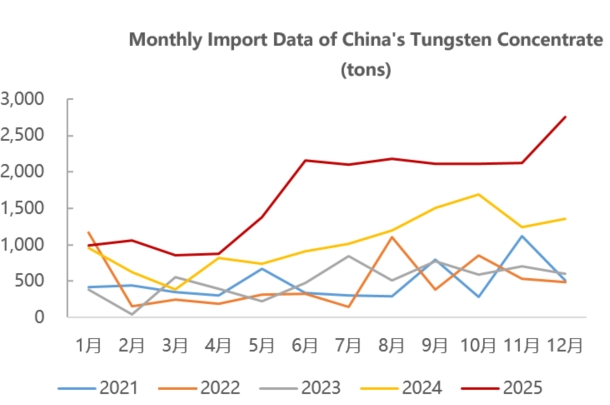

Marché des importations : Piloté par les ressources, les importations nationales de minerai de tungstène ont considérablement augmenté en 2025

Concentrés de minerai de tungstène

Le volume annuel des importations a atteint 20 676,0 tonnes, en hausse de 66,9 % sur un an ; le volume importé en décembre s'est établi à 2 750,0 tonnes, soit une augmentation de 29,9 % sur un mois et de 102,6 % sur un an.

En 2025, les importations chinoises de minerai de tungstène provenaient principalement du Kazakhstan, du Myanmar, de la Corée du Nord et d'autres pays et régions. Parmi ceux-ci, le Kazakhstan est apparu comme le plus grand fournisseur de concentrés de minerai de tungstène de la Chine, avec des importations totalisant environ 6 899 tonnes en 2025, représentant 33 % du total des importations chinoises de concentrés de minerai de tungstène.

Sur la base des données de valeur et de volume des importations, SMM estime que le prix unitaire à l'importation du minerai de tungstène kazakh en décembre était d'environ 34 000 dollars US par tonne (équivalent à 310 000 yuans par tonne standard), tandis que le prix mensuel moyen du concentré de wolframite à 65 % sur le marché intérieur en décembre était d'environ 400 000 yuans par tonne standard, indiquant que le minerai kazakh bénéficie toujours d'un avantage coût élevé.

Il est rapporté que la mine de tungstène de Bakuta au Kazakhstan dispose de ressources minérales de 1,104 milliard de tonnes, avec une teneur moyenne de 0,211 % en WO₃, équivalant à 233,2 mille tonnes de teneur en métal de trioxyde de tungstène. Les ressources contrôlées prouvées s'élèvent à 985 millions de tonnes, avec une teneur moyenne de 0,209 % en WO₃. La mine a été mise en production en juillet 2025, et sa production totale est actuellement expédiée vers la province du Jiangxi, en Chine, avec une production mensuelle d'environ 850 à 900 tonnes.

- Myanmar : Le deuxième plus grand fournisseur, avec des importations de 5 175 tonnes, représentant 25 %. Le minerai importé est principalement un minerai associé tungstène-étain de faible teneur (20 %-30 %), qui nécessite des processus de prétraitement complexes.

- Corée du Nord : Les importations ont atteint 3 349 tonnes, représentant 16,6 % du total des importations. Les concentrés de minerai de tungstène importés sont principalement envoyés vers quatre provinces : Jiangxi, Yunnan, Liaoning et Fujian.

Importation et exportation d'outils de coupe en carbure cémenté et de plaquettes pour machines-outils de travail des métaux

En 2025, le volume annuel des exportations d'outils de coupe en carbure cémenté et de plaquettes pour machines-outils de travail des métaux était de 3 441,3 tonnes, en baisse de seulement 1,5 % sur un an. Le volume annuel d'importation s'est établi à 1 346,2 tonnes, en hausse de 6,8 % en glissement annuel.

Au quatrième trimestre 2025, l'élargissement de l'écart de prix des produits en tungstène entre les marchés intérieur et étranger a entraîné une baisse de la rentabilité des exportations de carbure cémenté et d'autres produits nationaux, ouvrant une fenêtre d'importation. Certaines entreprises en aval ont choisi de se fournir en produits de carbure cimenté à l'étranger, ce qui s'est traduit par une croissance des importations de carbure cémenté et d'autres produits au quatrième trimestre.

Néanmoins, la demande intérieure pour certains outils de coupe haut de gamme et produits en carbure cémenté dépend encore des importations. Du point de vue du marché à l'exportation, sous l'effet des droits de douane étrangers, le volume des exportations de carbure cémenté et d'outils de coupe nationaux est resté relativement stable en 2025. Associée à la situation tendue de l'offre en matières premières de tungstène à l'étranger, la rentabilité à l'exportation du carbure cémenté et d'autres produits devrait continuer de croître à l'avenir.

Dans l'ensemble, dans le double contexte de la restructuration de l'approvisionnement mondial en ressources de tungstène et des jeux géopolitiques entre grandes puissances, le marché chinois des importations et exportations de produits en tungstène évoluera vers des caractéristiques d'« importations axées sur les ressources et structure des exportations orientée vers le haut de gamme ».

Du côté des importations, contraintes par le contrôle des quotas d'extraction du minerai de tungstène national et une offre tendue de long terme, associées à une demande résiliente dans les domaines haut de gamme comme le photovoltaïque et l'aérospatial, les importations chinoises de produits à base de ressources telles que les concentrés de minerai de tungstène resteront à un niveau élevé à l'avenir. Parallèlement, de nombreux pays en Europe et aux États-Unis ont classé le tungstène comme ressource de réserve stratégique, ouvrant une période de compétition pour les droits sur les ressources dans la prospection et l'extraction du minerai de tungstène à l'étranger.

Récemment, plusieurs mines de tungstène en Asie centrale ont enregistré de nouvelles avancées, comme les gisements de North Katpar et Upper Kailakht au Kazakhstan, et le projet K-Tungsten en Ouzbékistan (avec des réserves de 106 700 tonnes de WO₃, dont la production est prévue pour 2028). Simultanément, alors que l'Ouzbékistan accélère la construction de capacités de transformation locales en révisant la réglementation minière et en construisant un complexe de métaux technologiques, les mines de tungstène d'Asie centrale pourraient devenir une importante région d'approvisionnement en minerai de tungstène à l'étranger à l'avenir. Par la suite, une attention particulière devra être portée à la construction et à la mise en service de nouvelles mines en Asie centrale.

Concernant les exportations, dans un contexte où les produits en tungstène sont soumis à une licence d’exportation pour biens à double usage et où le prix FOB de l’APT domestique a augmenté de plus de 200 % par rapport au début de 2025 (atteignant 1 200–1 260 dollars américains par tonne-unité en janvier 2026), les exportations de matières premières traditionnelles en tungstène et de produits de moyenne à bas de gamme continueront d’être freinées à la fois par les contrôles politiques et par une compétitivité-prix affaiblie.

Cependant, les catégories à haute valeur ajoutée, telles que les fils de tungstène pour le photovoltaïque et les outils de coupe en carbure cémenté haut de gamme, grâce à l’avantage de la Chine représentant 80 à 90 % de la capacité mondiale et aux barrières technologiques dans la transformation avancée, maintiendront leur résilience à l’exportation. De plus, les entreprises continueront d’élargir leurs marchés le long des Nouvelles Routes de la Soie et dans les marchés émergents pour compenser les fluctuations de la demande en Europe et en Amérique dues aux stratégies de diversification des chaînes d’approvisionnement.

Globalement, les contraintes pesant sur l’exploitation des ressources minières de tungstène en Chine entraîneront inévitablement une augmentation de l’exploitation et de l’utilisation des ressources à l’étranger. Parallèlement, le marché chinois des importations et exportations de produits en tungstène s’articulera autour de la logique centrale de « garantir la sécurité par des importations stables de ressources et renforcer les barrières par des exportations haut de gamme », cherchera un équilibre dynamique dans un contexte de rivalité entre grandes puissances et de restructuration des chaînes de valeur, renforcera les barrières technologiques avancées et construira progressivement un système industriel plus résilient, mieux coordonné en interne et externe, et capable de faire face aux risques.

![Les prix des contrats à long terme et des prévisions des associations baissent de concert ; l'effet de basse saison couplé à un bras de fer entre vendeurs et acheteurs — Comment le marché du tungstène se comportera-t-il ? [SMM Comment]](https://imgqn.smm.cn/usercenter/XUnxM20251217171723.jpeg)