SMM News, January 16th:

This week, China's tungsten market maintained a strong upward trend. The tight supply situation at the mine end became more prominent, driving the steady rise in upstream raw material prices in the industrial chain. However, the downstream demand side was constrained by the off-season effect, resulting in an overall differentiated trading characteristic of "shrinking volume with rising prices". The overseas market followed the domestic market with a slight upward movement, with strong wait-and-see sentiment.

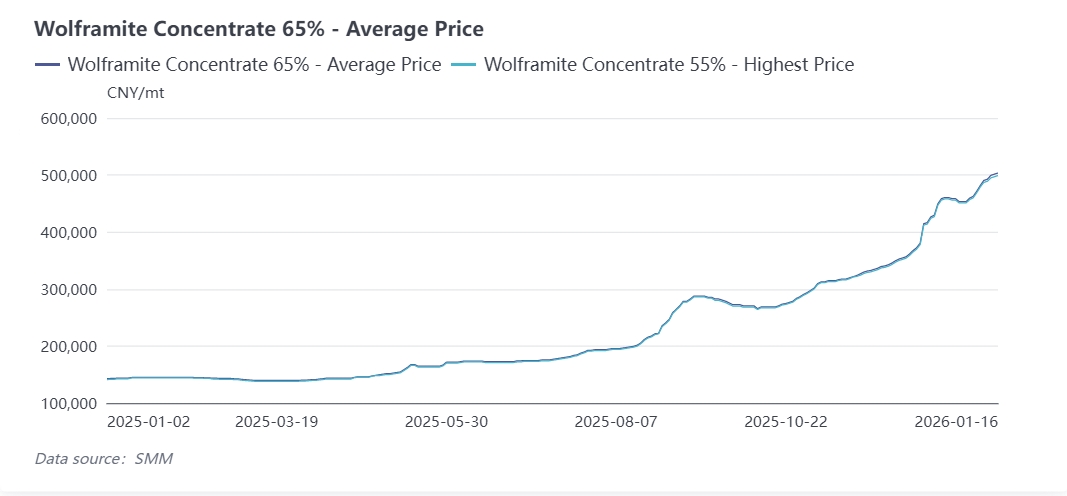

This week, the tight supply pattern in the tungsten concentrate market remained unchanged, and prices hit a new stage high. After major mines completed part of the auction sales last week, the centralized shipment volume dropped significantly this week, mainly maintaining stable shipments and controlling the rhythm, while spot quotes remained firm. The core contradiction in the market still focuses on the scarcity of high-grade ore resources. The shipment volume of high-grade tungsten concentrate is extremely small, and quotes continue to rise, leading to a further widening of the price gap between medium-low grade and high-grade ore to around 5,000 yuan per standard ton.

The superposition of policy and seasonal factors has intensified supply contraction. As the end of the year approaches, the frequency of safety inspections, environmental supervision and special campaigns against illegal mining in major producing areas such as Hunan and Jiangxi has increased significantly. Small and scattered mines maintain low operating rates due to compliance and cost pressures, and some even stop production and withdraw in advance; large mines have also gradually entered the year-end consolidation stage, taking the initiative to reduce shipments to avoid risks and sort out inventories, resulting in a continuous tightening of overall market circulation. Supported by this, as of January 16th, the price of 65% black tungsten concentrate has exceeded the 500,000 yuan/ton mark, with some spot quotes approaching 510,000 yuan/ton. The main tungsten raw material prices have increased by more than 11% since New Year's Day, and the industry's bullish sentiment is strong. From the perspective of supply fundamentals, China's tungsten ore mining is subject to total volume control. The tightening of quotas, coupled with rising mining costs and the current historical low social inventory, makes it difficult to ease the short-term tight supply pattern.

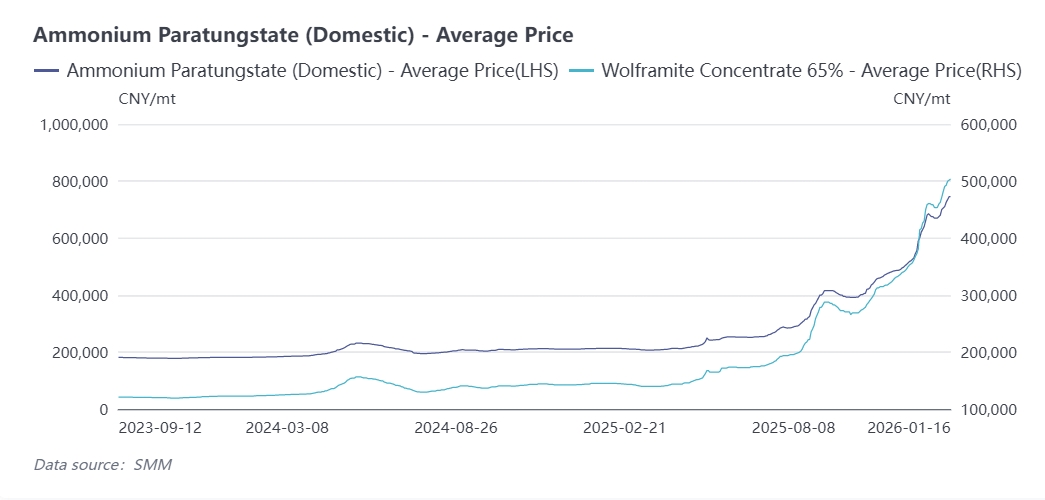

This week, the APT (Ammonium Paratungstate) market followed the raw material side with a slight increase, but the growth rate was lower than that of tungsten concentrate, showing a "low follow-up growth" trend. Affected by the rising price and tight supply of upstream tungsten concentrate, the cost pressure on APT production enterprises continued to increase, and quotes were raised accordingly. Currently, the APT price has stood above the 750,000 yuan/ton mark. Some enterprises have slightly reduced their production capacity release scale due to the increased difficulty in raw material procurement. The sluggish demand side has restricted market activity. Downstream tungsten powder enterprises mainly replenish inventories on rigid demand, with a cautious purchasing rhythm, mostly taking goods on demand according to their own inventory levels, resulting in an overall shrinkage in market transactions. Prices of downstream derivative products such as tungsten powder and tungsten carbide powder rose synchronously with the industrial chain. As of this week, the price of tungsten powder has exceeded 1.2 million yuan/ton. At present, terminal cemented carbide enterprises have entered the traditional off-season, and the weak demand in the manufacturing industry has been transmitted to the industrial chain. Demand in traditional fields such as general machinery processing and metallurgy has declined significantly, and enterprises' purchasing willingness is insufficient. Most demand is carried out in the form of "case-by-case negotiation".

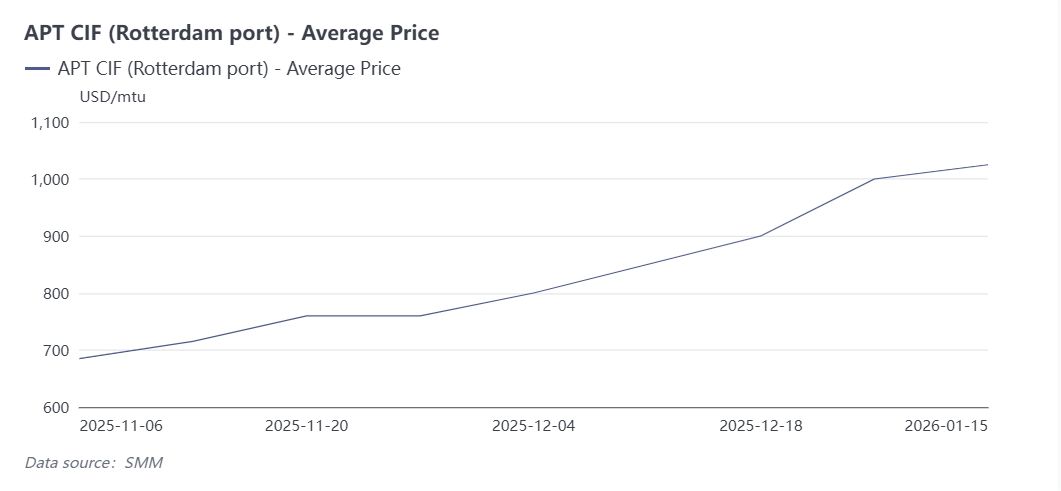

This week, the overseas tungsten market followed the domestic market with a slight upward movement, but overall transactions were sluggish, and the inventory replenishment cycle has not yet started. In the European market, the average APT price CIF Rotterdam Port rose to 1,025 US dollars/ton unit, and the average price of ferrotungsten (Rotterdam warehouse) was 145.5 US dollars/kg tungsten, showing a significant increase compared with the end of last month. However, European downstream customers generally find it difficult to accept the current price increase and mostly adopt a wait-and-see attitude. Only some terminal enterprises have gradually accepted quotes for Chinese goods due to rigid production demand. Overseas traders said they will further raise quotes according to the trend of the Chinese market to maintain purchasing competitiveness. At the same time, the impact of the global policy environment continues to emerge. China's implementation of export control measures on some tungsten products has led to a significant premium in the overseas market. The behavior of major consumers such as the EU and the United States to expand strategic reserves has further intensified expectations of tight global supply. However, the overseas demand side has not formed an effective boost in the short term, and the market as a whole has fluctuated within a narrow range.

In the short term, as the Spring Festival approaches, the scope of mine shutdowns and consolidation in major producing areas will further expand, and the tight supply pattern at the mine end may continue to strengthen. Coupled with the support of current low inventory, tungsten concentrate prices still have room for upward movement and will continue to be transmitted to APT and downstream. On the demand side, the traditional off-season effect will continue until after the Spring Festival, and there will be no substantial improvement in demand from terminal cemented carbide enterprises. The trend of shrinking transactions in the industrial chain may persist, and the price growth rate may gradually narrow. In the medium and long term, the rigid constraints on global tungsten resource supply will remain unchanged. The growth in domestic high-end manufacturing demand is highly certain, and supported by overseas strategic reserve demand, the tungsten market is expected to maintain high-level operation. However, we need to be alert to the risk of demand contraction caused by cost pressures on downstream small and medium-sized enterprises, as well as the disturbance to the market from the slower-than-expected start of the overseas inventory replenishment cycle. It is recommended that industrial chain enterprises closely monitor changes in mine-end supply and downstream inventory replenishment willingness before the Spring Festival, and reasonably control inventory levels.