I. Titanium Concentrate Market: Domestic and Imported Ore Prices Weaken Simultaneously, Supply Surplus Pattern Persists Throughout the Year

Domestic Titanium Ore: Supply Surplus Pattern Unlikely to Change This Year

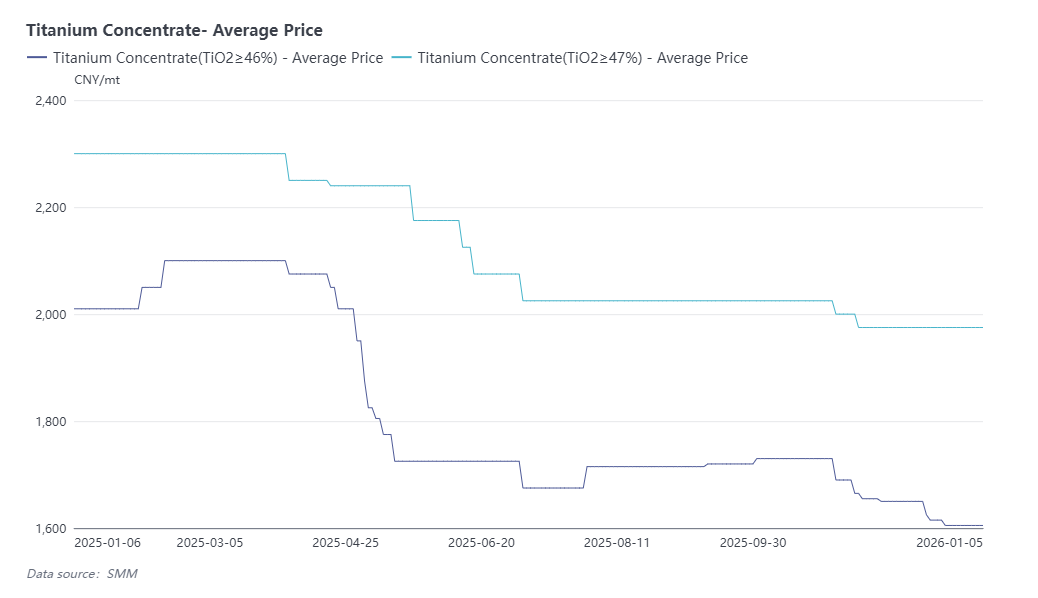

As of December 31, the price of domestic titanium concentrate (TiO₂ ≥ 46%) is quoted at 1,580–1,630 yuan per ton, with an average price of 1,605 yuan per ton, down 21.7% from the beginning of the year. The price of TiO₂ ≥ 47% specification is quoted at 1,900–2,050 yuan per ton, with an average price of 1,975 yuan per ton, down 14.13% from the beginning of the year.

This year, domestic titanium ore prices broke the seasonal fluctuation pattern of previous years, showing a continuous downward trend. Specifically:

January–March: Prices Stabilized

The Panzhihua region entered the Spring Festival maintenance period, with low operating rates and low inventory levels among miners. At the same time, downstream titanium dioxide market orders were strong, and new production capacities were gradually released, supporting ore prices in a consolidation phase.

March–July: Accelerated Decline

After March, the supply of ore increased significantly, with both raw ore mining and shipments rising simultaneously. However, the demand side of the titanium dioxide market remained persistently weak, and overall end-use industries were sluggish. The titanium ore market gradually shifted to a supply surplus, and prices continued to decline under demand pressure.

August–December: Weak Stabilization Followed by Another Decline

With the Panxi region controlling raw ore shipments, the market’s decline slowed, entering a phase of weak stability at low levels. However, demand showed no signs of improvement, mine inventories gradually accumulated, and prices lacked upward momentum. By the end of the year, the market once again faced downward pressure.

Overall, the continuous weakening of titanium ore prices this year was mainly due to weak demand from the titanium dioxide market and its downstream coatings industry, which account for a significant share. Coupled with generally high ore supply, the supply surplus pattern persisted throughout the year, making it difficult to reverse.

Outlook:

In the short term, as post-holiday mine maintenance and downstream demand are expected to stage a recovery, transaction prices may see a slight increase at the higher end. However, this will depend on the inventory digestion situation in the Panxi region. In the long term, according to SMM research, mining output in the Panxi region is expected to significantly decline by 2026, with stricter shipment controls. The titanium ore market is likely to gradually return to its historical seasonal fluctuation pattern.

Imported Titanium Ore: Narrowing Price Gap May Lead to Structural Reshaping

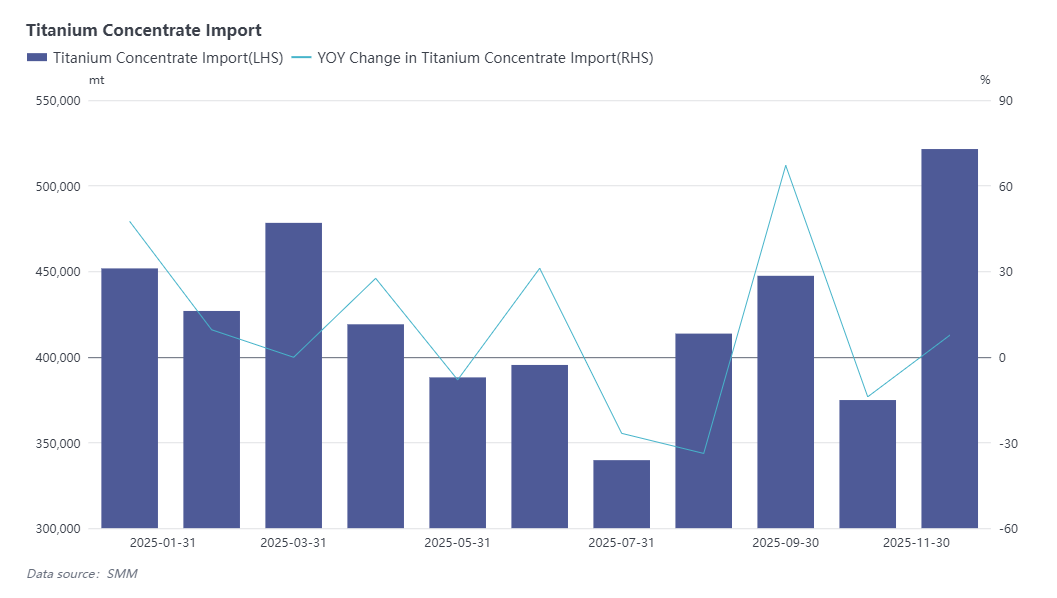

As of December 31, the price of imported titanium concentrate (Mozambique, TiO₂ ≥ 46%) is quoted at 1,700–1,800 yuan per ton; imported titanium concentrate (Nigeria, TiO₂ ≥ 50%) at 1,800–1,900 yuan per ton; imported titanium concentrate (Australia, TiO₂ ≥ 50%) at 1,850–1,959 yuan per ton; imported rutile (Sierra Leone, TiO₂ ≥ 90%) at 5,500–6,000 yuan per ton; and imported rutile (Sierra Leone, TiO₂ ≥ 95%) at 6,500–6,800 yuan per ton. As of November, the cumulative import volume of titanium concentrate this year has reached 4.656 million tons, a year-on-year increase of 3.38%.

The price of imported ore has also continued its downward trend since the second quarter. The main reasons include persistently weak demand for major titanium products such as titanium dioxide and sponge titanium, a sharp decline in titanium dioxide prices leading to cost-price inversion, and widespread price pressure from buyers. At the same time, the price of domestic ore (from the Panxi region), as a major competitor, has continued to fall, forcing importers to adjust their quotations downward accordingly. Although the supply of imported ore tightened somewhat in the second half of the year, with weaker market willingness to sell, transaction prices still followed the overall market downtrend.

Looking ahead, the price of imported titanium ore is expected to continue adjusting in line with the trend of domestic ore, and the profit margins for ore traders may further shrink. As terminal demand gradually recovers slightly, the sluggish state of the titanium ore market is expected to ease. In the long term, the price gap between imported and domestic ore is projected to narrow gradually.

II. Titanium Dioxide Market: Sulfuric Acid Cost Transmission and Industry Challenges

Sulfuric Acid: Year-Long Price Surge Leading to Widespread losses in Sulfate-Process Titanium Dioxide Industry

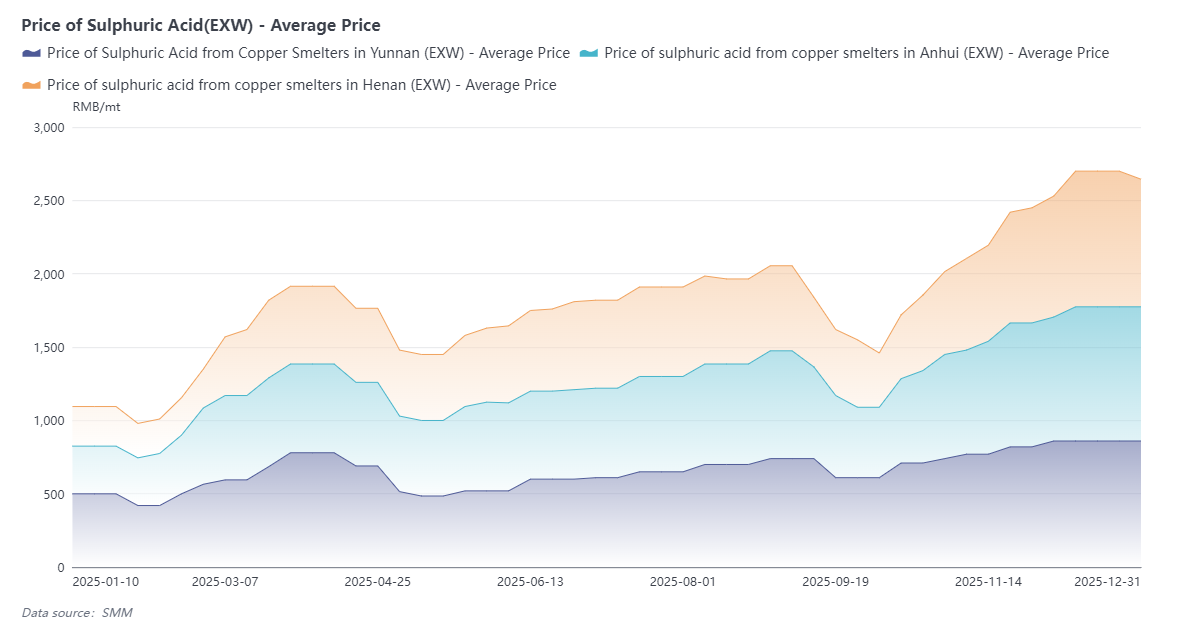

As of December 31, the price of smelting acid (sulfuric acid) in the Anhui region (ex-factory price) is reported at 870–960 yuan per ton, an increase of 181.5% compared to the beginning of the year. In the Henan region, the smelting acid (sulfuric acid) price (ex-factory price) is 840–900 yuan per ton, up 222% year-on-year. In the Yunnan region, the smelting acid (sulfuric acid) price (ex-factory price) is 840–880 yuan per ton, an increase of 72% compared to the beginning of the year. Throughout 2025, especially in the fourth quarter, the sulfuric acid market experienced sustained price surges, placing significant cost pressure on the sulfate-process titanium dioxide industry.

The persistently high prices of sulfuric acid are primarily driven by multiple international and domestic factors:

International Market:

The demand for sulfur from Indonesia's nickel mining projects has increased significantly, creating new demand support; Russia implemented an industrial sulfur export ban in November, substantially tightening global sulfur supply.

Domestic Market:

In the fourth quarter, the fertilizer industry entered its concentrated winter stocking phase. Chemical enterprises' winter fertilizer reserves led to a sharp rise in sulfuric acid demand. Coupled with tightening supply, the market faced a supply-demand imbalance, collectively driving the rapid increase in sulfuric acid prices.

As a key raw material for sulfate-process titanium dioxide production, the high price of sulfuric acid has placed significant cost pressure on titanium dioxide manufacturers, further exacerbating the operational burdens of related producers.

Since mid-December, sulfuric acid prices have entered a phase of consolidation at high levels, showing a slight downward trend. The government has taken measures to regulate sulfur and sulfuric acid market prices, such as restricting exports in the phosphorus chemical fertilizer industry from mid-December to August next year. After the winter fertilizer stocking period ends, it is expected that the operating rates in the fertilizer industry will gradually decline, thereby reducing demand for sulfuric acid. Although sulfuric acid prices are anticipated to decrease after the start of the year, they are unlikely to return to the low levels seen at the beginning of 2025. In the long term, guided by national policies and with the leadership of large state-owned enterprises, sulfuric acid prices are expected to gradually return to a rational range.

Titanium Dioxide: Prices Rose First Then Fell in 2025, with Losses and Export Pressure Throughout the Year

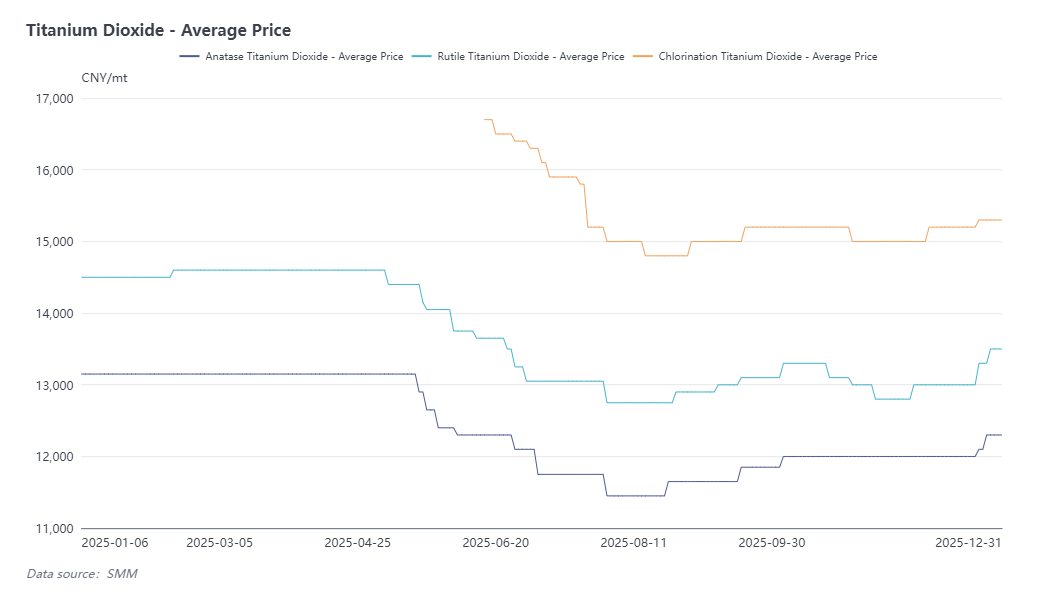

As of December 31, the domestic price of anatase titanium dioxide is quoted at 12,100–12,500 yuan per ton, with an average price of 12,300 yuan per ton, a decrease of 6.5% compared to the beginning of the year. The price of rutile titanium dioxide is quoted at 12,800–14,200 yuan per ton, with an average price of 13,300 yuan per ton, down 6.9% from the start of the year. The domestic price of chloride-process titanium dioxide is quoted at 13,600–17,000 yuan per ton, with an average price of 15,300 yuan per ton. This year, China's titanium dioxide production reached 4.178 million tons, a year-on-year decrease of 6.98%, while the production capacity expanded to 5.25 million tons, an increase of 6.84% compared to the previous year.

The titanium dioxide industry issued a cumulative total of seven price adjustment notices this year, but price and cost pressures continued to intensify. Specifically:

January–March: Prices Remained Stable

At the beginning of the year, titanium dioxide prices remained high, driven by strong domestic stocking demand and the anticipation of India imposing additional tariffs starting in April, which led to a significant rush in export orders. Meanwhile, maintenance work at some manufacturers before the Spring Festival resulted in supply contraction and continuous inventory reduction, prompting the industry to issue two rounds of price increase notices.

April–August: Accelerated Decline

Titanium dioxide production capacity continued to expand, but actual demand remained weak. Export markets saw price declines due to anti-dumping policies in multiple countries, while domestic terminal consumption remained sluggish. Many companies were forced to lower prices and initiate production cuts to alleviate high inventory pressure.

September–October: Slight Rebound

The traditional "Golden September and Silver October" peak season drove a temporary recovery in domestic demand, prompting titanium dioxide companies to issue two rounds of price increase notices aimed at halting the decline and stimulating the market. However, exports continued to be suppressed by anti-dumping policies in regions such as India, Brazil, and the European Union.

October–December: Weak Consolidation

Starting in October, a sharp rise in sulfuric acid prices led to losses across the entire sulfate-process titanium dioxide industry. Leading companies lowered their chloride-process product prices under competitive pressure, while overall market demand remained weak and competition intensified. As earlier production cuts and sales efforts progressed, industry inventory pressure eased somewhat. From late November, companies once again issued price increase notices to mitigate losses, followed by further price adjustments at the end of December to consolidate the gains.

In terms of product structure, the price gap between chloride-process and sulfate-process titanium dioxide continued to narrow this year. Meanwhile, the quoted price range for domestic chloride-process products significantly widened, with a notable divergence between high-end and mid-to-low-end product prices.

On whether chloride-process can form long-term competition with sulfate-process:

From a cost perspective, chloride-process technology has certain cost support, while sulfate-process currently relies on high sulfuric acid prices to maintain its quotations. If sulfuric acid prices gradually decline under policy regulation in the future, sulfate-process prices will also adjust downward. From a demand perspective, end-users' habits regarding product types are relatively stable, making a large-scale shift from sulfate-process to chloride-process unlikely in the short term, especially amid frequent price fluctuations. Existing sulfate-process users are unlikely to easily adjust their procurement structures. Overall, it is expected that the price gap between the two will remain stable or slightly widen in 2026.

From the export market perspective, the foreign trade situation was challenging this year. Major consumer countries such as India and the European Union continued to implement anti-dumping policies on titanium dioxide. To maintain export shares, companies often had to resort to methods such as rebates when selling to related end-users, significantly squeezing profit margins. Additionally, China's sulfate-process titanium dioxide faced intense competition in overseas markets, with quoted prices gradually being compressed.

In mid-December, India announced the cancellation of anti-dumping measures against Chinese titanium dioxide, providing positive support for exports to regions such as Southeast Asia and alleviating market pressure. Looking ahead to 2026, the titanium dioxide export industry is expected to continue its trend of survival of the fittest, with companies needing to consolidate their market shares and enhance competitiveness amid fierce competition.

In terms of prices, after a year of low-price operations, titanium dioxide prices saw a gradual increase in market optimism toward the end of the year, supported by the issuance of two rounds of price increase notices. Additionally, some regional companies are scheduled for pre-Spring Festival maintenance in January, with current production focused on fulfilling previous orders. After the Spring Festival, as demand recovers, titanium dioxide prices are expected to rise slightly. In the long term, sulfate-process product prices will still depend on raw material cost support, and terminal demand is unlikely to see significant growth. If raw material prices decline in the future, coupled with continuous industry capacity expansion, the titanium dioxide market may continue to operate at low levels with a weak trend.

III. Titanium Metal Market: Market Dynamics Amid Capacity Expansion and Structural Demand

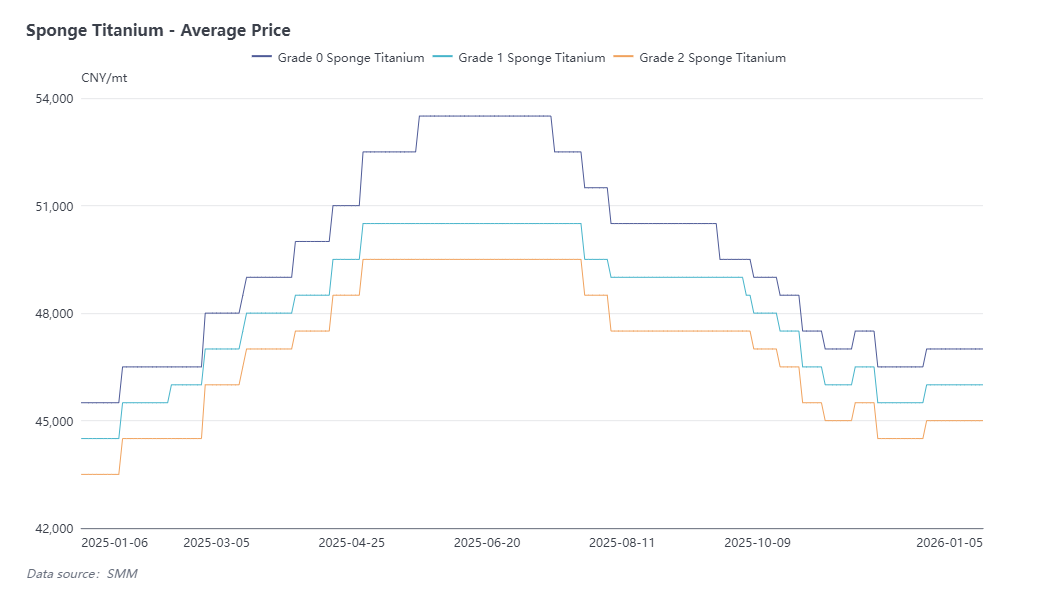

Sponge Titanium: Prices Rose First Then Fell, Consolidating Under Capacity Expansion and Export Constraints

As of December 31, the price of Grade 0 sponge titanium is quoted at 46,000–48,000 yuan per ton, an increase of 3.2% compared to the beginning of the year. China's annual sponge titanium production reached 270,000 tons, a year-on-year increase of 4.42%.

The price trend of the sponge titanium market throughout the year followed a pattern of rising first and then falling:

Accelerated Rise in the First Half:

Driven by the International Titanium Expo, demand experienced a temporary boost. Additionally, significant project growth in high-end sectors such as military and aerospace led to supply shortages, with enterprise inventories remaining consistently low.

Gradual Decline in the Second Half:

Demand in the civilian sector weakened, industry inventories gradually accumulated, and the traditional off-season further subdued market activity. Although some enterprises announced production controls in the third quarter, the actual demand response was limited, failing to reverse the downward trend. Simultaneously, foreign trade orders significantly decreased compared to the first half, collectively causing sponge titanium prices to continue adjusting downward. By the end of the year, the overall industry had entered a state of consolidation at low levels.

In 2025, the sponge titanium industry experienced significant capacity expansion. However, amid ongoing export restrictions on titanium products, the market supply-demand structure failed to improve correspondingly. As a result, sponge titanium prices have remained in a consolidation phase, supported primarily by cost factors.

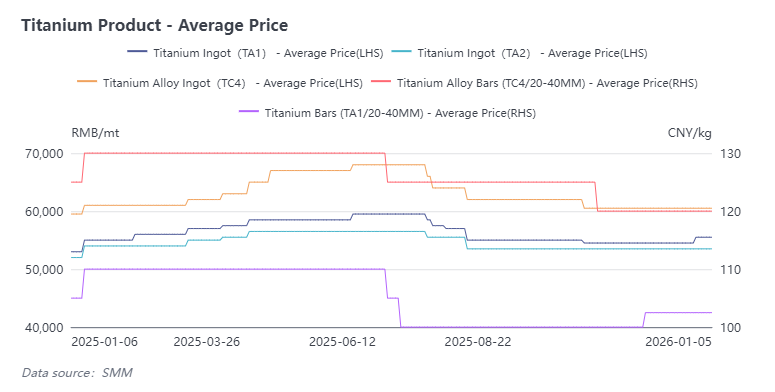

Titanium Materials: Structural Divergence in the Market with Strong High-End Demand but Pressure on Civilian and Export Sectors

As of December 31, the prices of major titanium material products are as follows: TA1 titanium ingot at 55–56 yuan/kg, TA2 titanium ingot at 53–54 yuan/kg, TC4 titanium alloy at 60–61 yuan/kg; hot-rolled titanium plate (3–8mm) at 62–63 yuan/kg, titanium welded pipe at 115–125 yuan/kg, pure titanium bar at 100–105 yuan/kg, and pure alloy bar at 115–125 yuan/kg.

This year, titanium material prices generally followed the trend of upstream sponge titanium, showing a pattern of rising first and then falling.

High-end market demand remained robust, particularly with significant growth in sectors such as military and aerospace. However, in civilian sectors such as chemical and marine equipment, project progress was slow, limiting demand release. Although the nuclear power sector holds some potential, its overall consumption remains relatively small, providing limited support to the market.

In terms of exports, the inclusion of titanium products in the dual-use items control list and strengthened customs enforcement have resulted in overall subdued performance in titanium material exports, without generating significant incremental growth.

On the cost side, rising tungsten prices toward the year-end led to price increases for processing tools such as drill bits, indirectly driving slight price increases for products like titanium plates.

Overall, the future trend of the titanium materials market will depend on the progress of civilian projects and the export policy environment. The market is currently in a consolidation phase, with significant breakthroughs unlikely in the short term.

![Titanium Concentrates Market Remains Weak, Raw Material Weakens, Titanium Dioxide Still Faces Downside Risks [SMM Titanium Spot Express]](https://imgqn.smm.cn/usercenter/XUnxM20251217171723.jpeg)

![China's Sulphuric Acid Market Continues Weakness; Price Hikes in Northeast China and Inner Mongolia Fail to Mask Overall Downtrend [SMM Sulphuric Acid Weekly Review]](https://imgqn.smm.cn/usercenter/HBsPu20251217171723.jpeg)

![[SMM Analysis] June Indonesia Sulphur and Sulphuric Acid Import and Export Data](https://imgqn.smm.cn/usercenter/EutUV20251217171724.jpeg)