As 2025 draws to a close, Indonesia’s nickel ore market remains characterized by tight supply and structural shifts. Despite downward pressure from weak downstream prices, the market has found a floor through stringent RKAB (Work Plan and Budget) controls and escalating production costs. The government’s intensified inspections and the transition toward a more restrictive 2026 quota system have effectively constrained raw material availability, preventing a total price collapse.

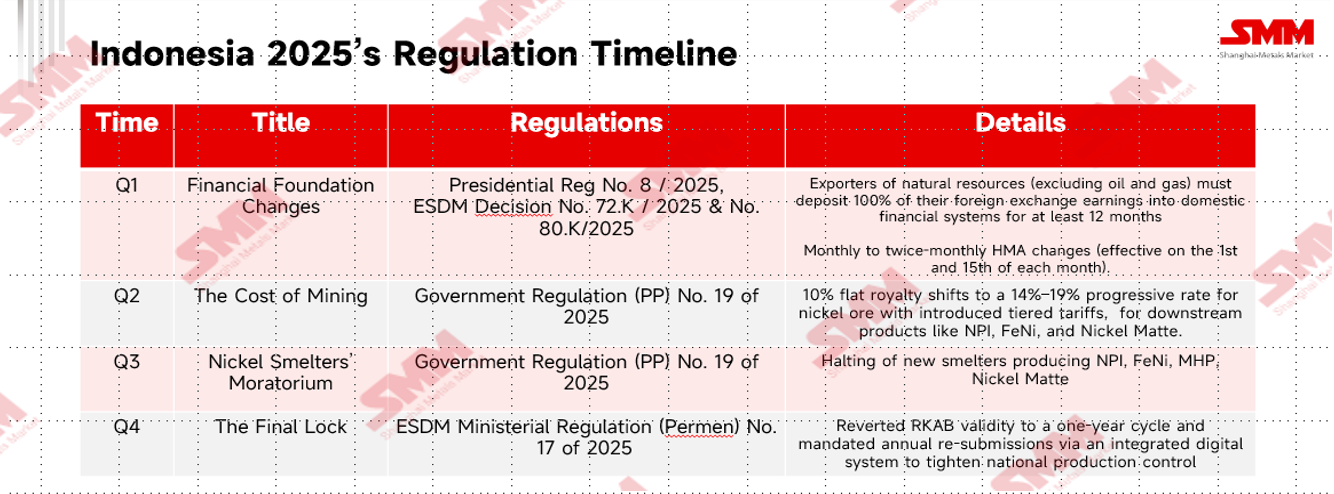

Section 1: The Regulatory "Squeeze" (The Indonesia Review)

In 2025, Indonesia reshaped its nickel sector into a high-value, digitally-controlled industry through four key strategic shifts, which includes:

In addition to this regulation, President Prabowo Subianto has intensified enforcement against non-compliant mines, with nickel operations becoming a key focus. Several companies have been sanctioned or temporarily sealed for forestry and permitting violations, while the Forest Area Enforcement Task Force (Satgas PKH) continues inspections across major mining regions to tighten oversight and control supply.

Section 2: Indonesian Nickel Ore Price and Supply Demand

In the first half of 2025, nickel ore prices were firmly supported by tight supply and strong restocking demand. Prolonged rainfall in Sulawesi and delays in effective RKAB quota execution restricted mine output, keeping saprolite supply particularly tight and pushing premiums to around $22/wmt in Q1, with prices continuing to rise into Q2. Limonite prices also strengthened early in the year, supported by limited spot availability and steady demand. On the demand side, Indonesian NPI smelters entered the year with low inventories and actively restocked after the Chinese New Year. The introduction of the semi-monthly HPM pricing system and the April implementation of higher progressive royalties further reinforced miners’ pricing power, lifting overall ore price levels in H1.

In the second half of the year, market conditions gradually shifted as RKAB quota revisions were increasingly approved, leading to a visible improvement in supply. Saprolite prices became more volatile rather than trending higher, with periodic support from smelter procurement, especially ahead of quota resets, but overall upside was capped as supply normalized. Limonite prices, by contrast, moved into a clearer downtrend throughout H2, as abundant supply from approved quotas met relatively flat downstream demand. As a result, while saprolite retained some structural support due to its tighter balance, limonite remained under sustained price pressure, defining a more polarized ore market in the second half of 2025.

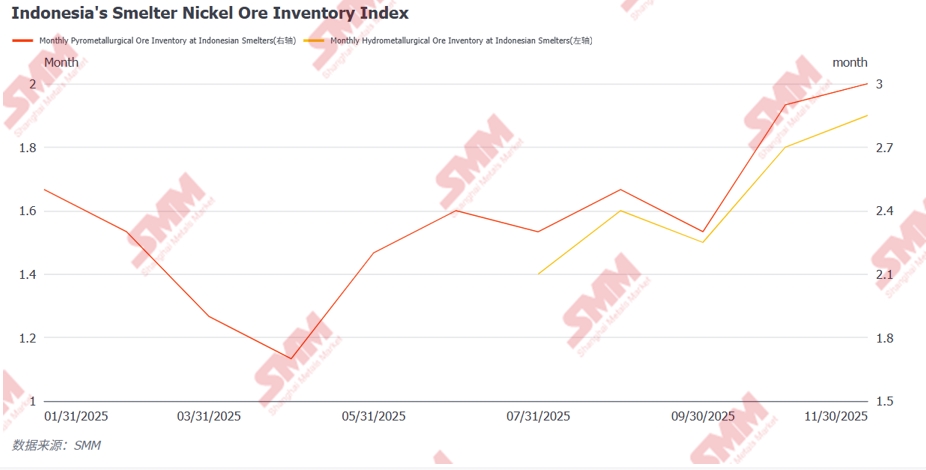

From a stockpiling perspective, RKEF smelters, remained under pressure for most of the year, with many holding less than two months of ore inventory. Elevated fuel costs and persistent logistical constraints further complicated restocking, and in some regions, procurement efforts were only partially successful. This supply tightness increased the urgency to secure cargoes, prompting buyers to accept higher prices during the quarter, even as overall inventories continued to trend lower on expectations of improved supply conditions in the following quarter. For HPAL smelters, the Then, it began to improve modestly in Q2 as most smelters stepped up replenishment efforts. Saprolite inventories bottomed out in April at around 1.7 months, prompting gradual restocking through May and June despite worsening cost inversion. In the second half of the year, ore inventories became more volatile but generally trended higher, driven by heightened procurement following news of the upcoming RKAB reset. Smelters accelerated stockpiling to hedge against rainy-season disruptions and the continued slow pace of RKAB approvals, providing intermittent support to procurement activity.

Section 3: Philippines Nickel Ore Price and Supply Demand

In 2025, Philippine nickel ore imports to Indonesia are projected to achieve a 14% year-on-year growth, reached approximately 15+ million tons, primarily driven by a surge in demand from Indonesian smelters for blending purposes. The annual price trend followed a "high-start, low-end" pattern. In Q1, prices peaked as Indonesian smelters increased imports from the Philippines to offset domestic supply shortages caused by RKAB quota delays and heavy rainfall in Sulawesi. This demand coincided with the Philippines’ own rainy season in Surigao, resulting in a supply-demand imbalance that pushed prices to their annual high. From supply perspective, first half of the year the import volume increases significantly and second half of the year showed a more stable By Q2, prices remained elevated despite increased Philippine output as the rainy season ended. This support came from a recovery in China’s NPI and stainless steel markets, alongside higher Indonesian production costs following the implementation of the PNBP policy. However, Q3 marked a significant price correction; Chinese demand for stainless steel underperformed during the "Golden September" period, and Indonesia released supplementary RKAB quotas, reducing the need for Philippine imports. In Q4, market activity slowed as smelters finalized winter stockpiling, leading to price stabilization within a narrow range.

Section 4: Outlook for 2026

In 2026, the Indonesian nickel ore market will navigate a complex balance between surging hydrometallurgical demand and tighter government supply controls. During the first half of the year, the market is expected to remain tight as the transition to the 2026 annual RKAB system typically causes administrative bottlenecks in Q1, potentially delaying full-scale mining approvals. This seasonal constraint is intensified by the ongoing rainy season in Sulawesi and Halmahera, which limits ore extraction and logistics. However, as the weather clears in Q2 and new quotas are gradually released, supply is expected to recover just as a wave of new projects, particularly MHP projects, which is ramping up their procurement activities, creating a strong demand floor.

The second half of 2026 will be defined by a "supply-demand resonance" as industrial capacity expands further. While Q3 may see another seasonal dip in production due to the returning rains, the government is likely to issue supplementary RKAB approvals for compliant miners who exhausted their initial quotas in the first half. Crucially, the Indonesian government has signaled a plan to reduce the total 2026 quota to prevent global oversupply and stabilize prices. This policy, combined with declining average ore grades that require higher volumes of feed, will likely keep nickel ore prices elevated and volatile as the year closes with even more smelters entering full operational status.