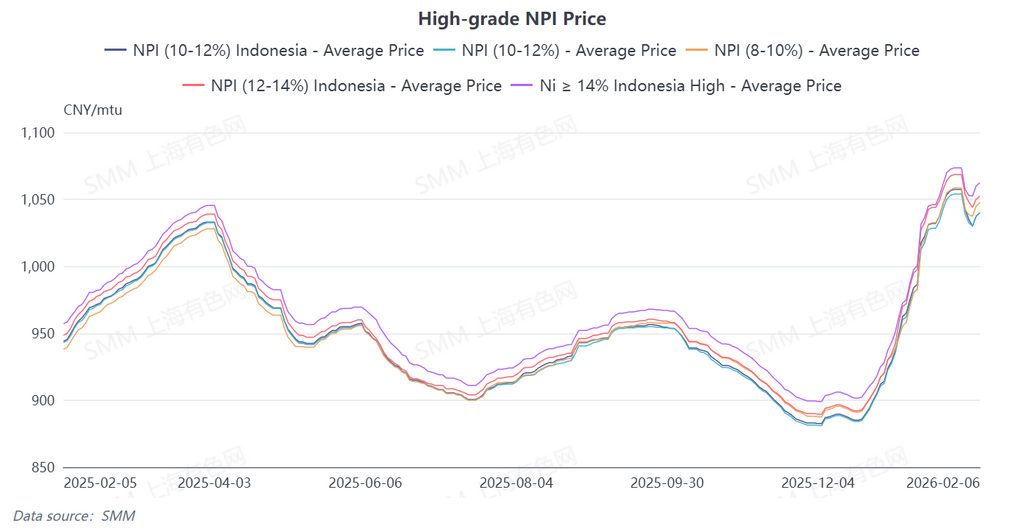

The average price of SMM 10-12% high-grade NPI fell 17.2 yuan/mtu WoW to 1,035.8 yuan/mtu (ex-factory, tax included), while the average Indonesian NPI FOB index price dropped $2.06/mtu WoW to $131.2/mtu. At the beginning of the week, futures hit limit-down, nickel prices fell sharply WoW, triggering low-priced sales of arbitrage materials in the market and causing a notable decline in high-grade NPI prices.

Supply side, the sharp drop in futures at the start of the week led to sell-offs to lock in spread profits, resulting in a short-term price collapse for high-grade NPI. However, supported by costs, upstream pig iron producers' offers remained firm. Demand side, influenced by trader sell-offs, downstream steel mills' purchasing intention prices were suppressed. Additionally, with the Chinese New Year approaching, market activity was already very sluggish. Overall, this week, the sharp decline in futures triggered arbitrage-related sell-offs, leading to a noticeable drop in high-grade NPI prices. However, after the sell-off subsided, supported by costs, upstream offers and the market center gradually returned to normal. Looking ahead, as the Chinese New Year holiday approaches, the market is expected to be quiet, with high-grade NPI prices likely to hover at highs without significant fluctuations.

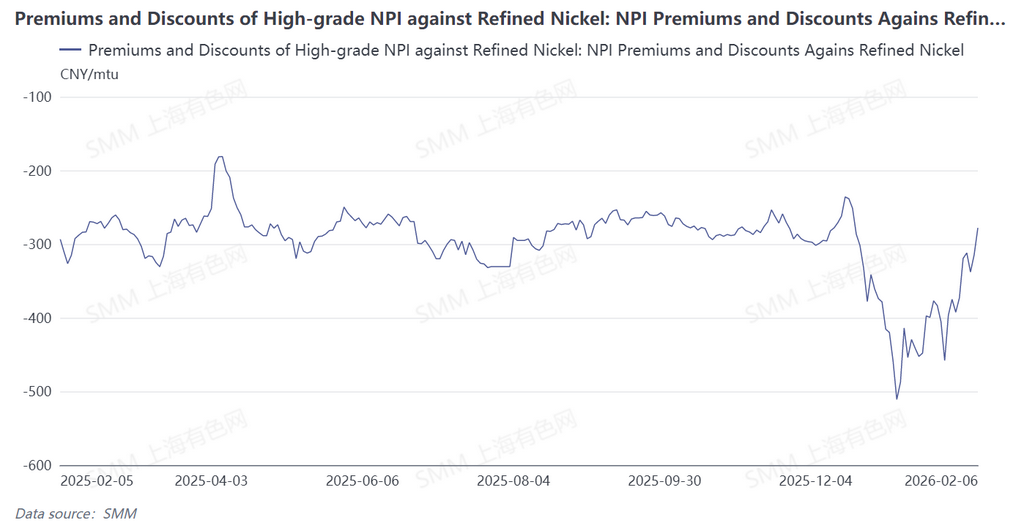

This week, refined nickel prices fell sharply, and high-grade NPI prices also declined WoW. The average discount of high-grade NPI to refined nickel narrowed to 312.4 yuan/mtu. Next week, high-grade NPI prices are expected to fluctuate at highs, while the average refined nickel price is anticipated to pull back. The average discount of high-grade NPI to refined nickel is expected to widen, maintaining the driving force for converting NPI to high-grade nickel matte.

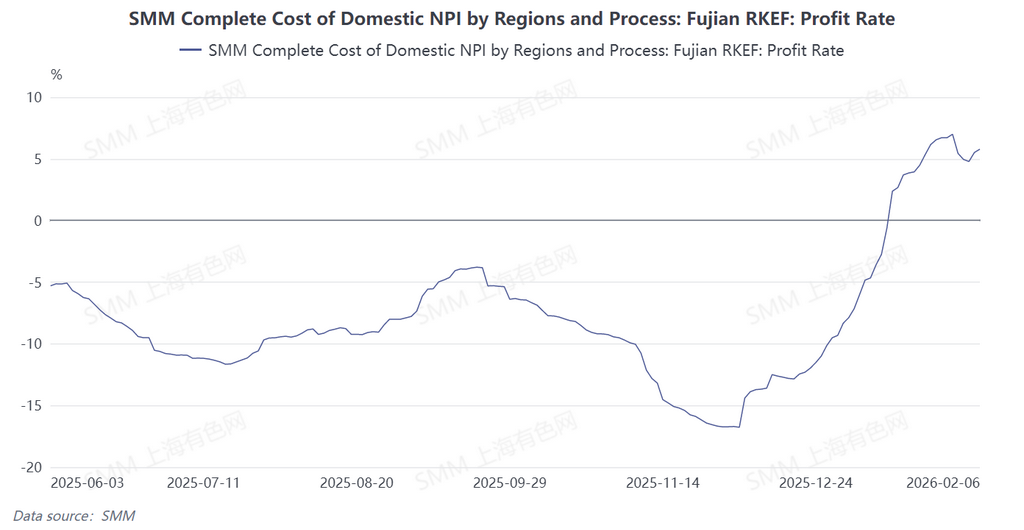

Based on nickel ore prices from 25 days ago for calculating the cash cost of high-grade NPI, smelter profits remained high this week. However, from the current raw material perspective, both Philippine and Indonesian ore prices increased, while auxiliary material prices edged down. The current ore cash production cost for high-grade NPI rose, and high-grade NPI prices saw some pullback, making sustained improvement in smelter profits difficult. Looking ahead to next week, on the raw material side, with ore prices rising and auxiliary material prices relatively flat, smelters are expected to face some cost pressure.