[SMM New Energy] As one of the most critical base metals in the new energy industry chain, lithium plays a vital role in power battery and energy storage systems. From lithium carbonate and lithium hydroxide to downstream ternary and LFP materials, and further to battery cells and EV installations, price fluctuations directly impact the cost structure of the entire new energy industry. Recently, price volatility in lithium carbonate and lithium hydroxide reflects multiple dynamics within the industry chain during its adjustment phase.

I. Upstream: Lithium Resource Extraction and Primary Processing

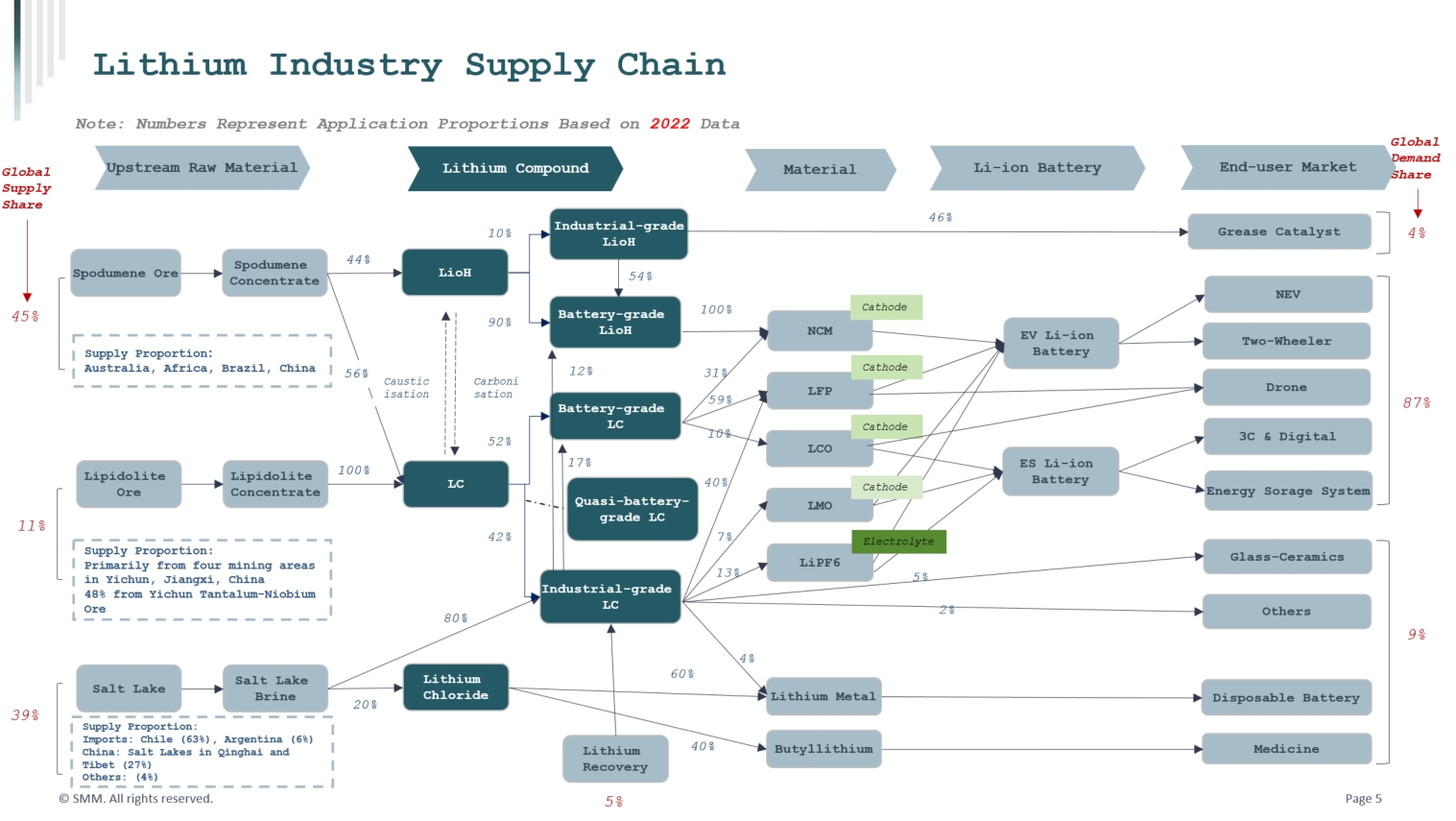

Diagram 1: Lithium Industry Chain

Lithium resources are mainly categorized into three types: spodumene, lepidolite, and salt lake brine. Spodumene resources are primarily distributed in Australia, Africa, and China; lepidolite is highly concentrated in Jiangxi, China; while salt lake brine is mainly found in the "Lithium Triangle" in South America and regions of China. Overall, global lithium resources exhibit a supply-demand pattern characterized by multiple sources and significant grade variations. With the growth in new energy demand, upstream resource competition has intensified. Global lithium mine projects are successively advancing capacity expansions, but construction progress and regulatory environments vary significantly across regions. China holds structural advantages in the industry chain, with approximately 70% of global lithium carbonate smelting capacity and nearly 90% of market demand located in China. Whether in terms of capacity scale, market liquidity, or spot pricing, China maintains an edge.

II. Midstream: Smelting and Processing System: Capacity Expansion and Slow Globalization

Lithium chemicals are a key link connecting the resource end to the material end, including products such as lithium carbonate and lithium hydroxide. Recently, midstream smelters have maintained high operating rates, mainly driven by cost-side pressures, enterprise order structures, and fluctuating upward market prices. Although China remains the dominant producer of lithium chemicals, the trend of industry chain expansion is becoming increasingly evident, with lithium chemical smelting projects planned in regions including Southeast Asia, the Middle East, and South America. However, overseas projects generally face challenges such as long construction cycles, difficult engineering management, and insufficient supporting systems, resulting in commissioning progress significantly slower than expectations and failing to form new supply competitive with China in the short term. On the price front, the lithium chemicals market is in a state of considerable fluctuation with an upward trend, primarily influenced by stronger-than-expected demand.

III. Application-Side Demand: Power Battery Slowdown, Energy Storage as Main Increment

Downstream applications of lithium mainly include power batteries, ESS batteries, and consumer electronics, but the demand structure has been quietly changing in recent years. As the global EV industry growth slows, traditional power battery demand is marginally weakening, while the energy storage sector is rapidly emerging as another core driver boosting lithium demand. Large-scale tenders for ESS power stations, power grid-side frequency regulation needs, and the popularization of distributed energy storage continue to boost demand for lithium carbonate and LFP materials. Driven by the "dual carbon" goals, increasing green electricity proportions, and power system flexibility requirements, the energy storage industry exhibits far weaker cyclicality than power batteries, with more stable growth, fundamentally supporting the long-term certainty of the lithium industry chain.

IV. Supply-Side Pattern

Supply side, upstream lithium mine expansion cycles are long, while midstream lithium chemical capacity distribution is gradually extending from China to overseas regions, such as the Middle East, Australia, and North America, which are adding new refining capacity to enhance local supply security. Demand side, global battery manufacturing shows a multi-polar trend, with Asia maintaining leadership while EV battery plant construction speeds up in Europe and the US, driving urgent demand for stable lithium chemical supply chains.

V. Conclusion

The lithium industry chain is in a critical period of global energy transformation. With rapid expansion in energy storage demand, continued upstream resource development expansion, and accelerated global layout of midstream smelting structures, lithium's strategic role in the new energy system is becoming increasingly evident. In the short term, prices may fluctuate due to market sentiment, inventory pace, and supply disruptions. However, from a long-term perspective, lithium's resource value, technological attributes, and industry chain synergy will further strengthen. In the future, as overseas capacity gradually comes online, material systems evolve, and energy storage demand continues to grow, the global lithium industry chain will maintain resilient expansion, reshaping the supply-demand pattern and competitive landscape with deeper globalization.