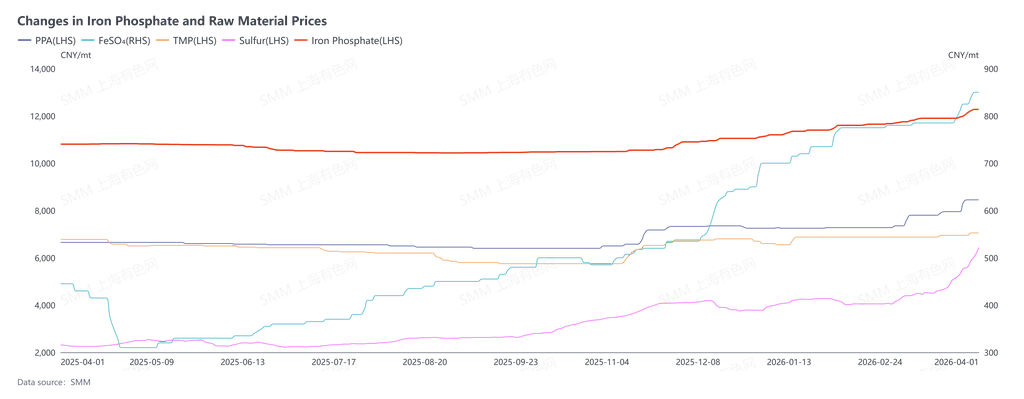

Starting from March 25, iron phosphate began executing orders for the April delivery cycle. This month’s order negotiations were now at their most intense stage. Mainstream quotations from iron phosphate enterprises had already reached 13,000 yuan/mt, up more than 1,000 yuan in a single month. Downstream LFP enterprises showed clear divergence in attitude: some, in order to secure supply, could still accept the price increase; others repeatedly pushed for lower prices and refused to budge. According to SMM statistics, as of April 1, the average price of iron phosphate stood at 12,275 yuan/mt. Although the 13,000 yuan/mt level had not yet seen much volume, 12,000 yuan/mt had already been crossed quickly, and 12,500 yuan/mt might not hold for long. Prices were moving step by step toward the 13,000 yuan/mt threshold. The direct trigger for this round of price increases was that geopolitical conflicts pushed up sulfur prices, causing iron phosphate raw material prices to rise sharply, with further upward momentum still in place. But fundamentally, the tug-of-war over pricing power was a reshuffle of the rules for profit distribution across the industry chain after the reversal in the supply-demand pattern.

Changes in Iron Phosphate and Raw Material Prices

Some voices in the market simply attributed this price increase to raw material cost push, but this view was clearly superficial. It was undeniable that rising prices of key raw materials such as phosphorus sources, iron sources, and hydrogen peroxide did raise the production cost of iron phosphate and formed the basis for higher prices, but this was by no means the core logic of the current negotiation game.

What truly dominated this game was the qualitative change in the supply-demand pattern since 2025 under the industry’s anti-involution backdrop, and the resulting transfer of pricing power: from the downstream’s one-way dominance over the past many years to a gradual tilt toward the upstream. This was the inevitable result of spontaneous market adjustment and also a real-world manifestation of Nash equilibrium in industry chain competition.

Looking back from 2023 to 2025, the iron phosphate industry went through a three-year period of deep losses. Most small and medium-sized enterprises were forced to exit the market due to losses and broken cash flow, and the industry completed a brutal round of capacity rationalization (of course, LFP enterprises, except for one or two top-tier enterprises, also suffered deep losses across the board). This rationalization was not the result of policy intervention, but rather a spontaneous correction by the market’s “invisible hand” to long-distorted supply and demand.

By the end of 2025, the iron phosphate supply side had taken the lead in entering a tight balance marked by low inventory and low redundancy, while downstream LFP enterprises were still continuing their previous expansion inertia of “large capacity and scrambling for market share.” This shift in the balance of supply and demand directly gave iron phosphate enterprises unprecedented bargaining power: upstream enterprises that once could only passively accept downstream price suppression and were reduced to “processing workshops” finally gained the confidence to negotiate with downstream players on equal footing.

The deadlock in this round of negotiations centered on two core contradictions, and these two contradictions precisely exposed the strategic dilemma and double standards of downstream LFP enterprises.

The first contradiction was the downstream’s double standard in judging “cost pass-through.”

At present, the core reason some LFP enterprises resisted iron phosphate price increases was that “the price increase of iron phosphate under some processes exceeded the increase in raw material costs,” and they therefore considered the increase unreasonable. But looking back over the past three years, when iron phosphate enterprises were generally trapped in a situation where production costs exceeded selling prices and every ton sold meant a loss, downstream enterprises never voluntarily gave up profits because of upstream losses. Instead, they continuously pushed for lower prices and enjoyed the dividends brought by low-cost raw materials. At that time, cost pressure was borne solely by iron phosphate enterprises, and no one paid for their losses; now, with supply and demand roles reversed, upstream enterprises were raising quotations on the strength of a tight balance, yet downstream players suddenly used “cost increases” as a bargaining chip to cut prices. This rule that is applied only when it benefits oneself is essentially a disregard for market pricing logic. In a market economy, pricing has never been a simple “cost addition,” but a revaluation based on supply-demand scarcity. Current upstream quotations were essentially a reasonable repair of losses over the past three years, not “excess profiteering.”

The second contradiction was the irrationality of downstream players passing their own structural losses upstream.

In negotiations, LFP enterprises repeatedly emphasized that their own price increases to downstream battery enterprises were not going smoothly, attempting to pass these “front-line defeats” on to upstream iron phosphate enterprises. But deeper analysis showed that the continued losses of some LFP enterprises were rooted not in upstream price increases, but in their own strategic mistakes and cut-throat competition. On the one hand, disorderly expansion of LFP capacity led to oversupply, allowing terminal battery cell enterprises, with ample supplier choices, to enjoy strong room for price cuts. On the other hand, although the state had repeatedly emphasized anti-involution, some LFP enterprises still chose low-price strategies to “transfuse” battery cell enterprises in order to seize market share, exchanging short-term losses for scale and hoping to recover losses in the future through economies of scale.

Losses caused by such strategic mistakes should not become a reason to suppress upstream prices. The core of healthy industry chain development is that all links can obtain reasonable profits and form a virtuous cycle. If LFP enterprises wanted to change their loss-making predicament, the correct path was to unite and fight for reasonable price increases from terminal battery cell enterprises, so as to achieve effective cost pass-through downstream, rather than shifting the pressure of involution upstream. Continuing to squeeze iron phosphate enterprises, which had already endured three years of losses and had only just regained bargaining power, would not only undermine the stability of the upstream supply chain, but would ultimately backfire on their own supply chain security.

From the perspective of Nash equilibrium, the current game in the iron phosphate industry chain was at a critical stage of non-cooperative competition: unilateral toughness or concession by any party could not achieve the global optimum. Iron phosphate enterprises holding prices firm were not seeking windfall profits, but repairing balance sheets severely damaged over the past three years and returning to a reasonable industry profit range. If LFP enterprises continued to cling to double standards and tried to make up for their own mistakes by squeezing the upstream, they would only fall into a vicious cycle of “upstream supply contraction and further cost pressure on the downstream.”

The deadlock in April negotiations marked the formal entry of the iron phosphate industry chain into a new stage of multi-party competition.

The reversal of pricing power was not accidental, but an inevitability under market laws and a correction of the distorted pricing mechanism of the past many years. For the entire new energy industry chain, abandoning the double-standard cost logic, stopping the transfer of losses from failed competition upstream, facing up to changes in the supply-demand pattern, and jointly building a pricing mechanism based on supply-demand balance and reasonable profits are the only way to break the current deadlock and achieve a win-win outcome across the industry chain. For iron phosphate enterprises, however, the current return of bargaining power was only the beginning. How to maintain the advantage of tight supply and demand and achieve sustained profit recovery would remain the core issue to face in the future.

Note: If you have any additions or corrections to the details mentioned in this article, please feel free to contact us at any time. Contact information is as follows:

Tel: 021-20707860 (or add WeChat 13585549799) Yang Chaoxing, thank you!