On 24 September 2025, Freeport announced output cuts at its Grasberg copper concentrate project in Indonesia due to force-majeure factors — one of the most market-moving shocks to the copper complex this year. The company also lowered its production guidance for 2025 and 2026, prompting sharp market attention and pushing LME copper up ~3.5% that day. By 25 September 2025, LME copper hit a year-to-date high of $10,485/tonne. Below is a brief analysis of the impact of the Grasberg production cut on the electrolytic/ refined-copper market.

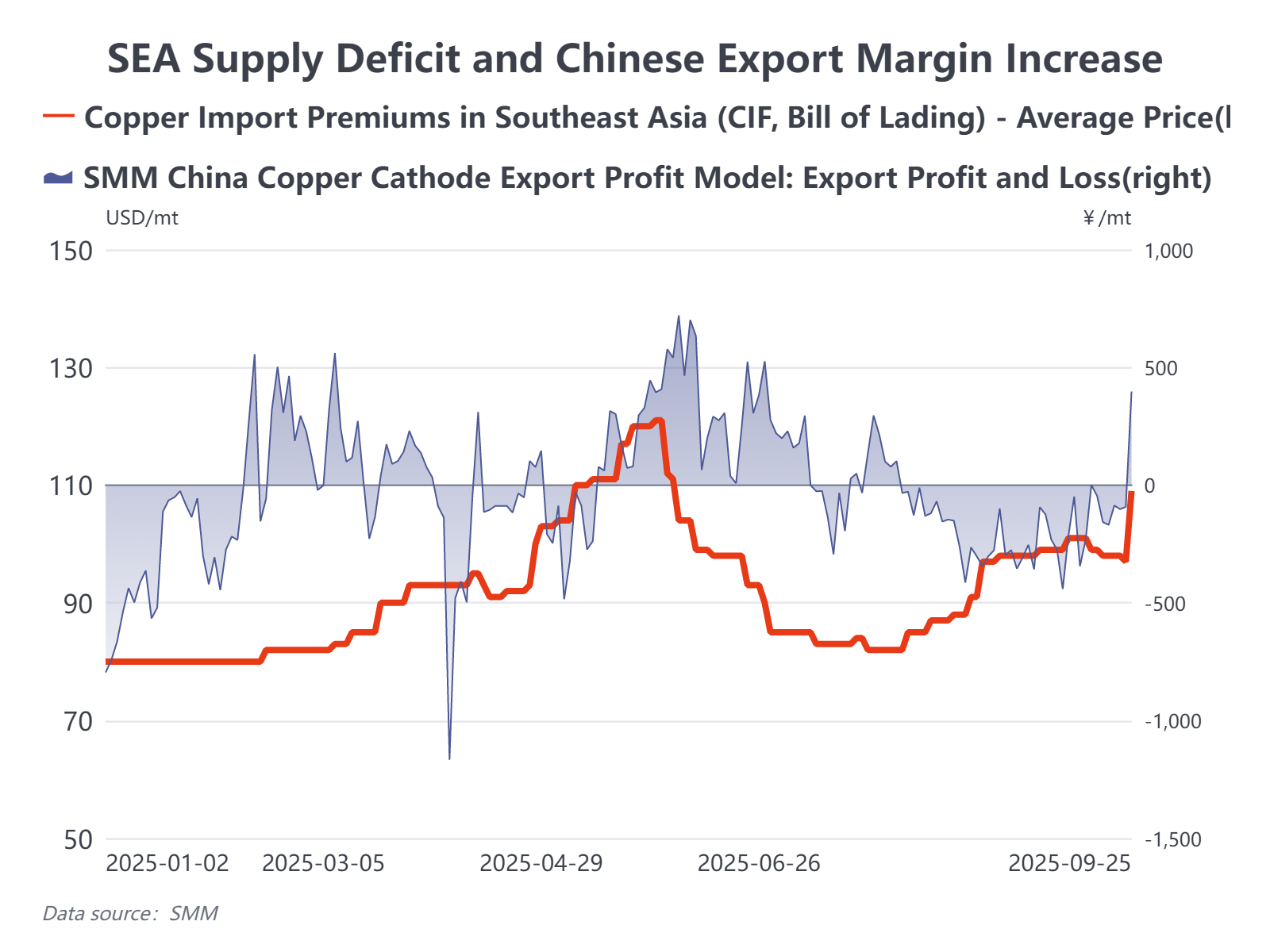

1. Southeast Asia supply hit further — spot premiums likely to reach YTD highs

Freeport said the force majeure will reduce Grasberg’s remaining 2025 output by 250,000–260,000 tonnes, and cut full-year 2026 guidance by roughly 270,000 tonnes. In aggregate, this implies about 500,000 tonnes of lost copper over the next 12–15 months. Although Freeport expects a phased recovery from 2027, it also warned of a potential additional loss of 100,000–200,000 tonnes. Grasberg is a major feed source for Indonesian smelters Gresik and Manyar. SMM estimates the disruption could reduce Indonesian refined-copper output in Q4 2025 by roughly 40,000 tonnes per month, much of which had been earmarked for long-term contracts serving the Southeast Asian market. Since the PSR smelter shutdown earlier this year, Southeast Asian refined-copper supply has already been very unstable; this event further disrupts an already fragile supply chain, and regional premiums have clearly risen.

2. Chinese import margin increase— but profit is limited

Domestic consumption in September did not show a material uplift and the National Day holiday is approaching. The price spike opened an export window from a pure arbitrage perspective, and some smelters may be motivated to export short-term. However, the lack of preferential tax exemption/offsets (and the structure of export tax/rebate mechanics) compresses export profitability after the recent rapid price rise. Using prior ore purchase assumptions around $9,900–10,000/tonne, additional tax/fee impacts amount to roughly RMB 500/tonne, meaning export margins are not as attractive as headline prices suggest. SMM expects some smelters to export refined copper in October to help filling Southeast Asian shortfalls, but volumes are likely to be limited.

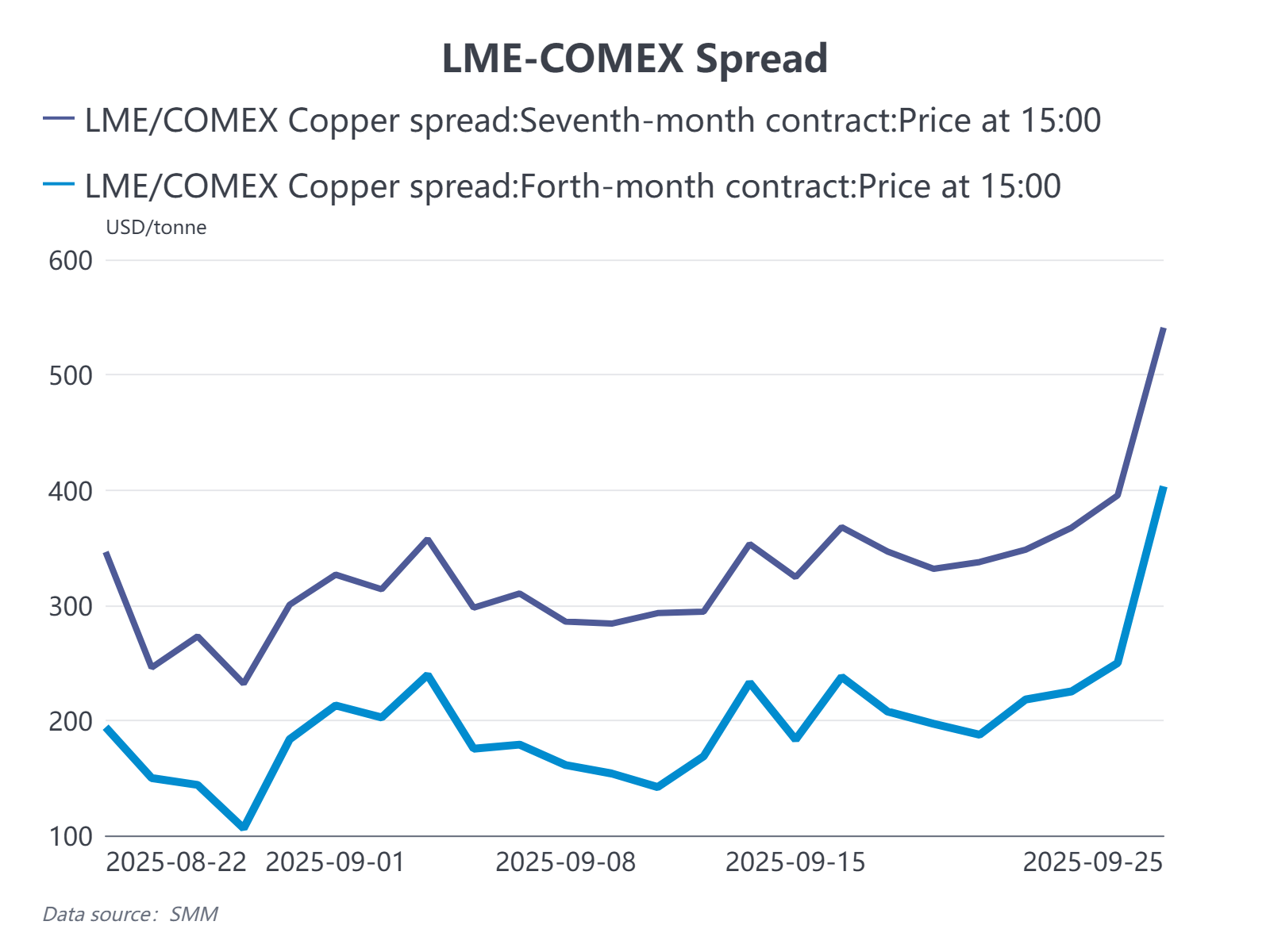

3. LME contango narrows; CL forward spreads widen

With tighter supply in Asia, LME inventories are likely to fall and the spot–forward (contango) structure should narrow. That said, with current LME stocks still around ~200,000 tonnes, and assuming Southeast Asia is partially replenished by Chinese exports at a monthly shortfall of 20–30 kt, the LME curve is unlikely to see an extreme shift within the year. However, attention should be paid to the existing LME–COMEX far-date spread (now roughly $500–600/tonne), as some traders are combining the current supply-tight logic with expectations of potential future U.S. tariffs on copper. This implies a non-zero probability of extreme structural moves across LME, SHFE–LME and COMEX–LME in Nov–Dec 2025.

4. Annual long-term contract negotiations are forced to accelerate

Overall, Asian copper supply will face episodic tightness in Q4. Production cuts in Africa and Indonesia have materially disturbed an already fragile refined-copper flow, and regional premiums are likely to continue rising. The event also puts renewed pressure on the already complex 2026 long-term contract negotiations — African long-term talks may begin as early as late September, and competition for long-term imports from Japan, Korea and South America is expected to intensify this year. On balance, 2026 benchmark long-term prices for Asia look set to move higher relative to 2025.

Outlook: Many of the strategic contests remain unresolved, but 2026 is shaping up to be another year of tight resource allocation. Regional trade fragmentation raises supply-security pressure, and by the year-end long-term negotiations, premiums priced into 2026 are expected to be higher than those for 2025.