1 July TItanium Dioxide Market Review

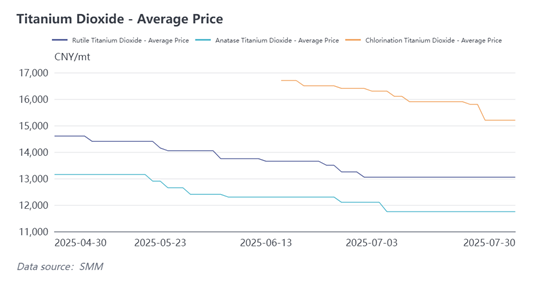

1.1 Price of Sulfate Process Stabilizes While Chloride Process Faces Downward Pressure

In July, the domestic titanium dioxide market price showed significant divergence. After two months of continuous decline, the price of sulphuric acid-based products stabilized this month, entering a low-level consolidation phase. Specifically, the quoted price range for rutile-type titanium dioxide remained between 12,500-13,600 yuan/tonne, with the mainstream market transaction price stabilizing at approximately 13,200 yuan/tonne. Some long-term cooperative customers may be eligible for additional price discounts. In terms of exports, FOB quotes continued to decline, with the mainstream transaction range dropping to 1,825–1,875 $/tonne. Rutile-type product quotes remain within the 11,500–12,000 yuan/tonne, with the mainstream transaction price at approximately 11,800 yuan/tonne.

Chlorination-processed titanium dioxide prices saw a significant decline in July. Current market quotes range from 14,500-15,900 yuan/tonne, with the mainstream transaction price having fallen below the 15,000 yuan/tonne threshold. Export quotes have also dropped to 2,050–2,200 $/tonne, with the mainstream transaction price having fallen below the 2,100 $/tonne threshold. This phenomenon is primarily attributed to two factors: on the one hand, domestically produced chlorination-based products remain positioned in the mid-to-low-end segment of the international market, facing intense price competition; on the other hand, newly added domestic production capacity is gradually coming online, further intensifying market competition pressure. Notably, domestic market acceptance of domestically produced chlorination-based products is gradually improving, with some companies beginning to explore the possibility of replacing imported products with domestic alternatives.

1.2 Production Cuts Continue with Initial Inventory Relief

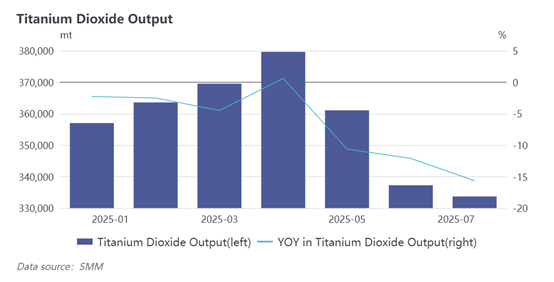

According to SMM data, Chinese titanium dioxide production decreased by 1.06% month-on-month in July 2025. This month, titanium dioxide manufacturers continued to maintain their production cutback strategy to address the ongoing decline in market demand. By actively adjusting production capacity, they effectively alleviated inventory pressure. Some manufacturers that had previously suspended production have planned to resume operations gradually next month. Currently, production primarily focuses on ensuring the fulfilment of long-term contracts with core existing customers. Inventory levels across manufacturers are generally maintained at a reasonable level of approximately one month, achieving a basic dynamic balance between production and sales. Notably, some large enterprises have initiated routine maintenance plans this month, further tightening market supply. On the demand side, the coatings industry's overall performance has continued to fall short of expectations, compounded by the traditional summer off-season, resulting in generally low terminal procurement intentions. The market generally expects the recovery in market conditions to be delayed until September.

1.3 Declining Overseas Orders Reshape Competitive Landscape

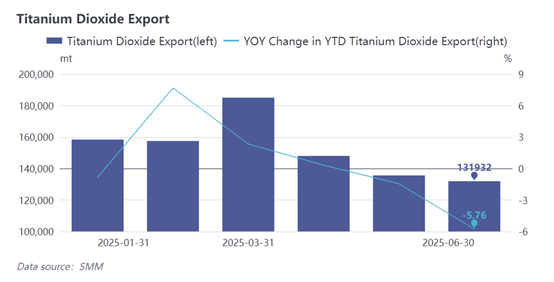

The titanium dioxide export market continues to face sustained pressure. In June, titanium dioxide exports totalled 131,932 tonnes, with cumulative exports for the first half of the year declining by 5.76% year-on-year. Due to the impact of U.S. tariff hikes and anti-dumping policies, demand in traditional export markets has significantly contracted. Currently, the export market is primarily dominated by large manufacturers, with export opportunities for small and medium-sized manufacturers continuing to shrink. Against this backdrop, the Southeast Asian coatings market has become a key focus area for manufacturers, and future export trends will largely depend on the success of efforts to expand into emerging markets.

2 July TItanium Sponge Market Review

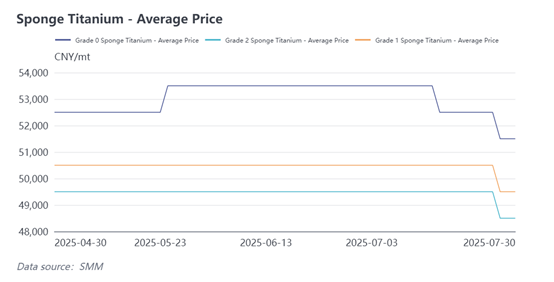

2.1 Prices Retreat from Highs as Market Pressure Builds

In July, the sponge titanium market ended its previous upward trend, with prices showing a downward trend from high levels. Latest market data shows that prices for mainstream product grades have generally decreased. The quoted price range for Grade 0 sponge titanium is 50,000–53,000 yuan/tonne, Grade 1 products are quoted at 49,000–50,000 yuan/tonne, and Grade 2 products are quoted at 48,000–49,000 yuan/ tonne. The average price across all product categories has decreased by approximately 2,000 yuan compared to the previous month. The price correction is primarily influenced by two factors: on one hand, the traditional summer off-season effect has become evident, with market procurement activity significantly slowing down; on the other hand, demand for titanium materials from downstream industries such as chemicals and construction has continued to shrink, leading to severe shortages of orders for titanium material processing companies. Against the backdrop of weak terminal demand, industry competition has intensified, and coupled with the continued expansion of sponge titanium production capacity, downward price pressure is gradually being transmitted upstream.

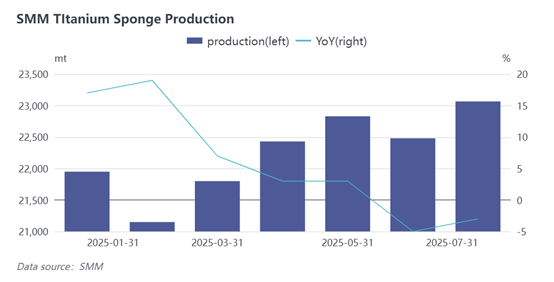

2.2 High Production Levels Persist Amid Policy-Led Capacity Rationalization

According to SMM data, Chinese sponge titanium production increased by 2.61% month-on-month in July 2025. This month, the sponge titanium market has remained stable in terms of production, but due to the continued rise in prices, the industry's production capacity is still expanding this year. Currently, it is the traditional summer off-season, and downstream procurement has slowed down, with the market supply and demand situation gradually shifting to a surplus. According to the latest SMM survey, in response to the industry's anti-overcapacity policy direction, some major manufacturers have planned to implement a 30% production cut in the third quarter, with market supply expected to significantly contract in August. Currently, the industry's overall inventory levels continue to rise, and this proactive production cut is expected to accelerate inventory digestion, creating favourable conditions for price stabilisation and recovery in the future.

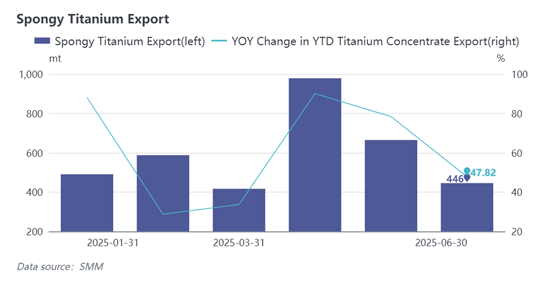

2.3 Export Dip Underlines Structural Adjustment Imperative

In June, exports of sponge titanium amounted to 446 tonnes, marking a significant month-on-month decline of 32.93%. However, cumulative exports for the first half of the year still maintained a year-on-year growth rate of 47.82%. It is worth noting that, compared to domestic production capacity, direct exports of sponge titanium have consistently remained at a relatively low level. This is primarily because downstream users typically prefer to directly import finished titanium products rather than smelting sponge titanium themselves. Additionally, overseas markets have stringent import standards for sponge titanium, which also limits export volumes to some extent. In contrast, exports of finished titanium products continued to grow slightly in June, indicating better acceptance in international markets.