SMM July 17 news:

Metal market:

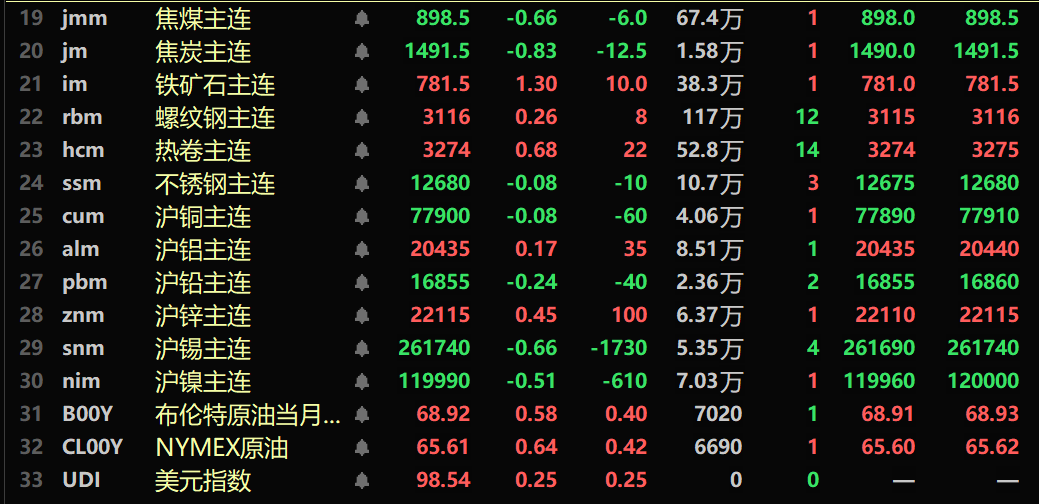

By midday close, base metals in the domestic market mostly fell, with SHFE nickel down 0.51%, SHFE aluminum up 0.17%, SHFE copper down 0.08%, SHFE lead down 0.24%, SHFE zinc up 0.45%, and SHFE tin down 0.66%.

Additionally, the most-traded cast aluminum futures rose 0.15%, while the most-traded alumina futures dropped 2.39%. Lithium carbonate fell 0.36%, silicon metal was flat at 8,680 yuan/mt. Polysilicon gained 4.03%.

Ferrous metals series showed mixed performance, with iron ore up 1.3%, rebar and HRC rising 0.26% and 0.68% respectively. Stainless steel edged down. For coking coal and coke, coking coal declined 0.66% and coke dropped 0.83%.

In overseas markets, as of 11:47, LME metals mostly fell, with LME copper, LME lead and LME zinc slightly down, all within 0.1%. LME aluminum dipped 0.1%. LME tin rose 0.23%. LME nickel gained 0.23%.

For precious metals, as of 11:47, COMEX gold fell 0.38%, COMEX silver rose 0.26%. Domestically, SHFE gold edged up 0.01, SHFE silver increased 0.17%.

By midday close, the most-traded Europe container shipping futures contract dropped 5.32% to 1,561.4 points.

As of 11:47 July 17, some futures midday quotes:

》SMM metal spot prices on July 17

Spot and fundamentals

Copper:Today, spot #1 copper cathode in Guangdong traded at a premium of 30-100 yuan/mt against the front-month contract, averaging 65 yuan/mt, up 5 yuan/mt from the previous day. SX-EW copper was quoted at a discount of 30-10 yuan/mt, averaging 20 yuan/mt, up 10 yuan/mt. The average price of #1 copper cathode in Guangdong was 77,965 yuan/mt, down 105 yuan/mt, while SX-EW copper averaged 77,880 yuan/mt, up 100 yuan/mt. Spot market: Guangdong inventory rose again, mainly due to low outflows from warehouses. Copper prices continued to pull back with warrants still not released, leaving limited spot cargo available...》Click for details

Macro front

Domestic:

[PBOC injects net 360.5 billion yuan via open market operations]The PBOC conducted 450.5 billion yuan of 7-day reverse repo operations at 1.40%, unchanged from previous operations. With 90 billion yuan of 7-day reverse repos maturing today, it resulted in a net injection of 360.5 billion yuan.

[Beijing's GDP grows 5.5% YoY in H1]Beijing held a press conference on its economic performance in H1 2025. It is reported that in the first half of the year (H1), the city achieved a regional gross domestic product (GDP) of 2,502.92 billion yuan, representing a year-on-year (YoY) increase of 5.5% at constant prices. According to the analysis of the Beijing Municipal Bureau of Statistics, the city's economy operated steadily and improved in the first half of the year. At the meeting, the Beijing Municipal Bureau of Statistics and the Beijing Survey Team of the National Bureau of Statistics (NBS) also released multiple economic data. In the first half of the year, the added value of industries above designated size in the city increased by 7.0% YoY at comparable prices, 0.2 percentage points higher than that in the first quarter. The added value of the tertiary industry in the city increased by 5.6% YoY at constant prices, 0.2 percentage points higher than that in the first quarter. In the investment and consumption sectors, the total fixed asset investment (excluding rural households) in the city increased by 14.1% YoY in the first half of the year. The total market consumption in the city increased by 0.9% YoY, with total retail sales of consumer goods reaching 673.42 billion yuan, a year-on-year decrease of 3.8%, while service consumption increased by 4.7% YoY.

US dollar:

As of 11:47, the US dollar index rose by 0.25% to 98.54. US President Trump stated that there was a "very slim chance" of removing Fed Chairman Powell from his position, following which market tensions eased and the US dollar rebounded. US data showed that producer prices in June remained unexpectedly flat, as price increases in goods due to import tariffs were offset by weakness in services. The Beige Book released by the Federal Reserve on Wednesday indicated that economic activity had increased in recent weeks, but the outlook was "neutral to slightly pessimistic," with US companies reporting upward pressure on prices due to higher import tariffs. In trade, a spokesperson for the European Union (EU) stated that EU Trade Commissioner Maros Sefcovic would head to Washington on Wednesday for tariff negotiations and would also meet with US Secretary of Commerce Lutnick and Trade Representative Greer.

Data:

Today, data such as the UK's May unemployment rate (ILO standard), the UK's May average annual wage rate including bonuses for three months, the eurozone's June harmonized CPI annual rate (unadjusted final value), the eurozone's June core harmonized CPI annual rate (unadjusted final value), the US's June import price index monthly rate, the US's initial jobless claims for the week ending July 12, the US's continued jobless claims for the week ending July 5, the US's July Philadelphia Fed manufacturing index, the US's June retail sales monthly rate, the US's June core retail sales monthly rate, the US's June retail sales annual rate, and the US's June retail sales control group monthly rate (seasonally adjusted) associated with GDP will be released.

Additionally, attention should be paid to the US Fed's release of the Beige Book on economic conditions. FOMC permanent voting member and New York Fed President Williams delivered remarks on the US economy and monetary policy. South Africa hosted the G20 finance ministers and central bank governors meeting until July 18.

Crude oil:

Both oil futures rose slightly, with WTI up 0.64% and Brent up 0.58% as of 11:47. Oil prices gained in early trading, reversing the previous session's decline, as economic data from major oil-consuming countries exceeded expectations and signs emerged of easing trade tensions.

The US Energy Information Administration (EIA) reported on Wednesday that US crude inventories fell last week due to higher exports, while gasoline and distillate stockpiles rose, raising some concerns about fuel demand. The report showed US commercial crude inventories decreased by 3.9 million barrels to 422.16 million barrels in the week ending July 11, compared with analysts' expectations of a 552,000-barrel draw. Gasoline inventories rose by 3.4 million barrels to 232.87 million barrels, versus market forecasts of a 1 million-barrel decline. Distillate stocks, including heating oil and diesel, increased by 4.2 million barrels to 106.97 million barrels, compared with expectations of a 200,000-barrel build. (Comprehensive report by Wen Hua)

Spot market overview:

►Tianjin zinc: Futures fluctuated while downstream demand stayed weak [SMM midday review]

►SMM seven-region zinc ingot social inventory increased by 400 mt [SMM data]

►Silver prices consolidated with sluggish spot market transactions [SMM daily review]

Other metal spot midday reviews will be updated shortly. Please refresh to view~