SMM News on July 11:

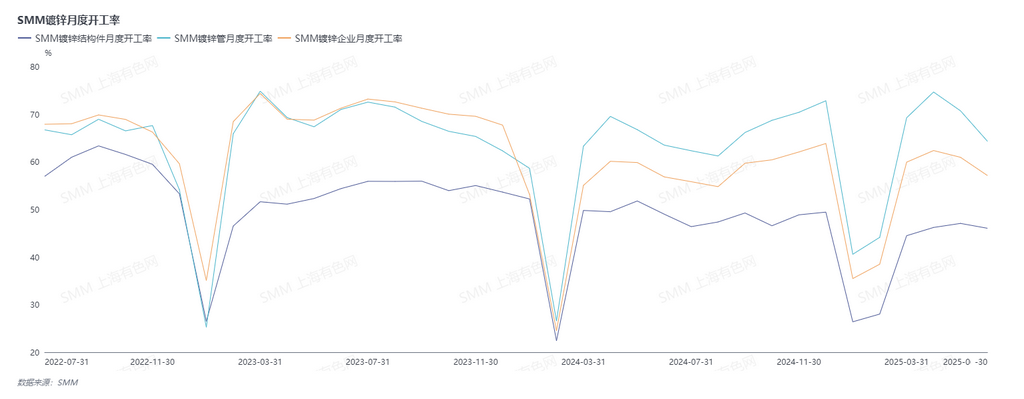

In the first half of the year, tariff disputes continued, jointly boosting domestic consumption from multiple perspectives such as capital and demand. However, due to timing issues, the implementation speed has been relatively slow. According to SMM's communication and understanding, the operating rates of galvanising producers in the first half of 2025 moved downwards after a higher opening. What are the reasons behind this?

From the perspective of the first quarter, galvanising enterprises began to enter the holiday maintenance rhythm one after another from early January. At the same time, due to the cold weather, most construction projects also gradually entered the holiday rhythm, and demand started to pull back. After the holiday, large factories resumed production first, while small factories gradually resumed production around the Lantern Festival. The progress of project construction and resumption of work was slow, and demand climbed slowly. Infrastructure investment in February increased slightly YoY. Most enterprises were fulfilling orders received before the Chinese New Year, and the operating rates of galvanising producers rose slowly. Compared with the same period, the operating rates were relatively weak. By early March, there was no obvious sign of the traditional "golden March" peak season as in previous years. However, subsequent demand improved, and the operating rates rose. Moreover, the "2024 China Fiscal Policy Implementation Report" released by the Ministry of Finance on March 24 explicitly mentioned actively expanding effective investment. It emphasized coordinating the use of various government investment funds, focusing on key areas and weak links to increase investment. It also stressed arranging the issuance of government bonds reasonably, accelerating the budget allocation of government bond funds, and forming physical workloads as soon as possible. This boosted the market, and overall, the operating rates in March increased YoY.

Entering the second quarter, the operating rates in April surged, and the operating rates of galvanized pipe producers also reached a three-year high. The main reasons were that ferrous metals prices in April were relatively stable, with a steady increase. The phenomenon of "rush to buy amid continuous price rise and hold back amid price downturn" among traders emerged. The overall sales volume of galvanized pipes was moderate, and many enterprises continued to operate in a low-inventory circulation mode, with weekly inventory days maintained at only around 7-8 days. The order circulation was good, leading to an increase in enterprise operating rates. In terms of structural parts, there were new orders gradually released for steel tower orders, and new tenders continued. Steel tower orders remained robust. Guardrail orders were also robust. Export orders were partially rushed to export due to tariff impacts. Overall, the operating rates in April were good. However, demand started to pull back in May and June, entering the traditional off-season. There were impacts such as heavy rainfall and floods, and the northern region entered high-temperature weather prematurely, limiting terminal construction. Demand pulled back significantly, and the operating rates gradually declined.

Looking ahead to the second half of the year, China's "supply-side reform 2.0" is heating up again. Anti-"rat race" competition policies are boosting the steel industry. At the same time, the National Development and Reform Commission's Urban and Small Town Reform and Development Center stated that it would use "implement major national strategies and build up security capacity in key areas" and "program of large-scale equipment upgrades and consumer goods trade-ins" funds as a starting point to increase investment in key areas of new urbanization. This will provide a certain boost to downstream consumption. However, the third quarter itself is a consumption off-season with more extreme weather conditions. Overall, the operating rates will be relatively weak. But with policy support, it is expected that consumption will gradually improve in September and October, leading to an increase in operating rates. By winter, the operating rates will gradually weaken on a MoM basis.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research decisions. Customers should make cautious decisions and should not replace their independent judgment with this information. Any decisions made by customers are not related to SMM.)