1. According to the SMM survey, the loss per ton of coke expanded this week, with a current loss of 23 yuan/mt.

In terms of prices, coke prices remained stable this week, having no impact on the profits of coking enterprises. On the cost side, with the resumption of production at some coal mines, the supply of coking coal gradually improved. Along with the continuous rally in the futures market, market sentiment was boosted, and the purchase willingness of downstream enterprises and traders increased. Coal mines had good sales, and the inventory pressure on coking coal eased. Online auctions also generally saw price increases, with coking coal prices rebounding by 10-30 yuan/mt. As costs increased, the losses of coking enterprises expanded.

Looking ahead, there is an expectation for a round of coke price increases, and there is also room for coking coal prices to rise, which may reduce the effectiveness of profit recovery for coking enterprises. It is expected that coking enterprises may turn from losses to profits next week, with some profits.

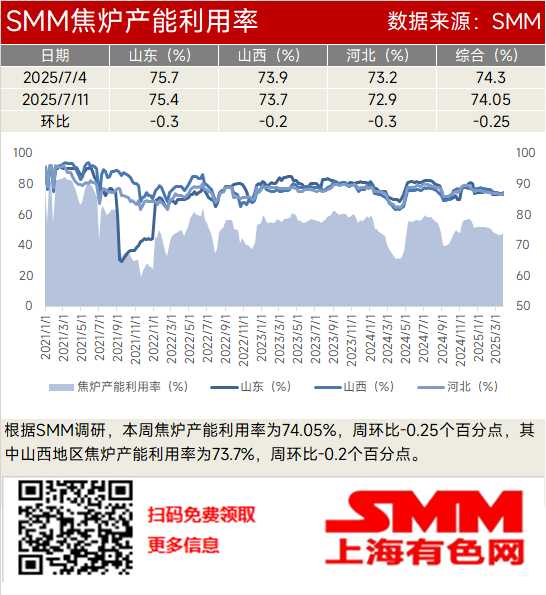

2. According to the SMM survey, the coke oven capacity utilization rate was 74.05% this week, down 0.25 percentage points WoW. Among them, the coke oven capacity utilization rate in Shanxi was 73.7%, down 0.2 percentage points WoW.

From the market perspective, the enthusiasm for downstream coke purchases increased this week, and coking enterprises had smooth sales. The coke inventory of some coking enterprises has already dropped to a low level. On the demand side, pig iron production of steel mill blast furnaces remained high, creating a rigid demand for coke. Some steel mills with low inventory had strong purchase willingness. In summary, the operation of coking enterprises was basically stable this week, with only a slight decline due to losses.

Looking ahead, the fundamentals of coke are good, and profits are expected to recover. It is expected that the coke oven capacity utilization rate will remain stable next week.

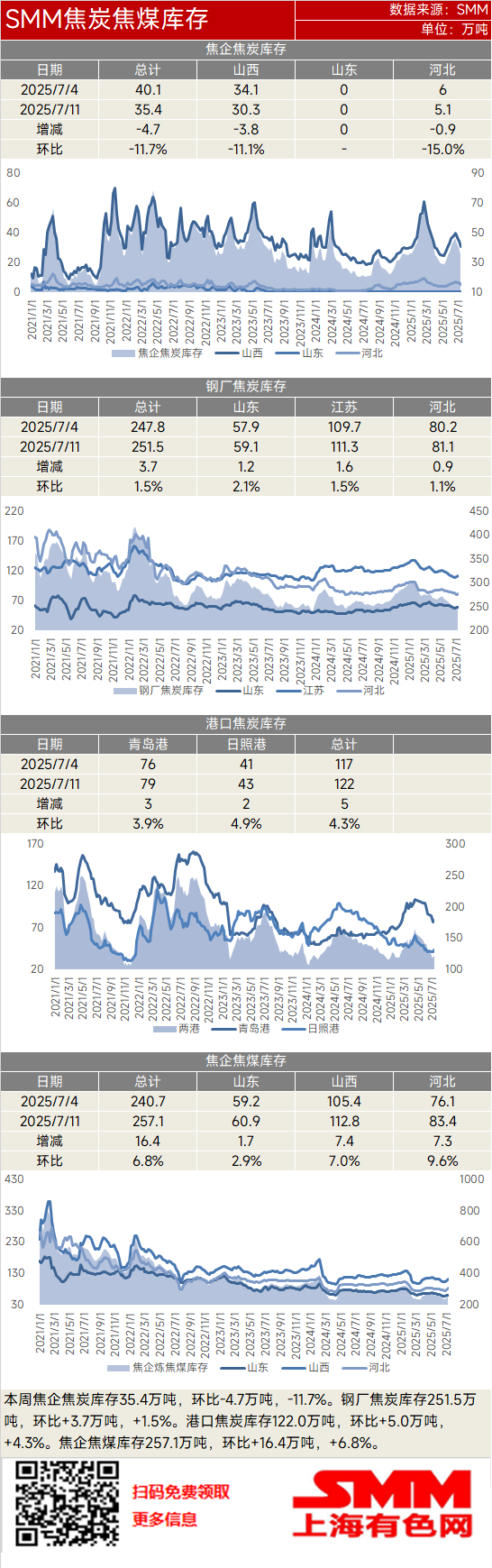

3. This week, the coke inventory of coking enterprises was 354,000 mt, down 47,000 mt MoM, a decrease of 11.7%. The coking coal inventory of coking enterprises was 2.571 million mt, up 164,000 mt MoM, an increase of 6.8%. The coke inventory of steel mills was 2.515 million mt, up 37,000 mt MoM, an increase of 1.5%. The coke inventory at the two ports was 1.22 million mt, up 50,000 mt MoM, an increase of 4.3%.

This week, coking enterprises operated normally and had smooth sales, with coke inventory continuing to decline. On the raw material side, coal mines had good sales, and online auctions also generally saw price increases. The downstream purchase demand was released, and the coking coal inventory of coking enterprises increased. On the steel mill side, pig iron production of steel mill blast furnaces remained high, creating a rigid demand for coke. Some steel mills with low inventory had high purchase enthusiasm, and the coke inventory of steel mills increased slightly.

Looking ahead, the operation of steel mills will remain at a high level, and the rigid demand for coke will continue. The purchase enthusiasm is moderate, and it is expected that the coke inventory of coking enterprises may continue to decline next week. On the raw material side, with stable production at coking enterprises and positive market sentiment, it is expected that the coking coal inventory of coking enterprises will remain stable or increase slightly next week. For steel mills, with good profits and high operating rates, the demand for coke procurement continues to be released, and it is expected that the coke inventory of steel mills will increase steadily next week. In terms of port inventory, coke producers have smooth shipments, and the market trading atmosphere is good. With a tight supply-demand pattern, it is expected that the port coke inventory will remain stable or increase slightly next week.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)