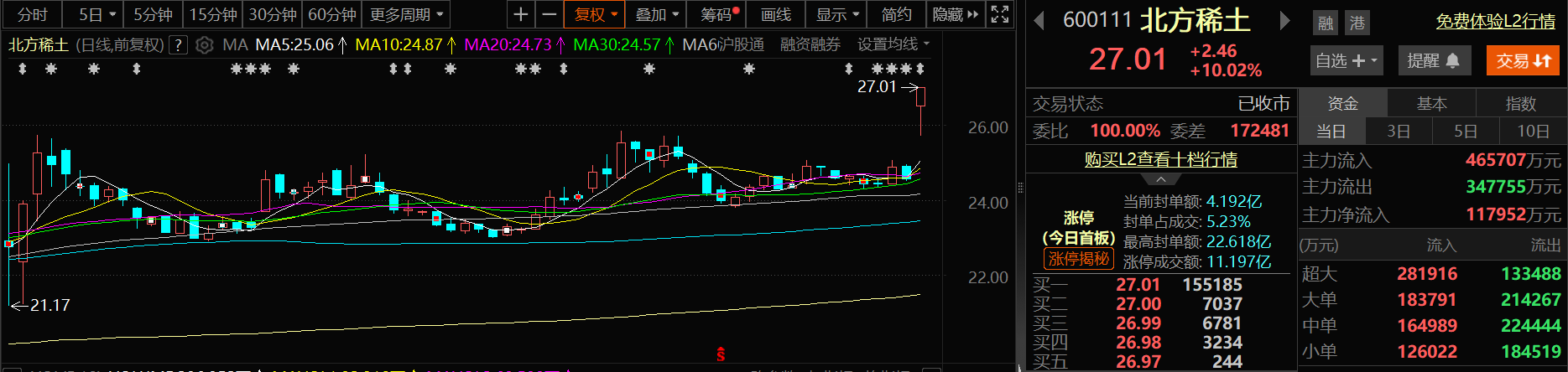

Affected by the significant year-on-year increase in China Northern Rare Earth's H1 performance, its share price surged by the daily limit on July 10, closing at a 10.02% increase, with the share price at 27.01 yuan per share.

On the news front: China Northern Rare Earth announced on the evening of July 9 that, based on preliminary calculations by the company's finance department, it is expected to achieve a net profit attributable to owners of the parent company of 900 million to 960 million yuan for the first half of 2025, representing an increase of 855 million to 915 million yuan compared to the same period last year (legally disclosed data), up 1882.54% to 2014.71% YoY. It is expected to achieve a net profit attributable to owners of the parent company, excluding non-recurring gains and losses, of 880 million to 940 million yuan for the first half of 2025, representing an increase of 865 million to 925 million yuan compared to the same period last year (legally disclosed data), up 5538.33% to 5922.76% YoY.

Regarding the main reasons for the significant year-on-year increase in performance for this period, China Northern Rare Earth stated:

In the first half of 2025, facing a complex development environment, the company seized the favorable conditions of market stabilization and improvement, actively responded to the impact of uncertain and unstable factors such as the Sino-US trade conflict, adhered to strategic planning, anchored the annual production and operation task targets, overcame difficulties, forged ahead, comprehensively implemented the new development concept, accelerated the construction of a new development pattern, and effectively assumed the responsibility of being the main force in the construction of the "two rare earth bases". It strengthened comprehensive budget management, deepened cost reduction, quality improvement, and efficiency enhancement, scientifically coordinated production scheduling, strengthened market research and forecasting, intensified marketing operations, accelerated the construction of key projects, promoted scientific research and management innovation, strengthened performance appraisal incentives and constraints, fully utilized the stable domestic market demand pattern and advantages, implemented coordinated strategies and efforts in all aspects of production and operation management, strengthened strengths, addressed weaknesses, improved quality, and promoted development, laying a solid foundation and providing strong support for the significant year-on-year increase in the company's H1 operating performance, and continuously leading the industry's sustainable and high-quality development with new achievements in high-quality development.

In terms of production and marketing, the company strengthened production system management, promoted production line linkage and process upgrades among its affiliated smelting and separation enterprises, further improved production line operating efficiency, continuously optimized raw material and product structures, and met the market demand for high-value-added products with special, customized, and characteristic features.It deepened horizontal and vertical benchmarking improvements, further reducing the costs of smelting and separation and rare earth metal processing. It fully ensured the supply of raw material products, guided by market demand, deepened marketing model innovation, strengthened marketing operations, and achieved varying degrees of year-on-year growth in the production and sales volumes of its main products, including smelting and separation, rare earth metals, rare earth functional materials, and permanent magnet motors. In terms of key project construction, we have comprehensively consolidated our scale advantages and accelerated the progress of key projects. The first phase of the new-generation rare earth green mining, beneficiation, and smelting upgrade and transformation project has entered the final stage of production line linkage debugging, while the second phase's process design and other work are progressing in an orderly manner. Capital operation projects aimed at extending, supplementing, and strengthening the industry chain, such as mergers, acquisitions, restructuring, joint ventures, and cooperation, are advancing efficiently and steadily. In terms of R&D and innovation, we have continued to strengthen our scientific research strengths, achieving fruitful results in technological innovation. We have formulated a reform plan for scientific and technological innovation, identifying six reform directions and proposing 23 reform tasks centered around optimizing the scientific research management system. We have strengthened the construction of industrial transformation centers, continuously improving the conversion rate of scientific research achievements. We have fully leveraged the advantages of our scientific research platforms, achieving new breakthroughs in new product R&D. In terms of deepening reform and governance improvement, we have advanced the reform of state-owned enterprises, consolidated and improved the modern governance system, strengthened performance appraisals across various dimensions and levels, optimized the "stretch goal mechanism," and introduced "basic targets," "aspirational targets," and "excellence targets," fully mobilizing the enthusiasm of all employees and consolidating a strong atmosphere of entrepreneurship. ESG, compliance, and market value management have been advanced synergistically, with multiple achievements. ESG ratings have been upgraded by mainstream institutions such as the China Securities Index Co., Ltd. The construction and operation of the compliance system have been increasingly refined, with compliance continuously driving high-quality development. Multiple measures have been taken in market value management, with synergistic efforts resulting in a 17.34% increase in market value in H1, maintaining the company's position as the publicly listed firm with the largest market value in the rare earth permanent magnets industry. Relying on its industry status, influence, and market value scale, the company's stock was selected for the first time as a constituent stock of the CSI A50 Index, further enhancing the company's visibility in the capital market and its investment appeal.

Previously, when asked about the company's expectations for future rare earth prices,China Northern Rare Earth responded in the investor relations activity record table announced on June 24:Since the first quarter of 2025, influenced by policies such as the tightening of upstream raw material supply and the stimulation of downstream consumption, the overall activity of the rare earth market has been better than that of the same period last year, which has also supported the company's performance in the first quarter. The company has seized the favorable market opportunities, comprehensively improved production line operational efficiency, continuously optimized raw material and product structures, expanded markets in multiple ways, and advanced reforms in depth, achieving record-high production and sales volumes. After entering April-May, rare earth prices experienced a brief pullback due to the international environment. However, as national policies have gradually become clearer, the attention paid to the rare earth industry has also risen, driving up product prices. Currently, the orders of the company's subsidiary, Inner Mongolia Northern Rare Earth Magnetic Materials Co., Ltd., are relatively full, and the company holds an optimistic view on the future trend of rare earth prices.

Additionally, according to Cailian Press, Wu Yonggang, the board secretary of China Northern Rare Earth, stated at the 2025 Q1 earnings presentation held earlier that the company's light rare earth export licenses are being processed normally, with normal exports; the export licenses for medium-heavy rare earth dual-use items have been submitted to the Department of Commerce of the Inner Mongolia Autonomous Region for approval. The company's main export products include Pr-Nd, lanthanum-cerium, gadolinium oxide, terbium oxide, yttrium oxide, etc., mainly exported to Japan, the US, Germany, and other places. It is expected that this year's export volume will be comparable to last year's export level. The proportion of the company's export revenue in its total revenue is very small. Furthermore, the company's green smelting upgrading and transformation project, as the world's largest and most complete rare earth smelting and separation project, has entered the stage of full completion and operation for its first phase, and the second phase is planned to commence construction in the second half of 2025.

》Click to view SMM rare earth spot prices

》Subscribe to view historical SMM metal spot price trends

Reviewing the price trend of SMM Pr-Nd oxide in the first half of this year, it can be seen that the average price of Pr-Nd oxide on June 30 was 444,500 yuan/mt, compared to the average price of 398,000 yuan/mt on December 31, 2024, showing an increase of 11.68% in the first half of this year. Comparing the daily average price of Pr-Nd oxide in the first half of 2025 (430,952.99 yuan/mt) with that in the first half of 2024 (381,350.43 yuan/mt), it can be seen that the daily average price in the first half of this year increased by 13.01% YoY. The rare earth market was driven by multiple positive news at the end of last year, akin to being injected with a strong stimulant, causing rare earth prices to rise rapidly. Especially before the Chinese New Year, the price of Pr-Nd oxide once surged to 415,000 yuan/mt, showing an increase of approximately 4.3% compared to the New Year's Day period. The festive atmosphere of the Chinese New Year seemed to have infected the rare earth market, with the bullish sentiment remaining high after the holiday. The procurement demand from downstream also showed great activity, and this robust demand further boosted the surge in rare earth prices. However, since the end of February, with the resumption of work by magnetic material enterprises, the number of new orders did not meet expectations, causing rare earth prices to experience a slight pullback, as if injecting a touch of calm into the overheated market. The rare earth market in March appeared somewhat mediocre. Without the intervention of new influencing factors, rare earth prices only fluctuated within a relatively small range, showing a fluctuating rangebound trend. By April, rare earth prices dropped rapidly, and the market seemed to enter a brief cooling-off period. However, by the end of April, with the procurement and restocking behavior of major customers and the delivery of long-term agreement orders, rare earth prices were boosted again, showing an upward trend. In May, with the superposition of various factors, rare earth prices generally continued their upward trend, and the market also showed a certain level of activity. However, in June, rare earth prices began to stabilize, with no significant fluctuations occurring. This was due to a weak supply-demand balance in the market, where a stalemate between upstream and downstream players made it difficult for prices to experience major changes.

According to SMM quotations, the average price of Pr-Nd oxide on July 10 was 453,500 yuan/mt, down 500 yuan/mt (0.11%) from the previous trading day. Since early July, Pr-Nd oxide prices showed consecutive increases from July 3 to July 8, primarily driven by the following factors: Supply side, market concerns about oxide production cuts intensified due to temporary shutdown expectations at some rare earth enterprises amid news-driven sentiment, while the rainy season in Southeast Asia is expected to reduce imports of ion-adsorption ore. Demand side, frequent tenders by major magnetic material manufacturers significantly boosted market confidence, with most industry participants holding optimistic expectations for warming downstream demand.

Regarding the rare earth market outlook, consensus has formed based on supply-demand dynamics: the expectation of tightening Pr-Nd oxide fundamentals in the short term has been established. This shift provides solid support for Pr-Nd oxide prices. Meanwhile, as the traditional off-season for NdFeB approaches its end, the impending September-October peak season will further strengthen market expectations. The industry widely believes Pr-Nd prices will maintain their upward trajectory in the coming period.

Guosen Securities previously noted in its research report on China Northern Rare Earth: the company adjusted its product mix, achieving high YoY growth in magnetic material production. The Bayan Obo mine owned by Baogang Group is China's largest rare earth deposit with unique characteristics—a super-large polymetallic complex ore containing rare earths, iron, niobium, and thorium, accounting for over 80% of national reserves with stable resource supply. In 2024, the company obtained a total mining quota of 188,700 mt (+5.6% YoY), maintaining a 69.9% share of national quotas, virtually unchanged from 2023. Production-wise, the company's total smelting and separation output (rare earth oxides + salts + metals) reached 177,700 mt (+1.63% YoY) in 2024, while magnetic material production hit 58,800 mt (+17.72% YoY) through equipment upgrades. In 2025Q1, smelting and separation output totaled 55,200 mt (+12.80% YoY), with magnetic material production at 16,400 mt (+40.88% YoY). Since 2024Q3, the company has strengthened its cost advantages. Structurally, China Northern Rare Earth doesn't engage in mining, sourcing raw materials by purchasing rare earth concentrate from Bao Gang United Steel. Since 2022Q4, the company has signed quarterly Rare Earth Concentrate Supply Contracts with Bao Gang United Steel, setting prices and transaction volumes through negotiated calculations based on market price fluctuations. In Q1 2024, the transaction price of rare earth concentrate was RMB 20,700 yuan/mt (excluding tax), while market prices pulled back significantly during this period. Due to the existence of a price adjustment cycle, the company faced significant cost pressure on raw materials. In Q3 2024, the company's purchase price was 17.21% lower than the average market price. In Q2 2025, the company's purchase price was adjusted to RMB 18,800 yuan/mt (excluding tax), which was 14.45% lower than the current average market price of RMB 22,000 yuan/mt, maintaining cost advantages. Risk warnings: The growth in demand for magnetic materials falls short of expectations; volatile rare earth prices; significant increase in concentrate prices; the growth rate of the company's mining quotas falls short of expectations.

![Rare Earth Prices Edge Down, Market Inquiry Activities Decline [SMM Rare Earth Daily Review]](https://imgqn.smm.cn/usercenter/vpWKL20251217171743.jpeg)