On July 4, Hongda shares continued to decline by 1.91% from the previous trading day, closing at 8.75 yuan per share.

When asked about "when the detailed survey work of the Duobuzaxi copper mine is expected to be completed, and if completed, whether the mining and development work will be initiated in a timely manner," Hongda shares stated on the investor interaction platform on July 2 that currently, the detailed geological survey work of the Duobuzaxi copper mine is underway, and subsequent related work will be gradually and orderly advanced.

Hongda shares announced on June 17 that the company's application for issuing shares to specific objects had received approval for registration from the China Securities Regulatory Commission. The closing price of Hongda shares on June 16 was 7.66 yuan per share, with a total market value of 15.565 billion yuan. According to the prospectus (registration draft), the company plans to issue 609.6 million shares to its controlling shareholder, Shudao Investment Group Co., Ltd., at an issue price of 4.68 yuan per share, raising a total of 2.853 billion yuan in funds. After deducting related issuance expenses, the funds will be used to repay debts and supplement working capital. Part of the funds raised from this issuance are intended to repay debts, including the principal and delayed performance fees for the profit refund from Jinding Zinc Industry, the company's former controlling subsidiary, as well as short-term borrowings. Given that the company finds it difficult to resolve its debt issues through its own profits in the short term, Shudao Group plans to inject capital and provide relief to the company by subscribing to the shares issued by the company, which is beneficial for resolving the company's debt issues, improving its risk resistance capability, and promoting its sustained and healthy development. Part of the funds raised are intended to supplement working capital, which will be beneficial for increasing the stockpiling of raw materials and inventory products, improving capacity utilization rates, and enhancing profitability. Meanwhile, by subscribing to the issued shares, Shudao Group's shareholding ratio will increase, which will help further enhance the stability of the company's control rights, demonstrate its firm confidence in the company's future development prospects, and be beneficial for sending positive signals to the market and minority shareholders.

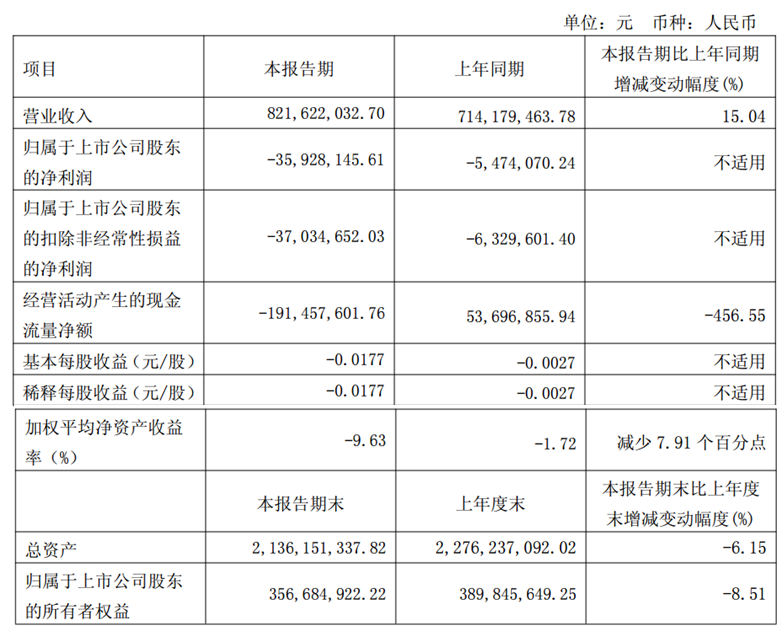

Hongda shares previously disclosed its 2025 Q1 report, showing that in the first quarter of this year, the company achieved a total operating revenue of 822 million yuan, up 15.04% YoY; the net profit attributable to shareholders of the parent company suffered a loss of 35.9281 million yuan, compared to a loss of 5.4741 million yuan in the same period last year. Regarding the main reasons for the increase in operating revenue, Hongda shares introduced that it was due to the increase in sales volume and selling prices of zinc products compared to the same period last year, as well as the increase in sales volume of compound fertilizer products during the reporting period.

The operating situation in the first quarter of this year is as follows:

1. Main business situation: In terms of phosphorus chemical products, the price of sulfur, a key raw material for phosphorus chemical products, rose sharply in the first quarter of 2025, with the sulfur procurement price increasing by 84.91% compared to the same period last year, leading to a certain degree of decline in the profitability of the company's phosphorus chemical products. In terms of non-ferrous metals, the processing fees for zinc products remained low in the first quarter of 2025, resulting in losses for the company's zinc smelting business. In terms of natural gas chemical products, the selling price of synthetic ammonia decreased compared to the same period last year in the first quarter of 2025, leading to losses for the synthetic ammonia business of the company's controlling subsidiary, Sichuan Mianzhu Chuanrun Chemical Co., Ltd. (hereinafter referred to as "Mianzhu Chuanrun").

2. Cash Flow: The net cash flow generated from the company's operating activities during this period was -RMB 1.91 billion, representing a decrease of 456.55% compared to the same period last year. This was primarily due to the company's payment of employee salaries accrued at the end of the previous year in Q1 2025, resulting in a reduction in accounts payable and an increase in cash payments for raw material inventory.

3. Changes in Period Expenses: Financial expenses during this period decreased by 29.4% compared to the same period last year, mainly due to the company's full repayment of the principal amount for profit refunds to Jinding Zinc Industry, a corresponding decrease in late payment penalties, and a reduction in interest expenses resulting from a decrease in bank loan interest rates for the company's existing loans. Administrative expenses decreased by 16.27% compared to the same period last year, primarily due to a decrease in expenditures on salaries, welfare benefits, depreciation expenses, and service fees for intermediaries compared to the same period last year.

4. Cost and Seasonal Factors: Q1 is the dry season, and higher electricity prices have led to an increase in production costs for the company's chemical and non-ferrous metal businesses compared to the rainy season. With the arrival of the rainy season in Q2 and Q3, electricity prices are expected to decrease, and the company's production costs will correspondingly decrease.

5. Production Plans and Outlook: According to the annual production and operation plan, Mianzhu Chuanrun and the Non-Ferrous Metal Branch have successfully completed their annual maintenance work in Q1 2025, laying a solid foundation for subsequent full-capacity production. The company will closely monitor market dynamics and its own business characteristics to further optimize production organization. It will actively reshape the supply chain system, strengthen collaborative relationships with upstream and downstream enterprises, and continuously expand raw material procurement channels and product sales channels. The company will also reasonably plan its capital arrangements, optimize its financing structure, and effectively reduce financing costs, thereby further reducing financial expenses.

Hongda shares stated on the investor interaction platform on April 29 that, with the strong support of the group, the company is actively promoting the development work of the Duolong Copper Mine. As of now, the Duolong Copper Mine has entered the exploration-to-mining transition stage, and the company has completed the review and filing of the "Duolong Copper Mine Exploration Report". The "Duolong Copper Mine Development and Utilization Plan" and the "Mine Geological Environment and Land Reclamation Plan" reports have also completed the review process.

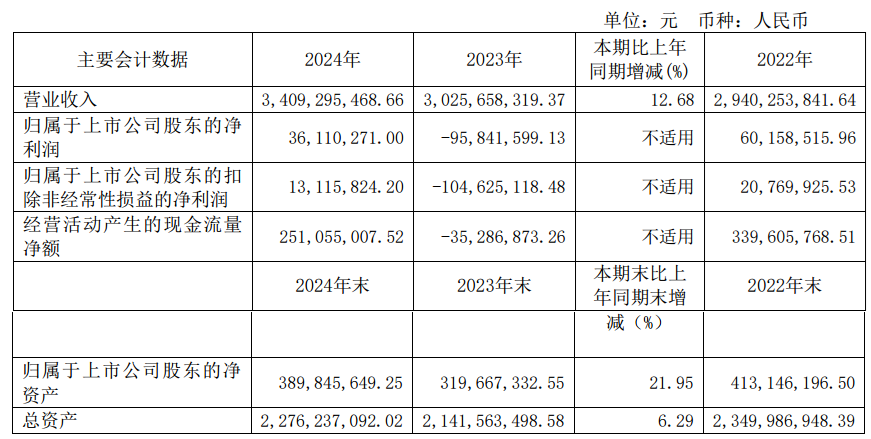

Hongda shares' 2024 annual report previously released showed that in 2024, the company achieved a total operating revenue of RMB 3.409 billion, representing a year-on-year increase of 12.68%; and a net profit attributable to shareholders of RMB 36.1103 million, turning from a loss in the same period last year.

Hongda shares' 2024 annual report indicates that the main performance drivers during the reporting period were as follows: 1. Main Business (1) In the phosphorus chemical industry, influenced by the positive international market situation, domestic market pull, and export policy support, the phosphorus compound fertilizer industry showed a market trend of initial decline followed by recovery. In 2024, the company thoroughly analyzed the trends in the procurement and sales markets, striving to align with market rhythms. During the spring farming and autumn sowing seasons, the company received a substantial and growing number of orders for its phosphate series products and compound fertilizer products, resulting in a thriving state of both production and sales. Influenced by the significant increase in sales of phosphate series products and compound fertilizers, as well as the decrease in the cost of some bulk raw materials such as liquid ammonia, the company's phosphate chemical business achieved a certain degree of growth in operating performance. (2) In the non-ferrous metal zinc smelting sector, the company made significant breakthroughs in the technology for extracting associated rare and precious metals, improving the recovery rates of associated rare and precious metals such as gold, silver, and copper in raw materials. Meanwhile, amid the continuous decline in zinc concentrate processing fees, the company increased its procurement of zinc concentrate rich in gold, silver, and copper. As a result, the production and sales of by-products containing rare and precious metals such as gold, silver, and copper surged, effectively reducing the overall production cost of zinc smelting. Influenced by international and domestic macro factors such as heightened expectations for US Fed interest rate cuts and escalating geopolitical conflicts, the prices of precious metals such as gold, silver, and copper rose sharply, significantly increasing the value of by-products. In 2024, the gross profit margin of the company's zinc products and by-products increased, and the company's zinc smelting business turned from losses to profits. (3) In the natural gas chemical sector, influenced by factors such as the low price of synthetic ammonia abroad, the increase in domestic synthetic ammonia capacity, and the decline in coal prices, the market price of synthetic ammonia continued to fall. In 2024, the average annual price of synthetic ammonia decreased by 18.73% compared to 2023. In 2024, the profitability of the synthetic ammonia products of the company's holding subsidiary, Mianzhu Chuanrun, declined to a certain extent compared to the same period last year. 2. Due to the contract dispute case with Jinding Zinc Industry, in 2024, the company accrued a delay performance fee of RMB 27.1324 million for the principal amount of unreturned profits, which was included in the 2024 profit and loss. 3. In accordance with the equity adjustment plan for contributors under the restructuring plan of Sichuan Trust, the company unconditionally transferred its 22.1605% equity stake in Sichuan Trust. On September 27, 2024, the Chengdu Intermediate People's Court approved the restructuring plan of Sichuan Trust Co., Ltd. The company no longer holds any equity in Sichuan Trust and disposed of its long-term equity investment in Sichuan Trust. The corresponding other comprehensive income of RMB -35.9446 million was included in the current profit and loss. The impact of this matter on the company's 2024 profit and loss was RMB -35.9446 million. 4. On December 3, 2024, the company received a total of RMB 11.8904 million in creditor's rights distribution payments from the bankruptcy liquidation case of its former wholly-owned subsidiary, Jianchuan Yiyun. In accordance with relevant provisions of enterprise accounting standards, the company reversed RMB 11.8904 million in credit loss provisions for other receivables in 2024, correspondingly increasing the total profit for 2024 by RMB 11.8904 million. 5. On December 10, 2024, the company received a debt settlement payment (cash portion) of RMB 39.1101 million from the administrator of Hongda Group. In accordance with relevant provisions of the Accounting Standards for Business Enterprises, the company recorded the received debt settlement payment (cash portion) of RMB 39.1101 million in revenue-related accounts, reporting it as non-operating income, and accordingly increased the total profit for 2024 by RMB 39.1101 million. 6. In 2024, the total government subsidies included in current profit and loss amounted to RMB 6.2856 million. The company's performance changes in 2024 were in line with industry development trends and its own actual situation.

Regarding its business plan, Hongda Co., Ltd. stated in its 2024 annual report: For 2025, the company plans to achieve operating revenue of RMB 3.554 billion and control total costs and expenses at RMB 3.489 billion. It plans to produce 80,000 mt of zinc products, 340,000 mt of phosphate series products, 210,000 mt of compound fertilizers, and 125,000 mt of synthetic ammonia. The company may adjust its business plan in a timely manner based on market changes. The aforementioned development strategies and business plans do not constitute performance commitments to the company's investors. Investors are advised to maintain sufficient risk awareness and understand the differences between development strategies, business plans, and actual operations.

A research report titled "Increased Group Support, World-Class Copper Mine May Soon Launch" published recently by China Post Securities, commenting on Hongda Co., Ltd., pointed out: The raised funds aim to address the company's liquidity issues and optimize its capital structure. Shudao Group's takeover and full subscription of the private placement demonstrate confidence. The Duolong copper mine has enormous reserves, with an annual production capacity of approximately 313,200 mt of copper. The company currently holds a 30% stake in Duolong Mining, while Shudao Group holds a 40% stake through Hongda Group. The Duolong copper mine is located in the Ngari region of Tibet and is China's first world-class super copper mine concentration area, with copper metal reserves reaching 6.91 million mt, accompanied by approximately 303 mt of gold resources and 1,758 mt of silver resources. In terms of production, the Duolong copper mine has a designed mining scale of 75 million mt/year and a total service life of 24 years (including a 2-year infrastructure construction period). Based on an 87% recovery rate for copper sulfide ore beneficiation, it is expected to produce approximately 313,200 mt of copper annually, along with 8 mt of gold and 12 mt of silver, potentially ranking among the top ten copper mines globally. The project has passed expert review and may commence development in the second half of the year. In March 2025, the Land and Mineral Rights Trading and Resource Reserve Review Center of the Tibet Autonomous Region organized experts to review and approve the "Mineral Resource Development and Utilization Plan for the Duolong Copper Mine in Gaize County, Tibet Autonomous Region." The project is currently in a critical early stage of transitioning from exploration rights to mining rights. According to the regulations of the Tibet Autonomous Region, which require the processing of exploration and mining rights applications within 40 days, the development progress of the Duolong copper mine is expected to accelerate significantly, with formal development expected to commence in the second half of the year. Risk Disclosure: Price fluctuation risk; risk of project progress falling short of expectations; risk of downstream demand falling short of expectations; model assumptions inconsistent with reality; risk of policies exceeding expectations, etc.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)