Consulte cotações, dados e análises de mercado de produtos de cobalto e lítio da SMM

Assine para acessar tendências históricas de preços à vista de produtos de cobalto e lítio da SMM

Principais fabricantes de células de bateria lançam concursos – os preços do LFP continuarão a cair no segundo semestre?

Os preços do LFP consistem principalmente em dois componentes: taxas de processamento agrupadas (também conhecidas como valorização no setor) + preço do carbonato de lítio × desconto de liquidação, com as taxas de processamento agrupadas já incorporando os custos da matéria-prima fosfato de ferro e despesas de processamento.

Nas negociações de preços, as partes a montante e a jusante concentram-se principalmente nestes dois aspetos, embora também sejam considerados termos comerciais como os períodos de pagamento. Geralmente, uma vez acordadas, as taxas de processamento agrupadas permanecem inalteradas por ciclos de execução mensais ou trimestrais, a menos que ocorram flutuações inesperadas nos preços da matéria-prima fosfato de ferro. Portanto,os preços do LFP flutuam principalmente em linha com os preços do carbonato de lítio.

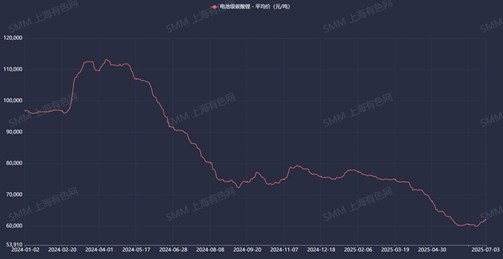

Desde o início de abril deste ano, os preços do carbonato de lítio registaram declínios sustentados e significativos, caindo gradualmente abaixo do "limiar de compra de fundo" percebido pelo mercado.

[Fonte: Preço médio de carbonato de lítio de qualidade para baterias da SMM]

Estreitamente correlacionados com os preços do carbonato de lítio, os preços do LFP inevitavelmente seguiram uma trajetória de queda acentuada durante estes três meses.

Até ao momentoZ11/>acumularam uma queda média de mais de 3.000 yuan/tonelada, com maio a registar a maior queda mensal (-5,3%), enquanto abril (-2,3%) e junho (-2,7%) apresentaram declínios relativamente menores.

[Fonte: Preço médio de LFP da SMM]

Como evoluirão os preços do LFP no segundo semestre? A análise dos preços das matérias-primas, das tendências das taxas de processamento e da procura a jusante sugere uma trajetória geralmente estável, mas de enfraquecimento. O preço mínimo depende das variações dos preços do carbonato de lítio e das tendências das taxas de processamento.

"Os aumentos dos preços do fosfato de ferro impulsionaram com sucesso os aumentos das taxas de processamento no primeiro trimestre de 2025"

A maioria das empresas finalizou suas taxas de processamento para 2025 antes de março,com aumentos gerais variando de 500 a 3.000 yuan/tonelada.O principal impulsionador foi o aumento acentuado dos preços do fosfato de ferro desde dezembro de 2024. A manutenção das taxas de processamento agrupadas originaisteria exacerbado as perdas para os fabricantes de materiais LFP, ameaçando as operações normais.Entretanto, fabricantes de células de bateria a jusante aumentaram as taxas de processamento para gerenciar a volatilidade do mercado e estabilizar as cadeias de suprimentos. Após o ajuste,as taxas de processamento do segundo trimestre permaneceram geralmente estáveis.

No entantoZ22/>a busca por novos aumentos de preços por parte dos fabricantes de materiais persiste– apesar dos ajustes anteriores, continuam negociando aumentos adicionais com fabricantes de células de bateria. Porém, a dinâmica do mercado mudou no final de abril, com o crescimento da demanda por fosfato de ferro desacelerando.Para garantir pedidos, fábricas de fosfato de ferro inundaram o mercado com preços baixos, impulsionando a queda do preço médio do fosfato de ferro. Produtores de materiais, que anteriormente mantiveram forte relutância em ceder nos preços, perderam uma premissa crucial de barganha – o aumento dos preços do fosfato de ferro.Apesar das tentativas ativas de negociar aumentos de preços com fabricantes de células de bateria de abril a junho, os produtores de materiais não alcançaram seus objetivos.

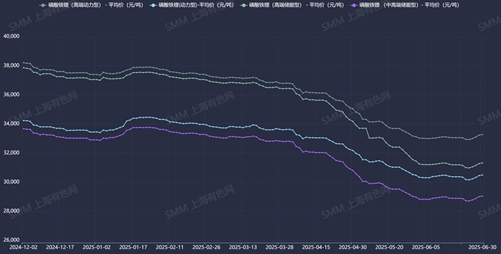

[Fonte: Preço Médio de Fosfato de Ferro SMM]

As esperanças de novos aumentos nas taxas de processamento LFP podem se mostrar infundadas.

Em junho, um grande fabricante de células de bateria lançou licitações para materiais LFP para o segundo semestre. Conforme antecipado, produtores de materiais que cotaram preços mais altos perderam a maioria dos leilões,enquanto os vencedores geralmente ofereceram preços mais baixos.Excluindo fornecedores de acordos de longo prazo isentos de licitação,aproximadamente quatro fornecedores garantiram licitações iniciais, com os perdedores entrando em negociações subsequentes com o fabricante de células de bateria individualmente.

Com base nas informações atuais, essa licitação sinaliza três desenvolvimentos:

- As taxas de processamento do segundo semestre podem tender a ser menores do que os níveis do primeiro semestre.Embora não tenham surgido resultados definitivos, fabricantes de células de bateria podem aproveitar a queda dos preços do fosfato de ferro para reduzir custos. O SMM prevê que as taxas de processamento terão dificuldade em subir no segundo semestre.

- Certos produtores de materiais de terceiro e quarto escalões entraram nas cadeias de suprimentos de grandes fabricantes com preços baixos. A definição de preços agressivos tornou-se fundamental para que os pequenos produtores de materiais garantam pedidos dos principais players, permitindo que os fabricantes de células de bateria alcancem reduções de custos. Consequentemente, o mercado de produtos de segunda geração (Gen 2) intensificou-se, com a oferta superando em muito a demanda. As perdas dominam esta linha de produtos devido a vendas abaixo do custo.

- Os preços da terceira geração (Gen 3) estão se aproximando dos níveis originais da segunda geração (Gen 2). À medida que a capacidade de materiais da terceira geração (Gen 3) também entra em excesso, as reduções de preços para garantir pedidos tornaram-se generalizadas para os produtos da terceira geração (Gen 3). Os preços estão até mesmo se aproximando dos níveis da segunda geração (Gen 2), tornando a terceira geração (Gen 3) não rentável para alguns produtores. Esta tendência sugere que os preços da terceira geração (Gen 3) não excederão significativamente os da segunda geração (Gen 2) no futuro, embora o poder de barganha específico dependa da escala dos fabricantes de células de bateria a jusante. No entanto, os produtos da terceira geração e meia (Gen 3.5) e da quarta geração (Gen 4) ainda mantêm resiliência nos preços. Dados detalhados de preços de LFP da SMM estão disponíveis para referência. Isso se relaciona principalmente com a dinâmica de oferta e demanda dos produtos: a pesquisa mais recente da SMM indica aproximadamente 6-7 fornecedores para os produtos da terceira geração e meia (Gen 3.5) e apenas 2-3 para os produtos da quarta geração (Gen 4). Em contraste, mais de 30 fornecedores competem no segmento da segunda geração (Gen 2) e mais de 25 na terceira geração (Gen 3), refletindo uma concorrência feroz.

A perspectiva de uma recuperação significativa nos preços do carbonato de lítio no segundo semestre ainda não está clara.

Outro fator-chave que influencia os preços do LFP é o preço do carbonato de lítio. A SMM acredita que a taxa de crescimento da demanda total de uso final irá gradualmente desacelerar no segundo semestre de 2025. Atualmente, não há aumento inesperado na demanda e, quando transmitido para a produção mensal de LFP, a taxa de crescimento parece medíocre. A taxa de crescimento mensal recente da produção de LFP também permaneceu basicamente dentro de 5%, aproximando-se da taxa de crescimento do material de cátodo ternário. Portanto, a possibilidade de uma melhoria no padrão de oferta e demanda do carbonato de lítio no segundo semestre ainda não está clara, e é difícil para seu preço reverter a tendência contra o mercado.

Levando em consideração todos os pontos acima, a guerra de preços pelas taxas de processamento está se intensificando. Juntamente com a dificuldade de reverter a tendência dos preços do carbonato de lítio, há uma alta probabilidade de que os preços do LFP continuem a operar em um nível baixo no segundo semestre. Nesta situação, as fábricas de materiais que não têm os fundos para sustentar as operações normais enfrentarão o risco de sair do mercado, serem adquiridas ou se tornarem processadoras de taxa.

Equipe de Pesquisa de Nova Energia da SMM

Wang Cong 021-51666838

Ma Rui 021-51595780

Feng Disheng 021-51666714

Zhou Zhicheng 021-51666711

Wang Zihan 021-51666914

Lv Yanlin 021-20707875

Zhang Haohan 021-51666752

Wang Jie 021-51595902

Xu Yang 021-51666760

Chen Bolin 021-51666836

![Revisão Semanal do Mercado de Carbonato de Lítio: 6.8-6.11 O Carbonato de Lítio à Vista Apresenta Tendência de Parar a Queda e Recuperar-se, com Flutuação Ascendente [Revisão Semanal SMM]](https://imgqn.smm.cn/usercenter/wZUBk20251217171729.jpg)

![[Revisão Semanal SMM] Mercado de Reciclagem Hidrometalúrgica desta Semana: Preços do Lítio Recuaram, Preços da Massa Negra de LFP Acompanharam e Subiram (8 a 11 de junho de 2026)](https://imgqn.smm.cn/usercenter/yZfeI20251217171727.jpg)

![[Lithium Battery: Times BAIC Battery Factory's First Cell Rolls Off Production Line]](https://imgqn.smm.cn/usercenter/KySZv20251217171726.jpg)