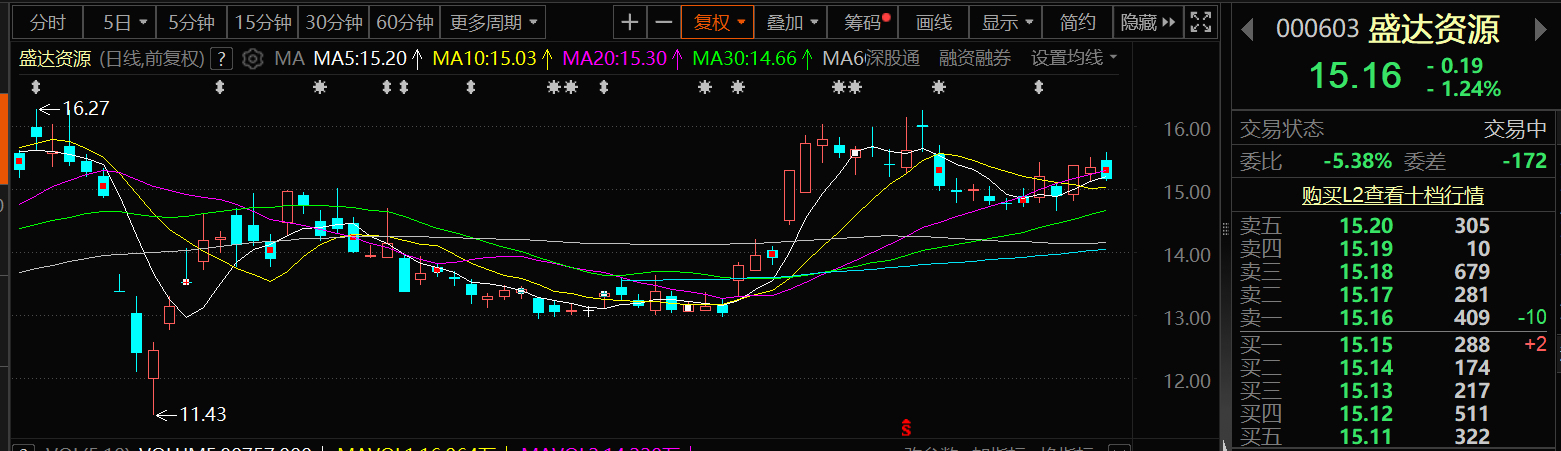

On July 3, Shengda Resources' stock price fell. As of 10:24 a.m. on the 3rd, Shengda Resources dropped by 1.24%, closing at 15.16 yuan per share.

When asked, "Is the trial production period of Honglin Caiyuanzi Gold Mine in the first or second half of July?", Shengda Resources stated on the investor interaction platform on July 2 that the trial production of Honglin Mining's Caiyuanzi Copper-Gold Mine is expected to commence from July to September 2025. For specific details on the trial production, please refer to the company's subsequent periodic reports and other relevant announcements.

In response to the question, "With the gradual mass production of all-solid-state batteries from 2026 to 2028, it is expected that the annual silver usage in EVs will exceed 16,000 mt, leading to a severe shortage. Does the company have plans to stockpile silver in anticipation of price increases?", Shengda Resources responded on the investor interaction platform on July 2:The company's profits primarily come from the mining and selection of non-ferrous metals.The company's currently operating mine resources are concentrated in the central and eastern parts of Inner Mongolia Autonomous Region. Due to climatic factors, the company produces very little in the first quarter. To cope with daily operational expenses during the non-production period of mining enterprises in the first quarter of the following year, and to adopt timely sales strategies for mining products based on the price trends of bulk commodities, the company will reasonably retain some inventory at year-end but will not stockpile in large quantities.

Previously, when asked, "How many mines has your company acquired over the years? Specifically, which mines have already commenced or are about to commence production? With the significant increase in silver prices, what is your company's main source of revenue?", Shengda Resources stated on the investor interaction platform on June 12 that the company is mainly engaged in the mining, selection, and sales of precious metals and non-ferrous metal ores. It has seven mining subsidiaries, including Yindu Mining, Jinshan Mining, Guangda Mining, Jindu Mining, Dongsheng Mining, Honglin Mining, and Deyun Mining. The mines under Yindu Mining, Guangda Mining, and Jindu Mining are silver-lead-zinc mines, while the mine under Jinshan Mining is a silver-gold mine. These four mines are all in production. Among the mines yet to commence production, the production scale stated on the Mining License of Honglin Mining's Caiyuanzi Copper-Gold Mine is 396,000 mt per year, and mine construction is currently underway, with trial production expected from July to September 2025. The production scale stated on the Mining License of Dongsheng Mining's Bayanwula Silver Polymetallic Mine is 250,000 mt per year, and it has entered the infrastructure construction phase, striving to commence production within 2026. The production scale stated on the Mining License of Deyun Mining's Bayanbaolege Mining Area Silver Polymetallic Mine is 900,000 mt per year, and Deyun Mining is currently further conducting exploration work and handling relevant procedures. For details, please refer to Section III "Management Discussion and Analysis" of the company's "2024 Annual Report". The company has not yet conducted hedging for precious metals and non-ferrous metal mining and selection business products this year.

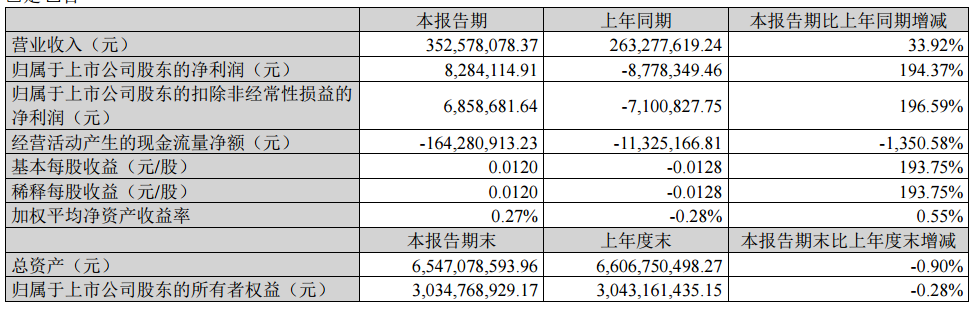

Shengda Resources previously disclosed its Q1 2025 report, showing that the company achieved total operating revenue of 353 million yuan in Q1, up 33.92% YoY. Net profit attributable to shareholders was 8.2841 million yuan, turning profitable YoY, while adjusted net profit was 6.8587 million yuan, also turning profitable YoY. Net cash flow from operating activities was -164 million yuan, compared with -11.3252 million yuan in the same period last year. The increase in Shengda Resources' operating revenue was mainly due to higher sales from mining and processing operations during the reporting period.

Shengda Resources stated in its Q1 report that its subsidiary, Inner Mongolia Jinshan Mining Co., Ltd., received a reply from the Hulunbuir Natural Resources Bureau in January 2025 titled "Reply on the Review and Filing of the Mineral Resource Reserve Verification Report for the Eren Tolgoi Silver Mine in New Barag Right Banner, Inner Mongolia Autonomous Region" (Hu Natural Reserve Letter [2025] No. 01). The review confirmed that the "Mineral Resource Reserve Verification Report for the Eren Tolgoi Silver Mine in New Barag Right Banner, Inner Mongolia Autonomous Region" complied with relevant regulations and was approved for filing. Compared with the previous review, Jinshan Mining's newly approved resource reserves included an increase of 1.8209 million mt in ore resources, 608.67 mt in silver metal content, 5,046.19 kg in associated gold metal content, 7,527.39 mt in lead metal content, and 7,018.44 mt in zinc metal content, while manganese metal content decreased by 87,141.36 mt. The approval of Jinshan Mining's resource reserve verification report marks a phased achievement in its exploration and reserve expansion efforts, which will help extend the mine's service life and provide resource security for long-term development. For details, refer to the company's announcement dated January 13, 2025, titled "Announcement on Subsidiary Jinshan Mining's Resource Reserve Verification Report Passing Review and Filing" (Announcement No.: 2025-002).

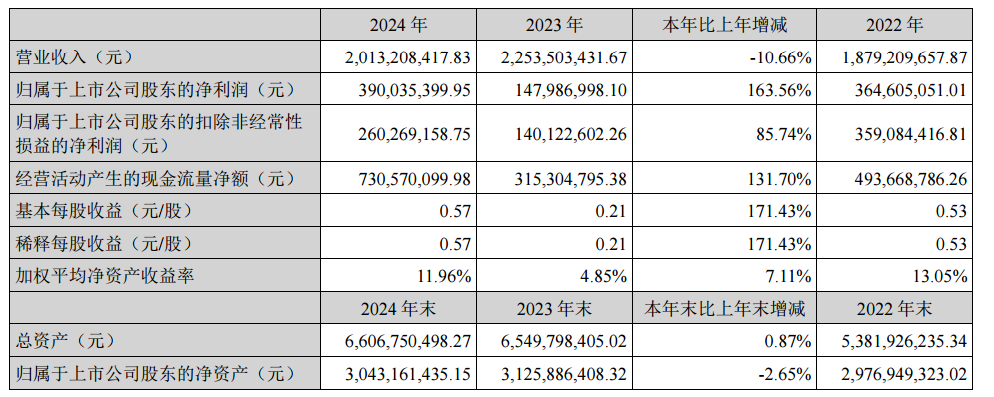

Shengda Resources previously released its 2024 annual report, indicating that its performance was primarily driven by the mining, processing, and sales of precious and non-ferrous metal ores, closely linked to domestic and overseas macroeconomic conditions. Global economic trends, financial market conditions, non-ferrous metal supply and demand, and price fluctuations all impacted the company's operating performance. In 2024, the average spot prices of domestic silver, gold, lead, and zinc rose by 30.94%, 23.87%, 9.67%, and 8.18% YoY, respectively (data source: SMM). Benefiting from higher base metal prices, the average selling prices of the company's mine products increased YoY. Additionally, Jinshan Mining completed its technological transformation and received compensation for litigation-related fund occupation and penalties, leading to a significant YoY improvement in operating performance. In 2024, the company achieved operating revenue of 2,013.2084 million yuan, down 10.66% YoY, including 1,468.7558 million yuan from non-ferrous metal mining and processing (up 15.81% YoY) and 385.0354 million yuan from non-ferrous metal trading (down 51.91% YoY). Net profit attributable to shareholders was 390.0354 million yuan, up 163.56% YoY. In 2025, the company will accelerate the construction and commissioning of relevant mines, while controlling production costs to ensure the achievement of annual production targets. It will also seize the favorable situation of rising metal prices, scientifically formulate sales plans, and maximize the company's operating efficiency.

Shengda Resources' 2024 annual report indicates that the company is primarily engaged in the mining, selection, and sales of precious metals and non-ferrous metal ores. It has seven mining subsidiaries, including Yindu Mining, Jinshan Mining, Guangda Mining, Jindu Mining, Dongsheng Mining, Honglin Mining, and Deyun Mining. Yindu Mining, Guangda Mining, and Jindu Mining are silver-lead-zinc mines, while Jinshan Mining is a silver-gold mine. All four of these mines are currently in operation. Among the mines yet to commence production, Dongsheng Mining has obtained a Mining License for the Bayanwula Silver Polymetallic Mine with a production capacity of 250,000 mt/year. Currently, mine construction is underway. After completion, the mine area will sign a toll processing agreement with Yindu Mining, and the ore will be sold after toll processing by Yindu Mining. Honglin Mining has obtained a Mining License with a production capacity of 396,000 mt/year. Currently, mine construction is underway, and trial production is expected to commence from July to September 2025. Deyun Mining obtained a Mining License in February 2024, with a licensed production capacity of 900,000 mt/year. In addition to the mining right, Deyun Mining also holds an exploration right for the Bayanbaolege District Lead-Zinc Polymetallic Mine, covering an exploration area of 33.2873 square kilometers. Currently, Deyun Mining is further conducting exploration work and handling relevant formalities. Apart from the aforementioned primary mine operations, the company has entered the comprehensive utilization business of solid waste resources containing metals such as nickel and copper through its holding subsidiary, Jinye Environmental Protection, focusing on the resourceful utilization of secondary nickel to continuously enhance economic benefits.

As of December 31, 2024, the resource reserves of each mine under the company are as follows:

Within the scope of the mining license for the Bairindaba Silver Polymetallic Mine of Yindu Mining, the retained main co-existing resources (proven + controlled + inferred) of silver, lead, and zinc include an ore quantity of 5.442 million mt, with a silver metal content of 1,182.5 mt and an average grade of 239.28 g/mt; a lead metal content of 122,208.1 mt and an average grade of 2.74%; and a zinc metal content of 230,457.1 mt and an average grade of 4.73%. The retained associated resources (proven + controlled + inferred) of silver, lead, and zinc include a silver metal content of 34.0 mt and an average grade of 54.49 g/mt; a lead metal content of 5,153.8 mt and an average grade of 0.54%; and a zinc metal content of 3,945.5 mt and an average grade of 0.69%. The retained associated component gold resources (inferred) include an ore quantity of 659,000 mt, a gold metal content of 106.0 kg, and an average grade of 0.161 g/mt; the associated component copper resources (inferred) include an ore quantity of 4.44 million mt, a copper metal content of 7,789.0 mt, and an average grade of 0.175%. The inferred resources of arsenic in associated components include an ore quantity of 5.431 million mt and an arsenic resource quantity of 90,945.0 mt, with an average grade of 1.675%. The inferred resources of sulfur in associated components include an ore quantity of 5.109 million mt and a sulfur resource quantity of 516,661.0 mt, with an average grade of 10.11%.

Within the exploration rights area of the Yindu Mining's Bairindaba (North Mine Area) silver polymetallic mine, the identified resources (proved + probable + inferred) of the paragenetic lead-zinc-silver mine include an ore quantity of 2.049 million mt, a silver metal content of 212 mt, with an average grade of 119.50 g/t; a lead metal content of 20,912 mt, with an average grade of 1.19%; and a zinc metal content of 41,874 mt, with an average grade of 2.09%. The identified resources (proved + probable + inferred) of the paragenetic lead-zinc-silver mine include an ore quantity of 284,000 mt, a silver metal content of 7 mt, with an average grade of 32.41 g/t; a lead metal content of 453 mt, with an average grade of 0.17%; and a zinc metal content of 218 mt, with an average grade of 0.45%. The inferred resources of copper, arsenic, and sulfur in associated components include a copper metal content of 1,500 mt, with a copper component content of 0.10%; an arsenic resource quantity of 14,193 mt, with an arsenic component content of 0.73%; and a sulfur resource quantity of 103,458 mt, with a sulfur component content of 5.28%.

The retained resources (proved + probable + inferred) of the Guangda Mining's Dadi mining area silver-lead-zinc mine include an ore quantity of 3.857 million mt, a silver metal content of 324.3 mt, with an average grade of 165.37 g/t; a lead metal content of 63,013.1 mt, with an average grade of 1.63%; and a zinc metal content of 132,632.1 mt, with an average grade of 3.44%. The retained inferred resources of paragenetic silver include an ore quantity of 1.874 million mt, a silver metal content of 61.2 mt, with an average grade of 31.00 g/t. The retained resources (proved + probable + inferred) of the Jindu Mining's Shidi silver-lead-zinc mine include an ore quantity of 5.454 million mt, a silver metal content of 639.62 mt, with an average grade of 264.64 g/t; a lead metal content of 90,396.3 mt, with an average grade of 1.66%; and a zinc metal content of 94,110.7 mt, with an average grade of 1.73%. The retained inferred resources of paragenetic copper and silver include an ore quantity of 5.454 million mt: a copper metal content of 4,683.9 mt, with a grade of 0.09%; and a silver metal content of 33.18 mt, with a grade of 10.93 g/t.

The retained resources (proved + probable + inferred) of the Dongsheng Mining's Bayanwula mining area silver polymetallic mine include an ore quantity of 2.67 million mt, a silver metal content of 556.32 mt, with an average grade of 284.90 g/t; a lead metal content of 13,052 mt, with an average grade of 1.32%; and a zinc metal content of 46,002 mt, with an average grade of 2.05%. The retained resources (proved + probable + inferred) of paragenetic components include an ore quantity of 2.655 million mt, a silver metal content of 34.06 mt, with an average grade of 50.6 g/t; a lead metal content of 5,522 mt, with an average grade of 0.45%; a zinc metal content of 2,347 mt, with an average grade of 0.77%; a gold metal content of 255 kg, with an average grade of 0.12 g/t; a gallium metal content of 32.01 mt, with an average grade of 12.7 g/t; an arsenic metal content of 11,403 mt, with an average grade of 0.55%; and a pure sulfur quantity of 123,917 mt, with an average grade of 6.18%.

The total identified resources (proven + controlled + inferred) of the industrial orebody at the Caiyuanzi Copper-Gold Mine of Honglin Mining are 6.056 million mt of ore, with 17,049 kg of gold metal content and an average grade of 2.82 g/t; and 29,015 mt of copper metal content with an average grade of 0.48%. The resources of the low-grade orebody (proven + controlled + inferred) are 394,000 mt of ore, with 120 kg of gold metal content and an average grade of 0.30 g/t; and 1,164 mt of copper metal content with an average grade of 0.30%.

The resources and reserves (proven + controlled + inferred) of the silver polymetallic ore at the Bayanbaolege Mining Area of Deyun Mining are 18.11 million mt of ore, with 612 mt of silver metal content and an average grade of 140.45 g/t; 16,620 mt of lead metal content with an average grade of 1.58%; and 361,160 mt of zinc metal content with an average grade of 2.60%. The associated mineral resources (inferred) are 18.063 million mt of ore, with 383.72 mt of silver metal content and a grade of 29.01 g/t; 25,193 mt of lead metal content and a grade of 0.42%; and 20,005.72 mt of zinc metal content and a grade of 0.91%.

The retained resources and reserves (proven + controlled + inferred) within the mining permit scope of the III-IX ore blocks at the Erentaolegai Mining Area of Jinshan Mining are 14.5125 million mt of ore, with 3,076.37 mt of silver metal content and an average grade of 211.98 g/t; 8,988.09 kg of gold metal content and an average grade of 0.62 g/t; and 349,853.09 mt of manganese metal content and an average grade of 2.41%. (Note: The latest resource and reserve verification report of Jinshan Mining was reviewed and filed in January 2025. For details, please refer to the "Announcement on the Review and Filing of the Resource and Reserve Verification Report of the Subsidiary Jinshan Mining" disclosed by the company on January 13, 2025. The resource and reserve data verified this time cannot be used as the basis for calculating the resource and reserve data of Jinshan Mining at year-end 2024, as the review and filing were not completed in 2024. Therefore, the resource and reserve data of Jinshan Mining as of December 31, 2024, did not take into account the increased resource and reserve data in the aforementioned resource and reserve verification report.)

Guosen Securities issued a research report on May 9, giving Shengda Resources an "Outperform" rating. The main reasons for the rating include: 1) The company's net profit attributable to shareholders for 2024 increased by 164% YoY; 2) The company's profitability is seasonal; 3) The technological transformation of Jinshan Mining has been completed, and production in 2025 will no longer be affected by this; 4) The company has significant resource advantages, and gold production is expected to increase significantly after the Caiyuanzi Mine comes into operation. Risk warnings: The project progress may not meet expectations, and there is a risk of volatile metal prices.

Hua'an Securities issued a research report on May 6, giving Shengda Resources a "Buy" rating. The reasons for the rating mainly include: 1) Shengda Resources released its 2024 annual report and the first quarterly report of 2025; 2) The rise in the prices of major metals has driven up the company's profits; 3) Jinshan's technological transformation has been completed + multiple projects are being advanced, with clear subsequent capacity increments. Risk warnings: volatile metal prices; capacity release falling short of expectations; mine safety and environmental protection risks, etc.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)