Although tin is a globally priced commodity, compared to major commodities like copper and aluminum, tin can be considered a minor commodity, as its content in the Earth's crust is relatively low. Global tin resources are concentrated, mainly in China, Indonesia, Myanmar, Australia, etc. In recent years, there have been limited new mines globally, resulting in low supply elasticity. Changes in tin ore supply have caused significant disruptions to the futures market, especially after Myanmar banned tin ore mining in August 2023, when this situation became more pronounced. In the first half of 2025, SHFE tin exhibited a trend of jumping initially and then pulling back, mainly influenced by supply disruptions and changes in macro sentiment.

I. Market Review

In the first stage, from January to early April 2025, SHFE tin showed a continuous upward movement in its center. The most-traded continuous contract rose from 240,000 yuan/mt at the beginning of the year to a peak of 299,990 yuan/mt, just shy of the 300,000 yuan/mt mark, with a gain of 25%. This was influenced by supply disruptions of tin ore from Africa and Myanmar. In early February 2025, SHFE tin surged due to the tense situation in the DRC. On March 14, the tension escalated further when Alphamin Resources, the operator of the Bisie mine in the DRC, announced the suspension of mine operations, pushing tin prices closer to the 290,000 yuan/mt mark. On the other hand, the recovery of tin ore supply from Myanmar has been fraught with difficulties, with an unsmooth resumption process. Meanwhile, an earthquake struck Myanmar on March 28, delaying the resumption meeting and pushing tin prices closer to 300,000 yuan/mt amid supply disruptions.

In the second stage, from after the Tomb-Sweeping Day holiday to the present, tin prices have pulled back from around 300,000 yuan/mt to approximately 260,000 yuan/mt, with a drop exceeding 13%. In early April, the US announced reciprocal tariffs that far exceeded expectations, leading to the spread of market pessimism and a sharp decline in SHFE tin, with the futures market hitting the daily limit down at one point. On April 10, Alphamin Resources announced that its Bisie tin mine in eastern DRC would resume operations, alleviating the supply issue of tin ore. SHFE tin fluctuated sharply, with the futures market dropping to the current year's low of 235,000 yuan/mt. However, as the US government announced a 90-day suspension of reciprocal tariffs on dozens of countries, maintaining the minimum tariff rate at 10%, the tariff suspension offset the impact of the Bisie tin mine's resumption, and SHFE tin rebounded along with major commodities. Subsequently, the market entered a vacuum period, with tin prices fluctuating rangebound around the 260,000 yuan/mt level.

II. Tight Supply in the Present, Clear Expectations for Increased Supply in the Future

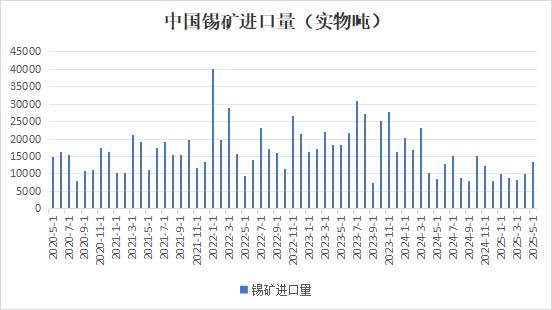

Myanmar is the world's third-largest tin producer (accounting for 15%-20% of global total supply), with its core production area, Wa State, contributing 90% of the country's output and being the "lifeline" of China's tin ore imports. Before the ban, tin ore imports from Myanmar accounted for over 90% of China's total imports. After Myanmar banned tin ore mining in August 2023, China explored import channels such as African tin ore, but could not make up for the loss of tin ore imports from Myanmar. Starting from Q2 2024, China's tin ore imports have plummeted, maintaining a low level this year. According to data from the General Administration of Customs of China, in May 2025, China's tin ore imports reached 13,400 mt (equivalent to approximately 6,518 mt (metal content)), up 36.39% MoM and 59.84% YoY, with an increase of 2,182 mt (metal content) compared to April (which was equivalent to 4,336 mt (metal content)). The cumulative imports from January to May totaled 50,200 mt, down 36.51% YoY. The import volume in May hit a new high for the year, primarily driven by increased contributions from African countries. Imports from the Democratic Republic of the Congo and Nigeria increased by 26.0% and 168.0% MoM, respectively. The total imports from Africa exceeded 3,660 mt (metal content), accounting for over 50% of the total imports. Australia's imports were around 902 mt (metal content), maintaining a relatively stable level. Myanmar's imports in May were less than 700 mt (metal content), with the annual import share dropping below 30%. Despite the rebound in import volume in May, the cumulative physical imports of tin concentrates from January to May were 10,000 mt, with overall supply remaining at historically low levels. The long-term gap caused by the mining ban in Myanmar has not yet been fully filled.

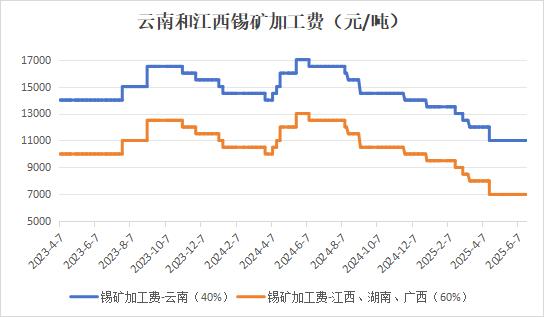

The tight domestic tin ore situation has intensified, with tin smelting processing fees continuing to decline. The decline accelerated further after February 2025. Currently, the processing fee for 40% grade tin concentrates in Yunnan is 11,000 yuan/mt, while in Jiangxi and other regions, it is 7,000 yuan/mt for 60% grade tin concentrates. Due to the persistent shortage of domestic tin concentrate raw materials, the production of some smelters has been affected. According to an SMM survey, the weekly operating rates of refined tin smelters in Yunnan and Jiangxi have remained low. As of June 27, the combined operating rate of the two provinces was only 50.97%. The processing fee for 40% grade tin concentrates in Yunnan has approached the cost line of smelters, severely squeezing profit margins. Some enterprises have been forced to cut production or undergo maintenance. Jiangxi's recycled tin industry is facing a raw material shortage crisis. Jiangxi smelters mainly rely on scrap tin recycling, but the recycling volume of scrap materials after the Chinese New Year has been less than 70% of the annual average. The supply of electronic scrap has declined by 30% MoM. The production pace of the electronics and home appliance industries has slowed down due to cost pressures, reducing the circulation of scrap materials and forming a negative feedback loop. Coupled with policy uncertainties (such as adjustments to renewable resource policies), the raw material gap has been exacerbated. The sorting cost of scrap materials has risen, while the processing fees for tin concentrates have declined, hurting the profits of recycled tin smelting. Some production capacity may permanently exit the market.

In H1 2025, the resumption of tin ore production in Myanmar was a core factor affecting the supply side, but the resumption process has been relatively unsmooth. Starting from the beginning of this year, the resumption of tin ore production in Myanmar has gradually been put on the agenda. On February 26, the Wa State Industrial and Mineral Administration Bureau issued a document titled "Procedures for Handling Mining, Beneficiation Plant, and Prospecting License Applications," which essentially provided explicit regulations for mine area license applications. Most market participants interpreted this as a signal for the resumption of production in Myanmar's Wa region. Following the announcement, SHFE tin prices plummeted on the same day. However, due to the unclear progress of production resumption in Myanmar and the suspension of tin ore operations in the DRC, tin prices regained upward momentum. On March 28th, a 7.9-magnitude earthquake struck Myanmar. Affected by the earthquake, the production resumption symposium originally scheduled for April 1st was postponed, further exacerbating supply concerns and driving prices to new highs in recent years. On April 23rd, 2025, the production resumption meeting in Wa region was reconvened, during which relevant documents were announced and relevant work processes were clarified. However, after the symposium, the authorities still did not issue a clear signal for a comprehensive resumption of production. According to SMM, the current progress of production resumption in Myanmar's Wa region has stalled, coupled with transportation difficulties during the rainy season, leading to a continuous decline in tin ore imports from Wa region. Meanwhile, due to Thailand's transportation ban, the southern part of Myanmar has seen a monthly reduction of 500-1,000 mt (metal content) in tin ore supply.

Overall, although Wa region is actively promoting the resumption of work and production, the overall progress remains slow. It mainly faces the following issues: Firstly, the cost of key materials has risen sharply. The prices of materials used in mining and beneficiation processes, such as explosives and beneficiation reagents, have increased significantly, which will significantly raise the comprehensive mining costs of mines. Secondly, the average grade of tin ore in the mining area has declined, dropping from around 1% before the suspension to approximately 0.5%, posing a severe challenge to resource quality. Thirdly, Wa region previously revised its taxation system to a 30% in-kind tax. Given the low inventory levels of the Wa regional government, priority may be given to rebuilding government inventories. Even if tin ore exports from Wa region resume in the future, it may be difficult to reach the pre-suspension levels in the short term. Overall, the supply of tin ore still maintains a situation of strong reality and weak expectations. The short-term supply of raw materials remains tight, while the long-term trend of increased supply is relatively clear. However, the magnitude and time window remain uncertain, with the focus still on the pace of production resumption in Myanmar.

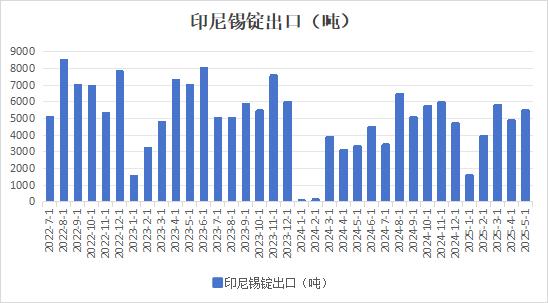

Indonesia, as the world's second-largest country in terms of onshore tin reserves, boasts tin reserves exceeding 800,000 mt, accounting for 17% of the global total. The average grade of tin ore in China's Yunnan province has dropped to 0.3%, while the mining area in Myanmar's Wa region remains stalled due to the mining ban policy. As a result, Indonesia has become an important alternative source of global tin supply. Indonesia harbors million-ton-level submarine placer tin deposits, with reserves potentially meeting global industrial demand for over 15 years. Currently, 94% of Indonesia's tin ingots flow into the international market, with Asia (including China), Europe, and North America accounting for 72%, 18%, and 10% respectively. It is worth noting that the Indonesian government is accelerating the implementation of the "Non-Ferrous Metals Downstream Strategy Plan", aiming to drive the construction of high-value-added product (such as electronic solder and PV welding strip) capacities by restricting the export of primary products (such as tin ingots). This policy orientation may reshape the global tin industry chain division of labor. At the beginning of 2024, influenced by the slow approval of export quotas, Indonesia's tin ingot exports were almost nil. Similarly affected by policies at the beginning of this year, in January 2025, Indonesia's tin ingot exports plummeted to 1,560 mt, with a MoM decline of 66.57%, mainly attributed to seasonal maintenance at smelters and delays in export license approvals. Tin ingot exports gradually recovered in February. From January to May 2025, Indonesia exported 21,600 mt of tin ingots, up 110% YoY, but still down 10% compared to the same period in 2023. The core contradiction in Indonesia's restricted exports lies in the intensified enforcement of policies. In 2024, the customs implemented a "resource tax ticket traceability verification" mechanism, coupled with the spillover effects of the nickel ore resource tax adjustment plan in 2025 (the nickel ore resource tax linked to the HMA price model may extend to the tin ore sector), leading to a significant increase in compliance costs for smelters. It remains to be seen whether subsequent policy adjustments in Indonesia will affect tin ingot exports.

III. Weak Terminal Consumption: High Tin Prices Suppress Demand

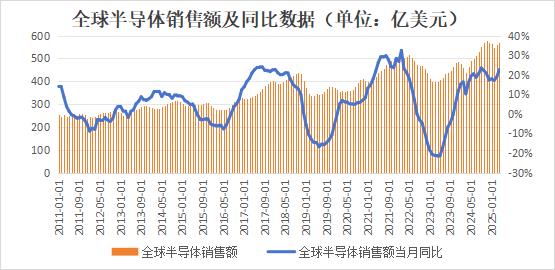

Global semiconductor sales exhibit cyclical changes. This semiconductor cycle bottomed out in February 2023, with YoY growth in sales turning positive in November 2023. Since then, the growth rate has been climbing, but it has gradually slowed down after October 2024. Sales rebounded somewhat on a MoM basis in March-April 2025. This global semiconductor cycle is driven by AI computing power construction, mainly in advanced processes. Therefore, the core beneficiaries are concentrated overseas, while domestic capacity is mainly in mature processes, with limited driving effects. Domestic semiconductor downstream industries are more concentrated in consumer electronics, automotive, and other fields. In H1 2025, the global consumer electronics market growth rate slowed down, with global/China smartphone market shipments up 1.5%/3.3% YoY in Q1 2025. IDC predicts that global smartphone shipments will continue to grow in 2025, but at a slower pace. Global PC shipments were up 4.9% YoY in Q1 2025, and IDC expects that full-year demand in 2025 may face challenges.

Domestically, from January to April 2025, 94.708 million mobile phones were shipped in the domestic market, up 3.5% YoY, showing a weak recovery pattern. Since 2024, the state has introduced a "trade-in" subsidy policy, which has to some extent stimulated the growth of consumer electronics products. However, due to the lack of sustained strong demand, the recovery in demand has been limited. As the stimulating effect of the subsidy policy diminishes, signs of subsidy withdrawal have emerged in some regions, and the sustainability of subsequent growth in consumer electronics remains to be observed.

In the PV sector, in January 2025, the National Energy Administration issued the "Administrative Measures for the Development and Construction of Distributed PV Power Generation," further standardizing the construction management of domestic distributed installations. According to this document, April 30, 2025, is the dividing point for the implementation of the old and new policies. Existing projects that completed registration before this time still enjoy the original subsidy and grid connection policies, while new projects implemented fully market-based rules thereafter. Industrial and commercial distributed PV projects connected to the grid before April 30 could be fully connected to the grid and enjoy higher subsidized electricity prices. For projects connected to the grid after this date, general industrial and commercial distributed PV projects of 6 MW and below could no longer opt for full grid connection and could only choose self-consumption with surplus electricity fed into the grid. Large industrial and commercial distributed PV projects exceeding 6 MW were required, in principle, to be fully self-consumed, with no surplus electricity fed into the grid. However, in areas with spot electricity markets, surplus electricity could be fed into the grid and traded. This document posed a certain negative impact on large industrial and commercial installation projects and triggered the "April 30" installation rush effect.

On February 9, 2025, the National Development and Reform Commission (NDRC) and the National Energy Administration jointly issued the "Notice on Deepening the Market-Oriented Reform of New Energy On-Grid Tariffs to Promote High-Quality Development of New Energy," proposing to promote the participation of new energy on-grid electricity in market transactions. Starting from May 31, 2025, incremental distributed PV projects entered the market comprehensively, and all new projects were required, in principle, to have all their electricity traded in the power market, with electricity prices formed through market bidding, and subsidies completely phased out. At the same time, a "price settlement mechanism for the sustainable development of new energy," namely, a "more refunds, less supplements" differential settlement mechanism, was established to stabilize yield expectations. This directly affected the yield of installation projects and triggered the "May 31" installation rush effect.

In the first half of 2025, driven by the "April 30" and "May 31" installation rush effects, China's newly added PV installation capacity surged significantly. Statistics released by the National Energy Administration showed that from January to May 2025, the cumulative newly added PV installation capacity reached 197.85 GW, up 88.55% MoM and 149.97% YoY. In May 2025, the newly added PV installation capacity was 92.92 GW, up 105.48% MoM and 388.03% YoY.

From a vertical comparison perspective, China's newly added PV installation capacity reached 277.57 GW for the full year of 2024 and 216.3 GW for the full year of 2023. The newly added installation capacity in the first half of 2025 approached the 200 GW level, close to the full-year installation capacity of 2023. The superposition of the "April 30" and "May 31" installation rushes greatly stimulated a "blowout" in the PV installation market. However, the subsequent policy "vacuum period" might trigger a rapid market cooling, with concerns about overdrawing on installation demand in the second half of the year.

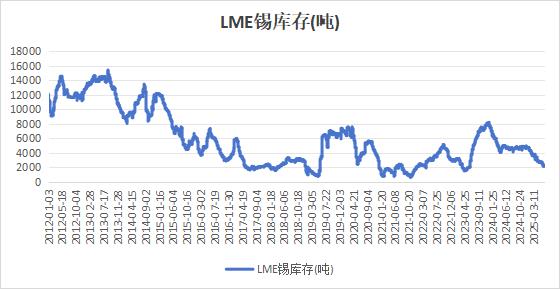

Against the backdrop of weak end-use demand, downstream procurement was relatively cautious and price-sensitive. Tin prices, supported by costs, remained high, exerting a significant inhibitory effect on the downstream. Buyers tended to restock when prices declined and adopted a wait-and-see attitude after prices rose. After experiencing significant destocking of domestic and overseas tin ingot inventories in 2024, inventory changes diverged in the first half of this year, possibly reflecting stronger overseas demand than domestic demand. LME tin inventories continued to decline, dropping from 4,700 mt at the beginning of the year to 2,145 mt, a decrease of over 50%, reaching a relatively low historical level. Domestic social inventories first rose and then fell. As of June 27, they had increased by 3,000 mt compared to the beginning of the year.

Looking ahead, the core contradiction in the tin market still lies on the supply side, with tin ore supply facing a situation of tight immediate supply but expected increases in the future. In the short term, supply recovery is still time-consuming due to the slow pace of production resumption in Myanmar. The Bisie mine in the DRC has now returned to normal production. In local time May, only part of the early-stage mine inventories were shipped, and the new mining output in June has not yet been shipped. It is expected that tin ore imports in June may only decline slightly, and tin ore imports in the first half of 2025 may remain flat MoM. The second half of the year will enter the verification stage for the recovery of tin ore supply in Myanmar, with the timing and scale of production resumption becoming the focus of market competition. On the demand side, the growth rate of the global consumer electronics market slowed down in the first half of 2025, with weak growth in global smartphone and PC shipments. The installation rush for domestic PV projects ended in mid-year, possibly depleting some installation demand in the second half of the year. In the short term, before tin supply recovers, tin prices are expected to maintain a relatively strong oscillating pattern. However, as production resumption in Myanmar's tin mines progresses and transportation of tin mines in Africa resumes, the center of tin prices may shift downward.

(Wenhua Comprehensive)

![The Most-Traded SHFE Tin Contract Opened Lower and Then Traded Stronger, Spot Market Recovers Amid Downtrend [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/WWXJU20251217171753.jpg)

![The most-traded SHFE tin contract fluctuated rangebound during the night session, with downstream enterprises mostly following up with small-lot transactions. [SMM Tin Morning Brief]](https://imgqn.smm.cn/usercenter/bYFQn20251217171752.jpg)