Non-ferrous

Non-ferrous

Base Metals

Rare Earth

Scrap Metals

Minor Metals

Precious Metals

New Energy

Price CenterDatabaseProReportsEventsCar Insight

SMM June 30 Report:

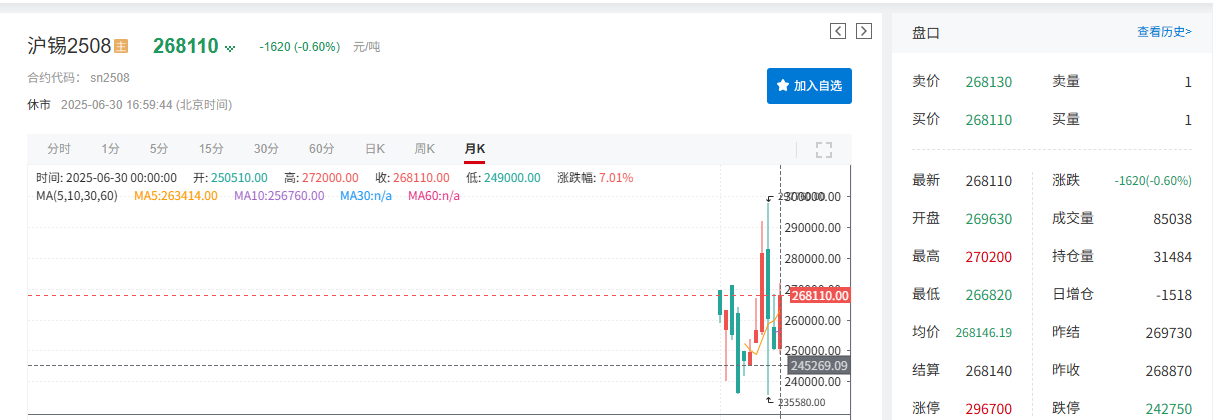

Expectations for US Fed interest rate cuts have heated up, coupled with the Trump administration's interference in monetary policy, sparking concerns about the Fed's independence. The US dollar index weakened under pressure in June. As the US dollar generally moves inversely with commodity prices, this boosted tin prices. On the fundamentals side, the progress of production resumptions in Myanmar fell short of expectations, and the current tight domestic ore supply situation, along with changes in the supply-demand pattern, provided strong support for tin prices, enabling them to break free from two consecutive monthly declines. As of around 17:00 on June 30, SHFE tin fell by 0.6%, closing at 268,110 yuan/mt, with a monthly gain of 6.01% in June. LME tin fell by 0.11%, closing at $33,725/mt, with a temporary monthly gain of 10.92% in June.

》Click to view SMM Futures Data Dashboard

Spot Market

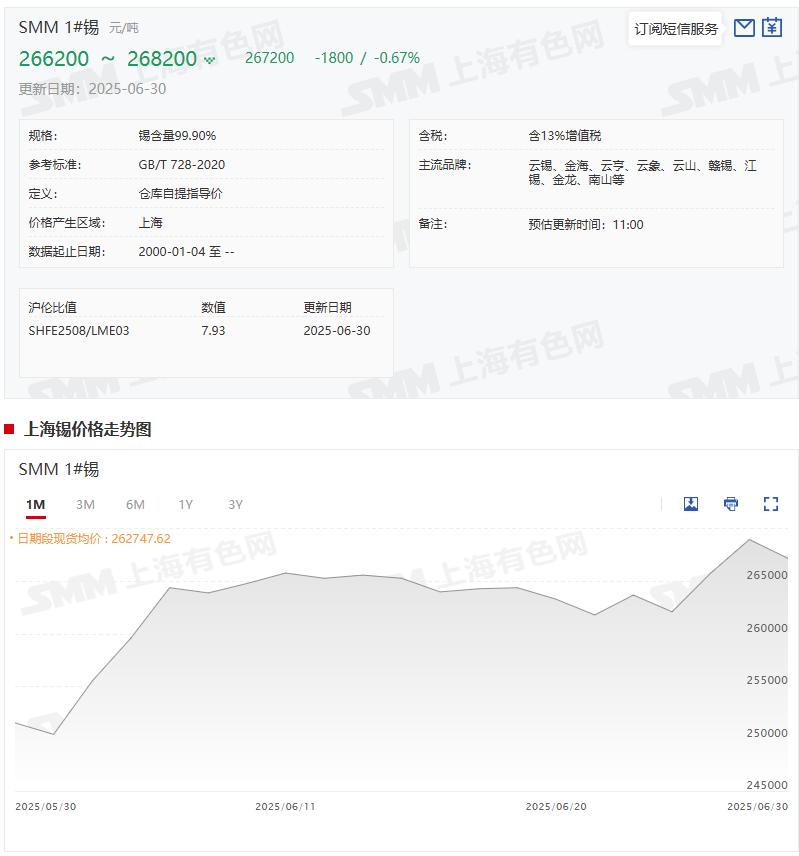

Tin spot prices break free from two consecutive monthly declines, rising over 6% in June

》Subscribe to view SMM Metal Spot Historical Prices

Tin spot prices: According to SMM quotations, SMM 1# tinThe average spot price on June 30 was 267,200 yuan/mt, compared to an average price of 251,500 yuan/mt on May 30, an increase of 15,700 yuan/mt or 6.24%.

Fundamentals

►Production:

Affected by factors such as raw material shortages, cost pressures, and regional production disruptions, refined tin production in June fell by 6.94% MoM.

According to SMM's market-based processing data, in June 2025, China's refined tin production fell by 6.94% MoM and by 15.2% YoY. This production cut was mainly influenced by multiple factors such as raw material shortages, cost pressures, and regional production disruptions. A detailed regional analysis is as follows:

According to data from the General Administration of Customs, China's physical imports of tin concentrates reached 13,449 mt in May 2025. Despite Myanmar being China's largest importer of tin ore, imports from Myanmar remained sluggish. Although Myanmar was once China's largest importer of tin ore, affected by the mining ban policy in August 2023 and the delayed production resumptions in the Wa region in 2025, Myanmar's imports in May were less than 700 mt (metal content), and its share of annual imports has dropped below 30%. Although imports rebounded in May, the cumulative physical imports of tin concentrates from January to May were 10,000 mt, with overall supply remaining at historically low levels. The long-term gap caused by Myanmar's mining ban has not yet been fully filled. Yunnan region: The most severe raw material shortage: Smelter raw material inventories are generally below 30 days, with intense competition for tin ore procurement. Some enterprises have experienced inventory backlogs due to high-price stockpiling, but weak downstream demand has suppressed shipments. Prominent cost pressures: The processing costs for low-grade ores are high, coupled with rising electricity costs, leading to a further reduction in enterprise operating rates. Jiangxi region: **Supply chain disruption for scrap**: The tin scrap recycling system is under pressure, with secondary material circulation in the market decreasing by over 30%. Insufficient crude tin supply directly led to a decline in refined production. **Risk of capacity withdrawal**: Small and medium-sized secondary smelters face production halts due to sustained losses, passively increasing industry concentration. Anhui and other regions: **Dual raw material shortage**: Weak supply of both tin concentrates and tin scrap has kept operating rates below 70% of planned capacity for an extended period. Some companies plan maintenance, further suppressing production. 》Click for details

►Imports:

May imports rebounded but overall supply remains at historically low levels

China's tin ore imports in May reached 13,400 mt (equivalent to 6,518 mt metal content), up 36.39% MoM and 59.84% YoY, an increase of 2,182 mt metal content from April (4,336 mt metal content in April). January-May cumulative imports totaled 50,200 mt, down 36.51% YoY. Tin ingot imports in May were 2,076 mt, up 84.04% MoM and 225.9% YoY. January-May cumulative imports reached 9,584 mt, up 38.48% YoY.

According to General Administration of Customs data, China's tin concentrate imports (physical content) in May 2025 hit 13,449 mt, a yearly high. This growth was mainly driven by increased contributions from African countries: DRC and Nigeria saw import volumes rise 26.0% and 168.0% MoM, respectively. African imports totaled over 3,660 mt metal content, accounting for more than 50% of total imports. Australia maintained relatively stable imports at around 902 mt metal content. Myanmar imports remained sluggish. Despite being China's top tin ore import source historically, Myanmar's imports fell below 700 mt metal content in May due to the August 2023 mining ban and delayed production resumptions in Wa State in 2025. Its annual import share has dropped below 30%. Although May imports rebounded, January-May cumulative tin concentrate imports (physical content) stood at 10,000 mt, keeping overall supply at historically low levels. The long-term gap caused by Myanmar's mining ban remains unfilled.

►Inventory:

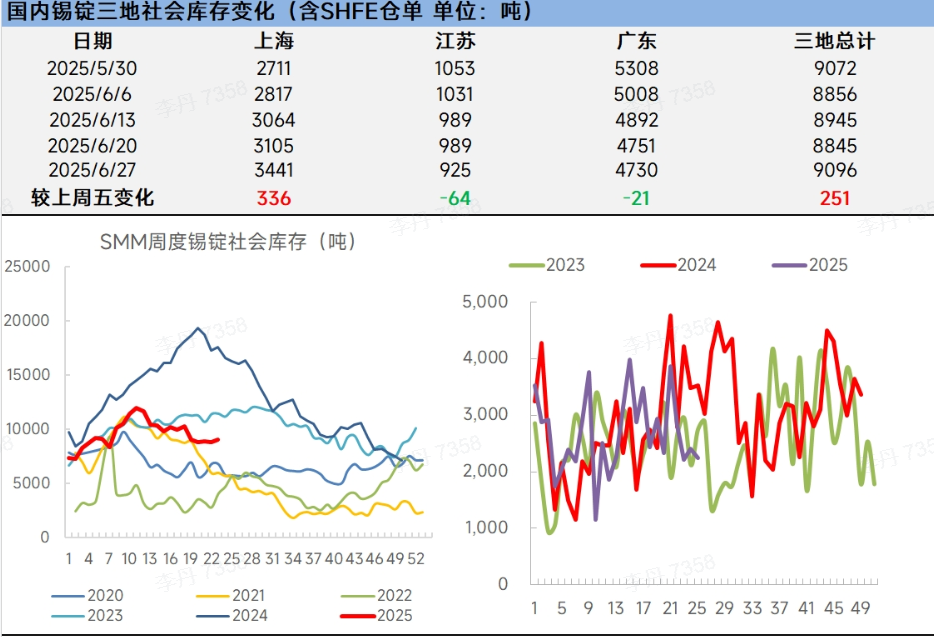

SMM tin ingot social inventory across three regions increased slightly while LME tin inventory declined significantly

》Click to view SMM tin industry chain database

Domestic tin ingot social inventory: Last week, the spot tin ingot market saw sluggish trading and slight inventory buildup amid high price volatility, persistently weak demand, and dual supply-demand weakness. Short-term inventory pressure may persist, with attention needed on Myanmar's production resumption progress, seasonal recovery in end-use demand, and macro policy changes.

LME tin inventory: LME tin inventory stood at 2,175 mt on June 30, compared to 2,680 mt on May 30, marking a significant 18.84% decline in June.

SMM Outlook

Macro: As the Political Bureau meeting approaches, market expectations for enhanced domestic macro policy support are likely to bolster tin prices. Should US July non-farm payrolls and CPI data weaken, coupled with the US Fed signaling "preventative interest rate cuts," the US dollar may soften further, benefiting tin and other commodities. Future market movements will require monitoring of Sino-US inflation data, global PMI figures, and the Fed's July policy meeting guidance on interest rate trajectories. Additionally, with the temporary tariff suspension window nearing expiration, policy adjustments warrant vigilance regarding potential market sentiment disruptions.

Fundamentals: Supply side: Based on SMM calculations, some Yunnan and Jiangxi smelters have concluded maintenance shutdowns and gradually resumed production, with July refined tin output projected to rebound MoM. While Myanmar's tin mine production resumptions have lagged behind expectations and May tin imports recovered, the long-term supply gap from Myanmar's mining ban remains unfilled, maintaining tight raw material supply. Inventory dynamics: Despite minor domestic inventory buildup, overall levels remain at historically low seasonal levels, with LME tin stocks hovering near two-year relative lows. As of the week ending June 20, SHFE tin inventories continued declining, reaching a four-month low.

In summary, July represents a critical window for policy expectations versus economic data interactions, requiring close attention to macroeconomic trends' influence on tin prices. Fundamentally, tight raw material supply combined with depressed global tin inventories will provide underlying support. Should macroeconomic conditions remain supportive alongside these fundamentals, tin prices are positioned to hold up well.

Recommended Readings:Z35/>》[SMM Analysis] June 2025 China Refined Tin Industry Performance Analysis and Trend Outlook

》[SMM Data] June 30, 2025 Regional Breakdown of Social Tin Ingot Inventories

For queries, please contact Lemon Zhao at lemonzhao@smm.cn

For more information on how to access our research reports, please email service.en@smm.cn