Zijin Mining announced on June 30: Its wholly-owned subsidiary, Zijin Gold International Limited (the entity to be spun off and listed on the Hong Kong Stock Exchange), and its wholly-owned subsidiary in Singapore, Jinha (Singapore) Mining Co., Ltd., signed an agreement with Cantech S.à.r.l. on June 29, 2025, Beijing time. Jinha Mining intends to acquire 100% of the interests in RGGold LLP and RGProcessing LLP held by Cantech, thereby obtaining 100% of the interests in the Raygorodok gold mine project in Kazakhstan. The transaction is based on September 30, 2025, as the valuation date, and the acquisition consideration is determined to be $1.2 billion on a "cash-free, debt-free" basis for the target company as of the valuation date. The specific acquisition consideration to be paid will be adjusted by the parties to the transaction based on the actual cash, working capital, and interest-bearing liabilities in the financial statements as of the valuation date.

According to Zijin Mining's announcement, the shareholders of Cantech are VGroup International S.A. (holding 65%), managed by and with Verny Capital, one of Kazakhstan's largest equity investment companies, serving as the investment advisor, and RCF VII–RGGold S.a.r.l. (holding 35%), under Resource Capital Funds, a US private equity firm focusing on mining and resource investments.

Regarding the overview of the RG gold mine project, Zijin Mining's announcement states:1. Natural Geography and InfrastructureThe RG gold mine project is located in the Burabay region of Akmola state in northern Kazakhstan, approximately 70 kilometers from Shchuchinsk city, 40 kilometers from the highway, and 66 kilometers from the railway station, with convenient transportation. The mining area features a hilly landscape with an elevation of 350-500 meters. The annual temperature fluctuates significantly, with a total annual precipitation of 320 millimeters, belonging to a typical arid continental climate. The project is an operating mine with good production infrastructure conditions for water supply, power supply, and communications.

2. Mining RightsThe core mining rights of the RG gold mine are based on the "Exploration and Gold Mining License Agreement in the Novodneprovka Area of the Burabay District, Akmola State" (No. 486) signed by RGG with the Ministry of Industry and Construction of Kazakhstan in June 2000, as well as 19 subsequent supplementary agreements. The mining rights are valid until December 31, 2040, and can be renewed before expiration if conditions such as reasonable resource utilization are met. The project also holds six exploration rights. RGG holds 100% of the aforementioned mining rights.

3. Resource ReservesThe RG gold mine consists of two deposits, north and south. According to the technical report submitted by AMC in October 2024, using a cut-off grade of 0.3 g/t for gold in oxidized and transitional ores and 0.5 g/t for gold in primary ores,the resource and reserve estimates for the RG gold mine as of the end of 2023 are as follows: The RG gold mine project has a total resource (at a gold price of $2,000/ounce) of 241 million mt of ore at an average grade of 1.01 g/t of gold, with a total metal content of 242.1 mt of gold. The retained reserves within the originally planned open-pit mining boundary of the RG Gold Mine (with a gold price of US$1,750 per ounce) are as follows: ore quantity of 94.9 million mt, an average gold grade of 1.06 g/mt, and a gold metal content of 100.6 mt. Given the current gold price context, it is entirely feasible to optimize the open-pit mining boundary, further enhancing the resource utilization rate within the boundary and expanding the production scale of the mine.

4. Mine Development Status and PlansThe RG Gold Mine project is an active open-pit mine, comprising two open pits, North and South, located 2 kilometers apart. Currently, both pits have a mining depth of approximately 130 meters. The open-pit mining operation is stable, with detailed mining and stripping plans in place. The ore types in the open-pit mine include oxidized ore, mixed ore, and primary ore. In 2016, the project completed the construction of a heap leaching system for ore processing, primarily targeting oxidized ore. In 2022, a new carbon-in-pulp (CIP) cyanidation beneficiation plant was commissioned to process primary ore, with the end-use product being dore gold (gold bullion). From 2022 to 2024, the project's gold production was 2.0 mt, 5.9 mt, and 6.0 mt, respectively. In 2024, the project's mine cash cost was US$796 per ounce (excluding heap leaching). According to data provided by the original owner, the project has a remaining service life of 16 years (from 2025 to 2040), with an average annual gold production of approximately 5.5 mt. Based on preliminary research by the company's technical team, the optimized mining and beneficiation scale of the project can be increased to 10 million mt per year. Through measures such as optimizing the open-pit mining boundary and adjusting the beneficiation process, the project's production and economic benefits are expected to further improve.

When introducing the main contents of the agreement, Zijin Mining mentioned that the seller, Cantech, agreed to sell 100% of the interests in RGG and RGP to the buyer, Jinhua Mining. After the signing of this agreement, Jinhua Mining will establish a wholly-owned subsidiary at the Astana International Financial Centre (AIFC) in Kazakhstan as the entity for the transfer of interests.

Regarding the impact of this transaction on the company, Zijin Mining stated: The RG Gold Mine has a significant resource volume, being a large-scale active open-pit mine with a long service life and well-developed infrastructure. The project's beneficiation process is mature, with low comprehensive costs and strong profitability. There is still room for further improvement in production and operation. The acquisition will contribute to the company's production and profitability in the year of the transaction. The expected investment payback period is short, with good economic benefits. This transaction aligns with the company's strategic orientation of increasing mergers and acquisitions of major resource projects in countries surrounding China. Kazakhstan offers a favorable investment environment for mining. The RG Gold Mine will form a good synergistic effect with the company's Jilau/Taluo Gold Mine in Tajikistan and the Zuoan Gold Mine in Kyrgyzstan, helping the company to further deepen its presence in the mineral resource-rich Central Asia region and optimize its global resource allocation. The transaction will be conducted through Zijin Gold International, the entity to be spun off, as the investment vehicle. If the RG mine is successfully acquired, it will significantly enhance Zijin Gold International's asset scale, profitability, and global industry standing, facilitating its listing on international capital markets. The deal aligns with the company's development strategy, further enriching its gold resource reserves, rapidly increasing gold production, and accelerating the achievement of its 2028 production target.

Zijin Mining also highlighted investment risks: the transaction is subject to uncertainties, and its final completion requires fulfillment of certain conditions, including routine antitrust reviews and regulatory approvals; the regulatory environment and policy changes in the project's location may introduce operational uncertainties; the project's economic performance will be affected by gold price fluctuations.

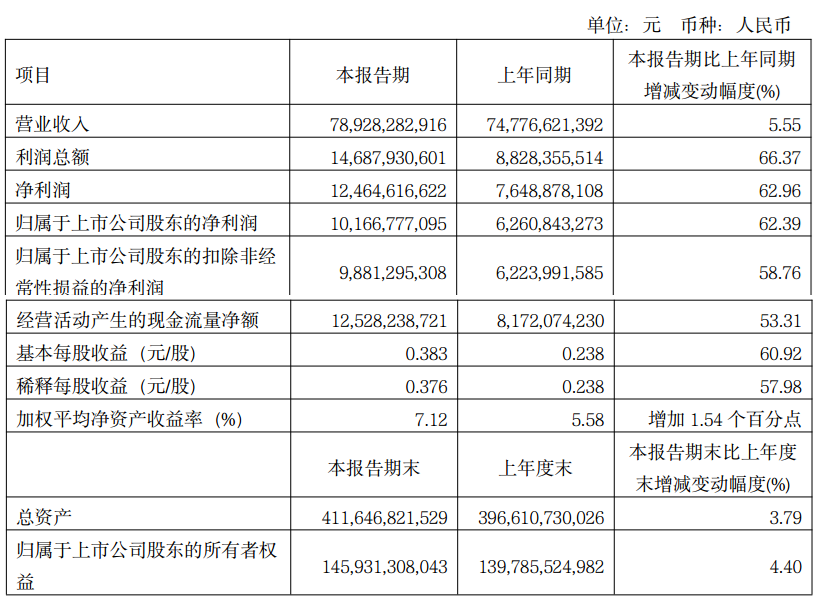

Zijin Mining previously disclosed its Q1 2025 report, showing operating revenue of 78.928 billion yuan, up 5.55% YoY, and net profit attributable to shareholders of 10.167 billion yuan, up 62.39% YoY. The company attributed the profit growth to improved production and operational management capabilities, increased output of key mineral products, and enhanced market analysis capabilities, allowing it to fully benefit from rising metal prices.

Key operational data from Zijin Mining's Q1 report: gold production increased 13% YoY, copper production rose 9% YoY, while zinc production declined 10% YoY, January-March. Revenue reached 78.928 billion yuan, up 6% YoY, with net profit attributable to shareholders of 10.167 billion yuan, up 62% YoY. Mine gross margin stood at 59.94%, up 5.44 percentage points YoY. Sequentially, gold production increased 2% QoQ, copper production rose 3% QoQ, while zinc production fell 9% QoQ. Revenue increased 8% QoQ to 78.928 billion yuan, and net profit attributable to shareholders grew 32% QoQ to 10.167 billion yuan. Mine gross margin in Q1 2025 was 59.94%, up 1.23 percentage points QoQ. During the reporting period, unit sales costs of mineral products rose due to lower ore grades, increased transportation distances, and higher stripping ratios at some open-pit mines.

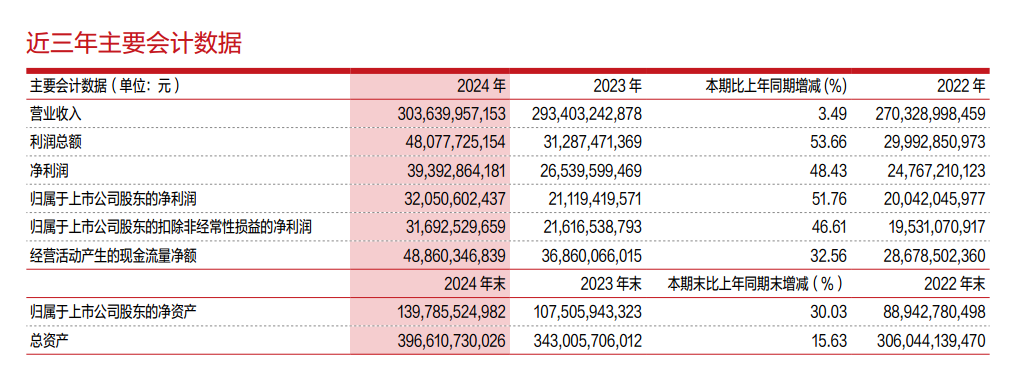

Zijin Mining's 2024 annual report showed revenue of 303.640 billion yuan, up 3% YoY, and net profit attributable to shareholders of 32.051 billion yuan, up 51.76% YoY. In 2024, the company's main mineral product resources and production continued to grow year after year, with both volume and price rising. Copper ore production exceeded the 1 million mt milestone and continued to grow, while gold ore production increased rapidly. The company achieved annual production of 1.07 million mt of copper ore, 73 mt of gold ore, 450,000 mt of zinc (lead) ore, and 436 mt of silver ore. Among them, the YoY growth rates of copper ore and gold ore production were 6% and 8%, respectively. Despite the widespread cost pressures in the global mining industry, Zijin Mining reshaped its comparative advantage of low costs and high efficiency, effectively curbing the upward trend in costs. The sales costs of copper concentrates and gold concentrates decreased by 4.3% and 0.43% MoM, respectively, continuing to rank among the lowest in the global mining industry. Major economic indicators reached new highs, with strong profitability. During the reporting period, the company achieved earnings before interest, taxes, depreciation, and amortization (EBITDA) of 63.2 billion yuan, total profit of 48.1 billion yuan, and net profit attributable to the parent company of 32.1 billion yuan, representing significant YoY increases of 36%, 54%, and 52%, respectively. The net cash flow generated from operating activities was 48.9 billion yuan, up 33% YoY, indicating robust and ample cash flow. At the end of the period, total assets were 396.6 billion yuan, including 139.8 billion yuan of net assets attributable to the parent company, representing increases of 16% and 30%, respectively, compared to the beginning of the period. The asset-liability ratio decreased to 55%, optimizing the asset structure.

In its 2024 annual report, Zijin Mining outlined the production plans for its main mineral products in 2025:1.15 million mt of copper ore, 85 mt of gold ore, 440,000 mt of zinc (lead) ore, 40,000 mt of lithium carbonate equivalent, 450 mt of silver ore, and 10,000 mt of molybdenum ore. Given the complex and volatile market environment, this plan serves as a guiding indicator and is subject to uncertainties. It does not constitute a commitment to achieving the production targets. The company reserves the right to make corresponding adjustments to this plan based on changes in circumstances. Investors are advised to pay attention to the risks involved.

A research report on Zijin Mining issued by China Post Securities on June 2 stated that Zijin Mining announced its intention to spin off its majority-owned subsidiary, Zijin Gold International, for listing on the main board of the Hong Kong Stock Exchange. Prior to the implementation of this spin-off, Zijin Mining plans to integrate multiple overseas gold mine assets under Zijin Gold International, with the relevant restructuring work currently in progress. After the completion of this spin-off, Zijin Mining's equity structure will remain unchanged, and it will continue to maintain control over Zijin Gold International. Integrating high-quality gold mine resources, the company is taking a further step towards globalization. The assets proposed for spin-off and listing consist of eight world-class large-scale gold mines located in South America, Central Asia, Africa, and Oceania. As of the end of 2024, these eight mines had a total gold reserve of 697 mt and a resource volume of 1,800 mt, with a combined production of 46.22 mt in 2024. The net profits for 2022-2024 were 2.12 billion yuan, 2.31 billion yuan, and 4.46 billion yuan, respectively, while the net assets were 16.68 billion yuan, 18.59 billion yuan, and 21.14 billion yuan, respectively. Zijin Gold International will continue to leverage the company's leading experience in mine mergers and acquisitions and mine operations to achieve continuous reserve growth and efficient development of overseas gold mine resources, further promoting a high-quality global strategic layout. The launch of an employee stock ownership plan demonstrates the company's confidence in its development. China Post Securities stated: With the steady upward movement of the gold price center and copper prices fluctuating at highs, the company's copper and gold production and sales have steadily increased. It is expected that the net profit attributable to shareholders will be RMB 40.565 billion/44.045 billion/50.011 billion, with a year-on-year (YOY) growth rate of 26.57%/8.58%/13.54%, corresponding to a price-to-earnings (PE) ratio of 11.68/10.75/9.47. If the company successfully spins off its gold subsidiary for listing on the Hong Kong Stock Exchange, it is expected to reshape the valuation of its gold business. Risk warnings: The gold price may fall unexpectedly, the company's project progress may not meet expectations, and the spin-off and listing plan remains uncertain, among others.

Pacific Securities released a research report on April 17, giving Zijin Mining a "buy" rating. The main reasons for the rating include: 1) The Akyem gold mine is one of the largest gold mines in Ghana and is currently operating steadily; 2) With the continuous upward movement of the gold price, the project's resource and reserve quantities have continuous mining potential; 3) The continuous increase in resource and reserve quantities lays a solid foundation for long-term development. Risk warnings: Demand may fall short of expectations; supply may be released beyond expectations; and the US Fed's tightening may exceed expectations.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)