SMM Alumina Morning Comment on June 30

Futures Market: Overnight, the most-traded alumina 2509 futures contract opened at 2,980 yuan/mt, with a high of 3,001 yuan/mt, a low of 2,973 yuan/mt, and closed at 2,989 yuan/mt, up 8 yuan/mt or 0.27%, with an open interest of 296,000 lots.

Ore: As of June 27, the SMM imported bauxite index stood at $74.21/mt, down $0.09/mt from the previous trading day; the SMM Guinea bauxite CIF average price was $74/mt, unchanged from the previous trading day; the SMM Australia low-temperature bauxite CIF average price was $70/mt, unchanged from the previous trading day; and the SMM Australia high-temperature bauxite CIF average price was $61/mt, unchanged from the previous trading day.

Industry News:

- Bauxite Port Inventory: According to SMM statistics on June 27, the total bauxite inventory at nine domestic ports was 23.35 million mt, an increase of 1.27 million mt from the previous week.

- Canyon Resources confirmed on June 26 that the development progress of its flagship Minim Martap bauxite project in Cameroon is advancing steadily. The company secured a loan of approximately $140 million from AFG Bank Cameroon and received a capital injection of AUD 15.8 million from its major shareholder, Eagle Eye Asset Holdings, through the exercise of options. The funds will be used to purchase critical equipment and sign key contracting agreements. Currently, 22 locomotives have been ordered from CRRC Ziyang Co., Ltd., with the first batch expected to be delivered in Q1 2026. Road construction and railway inland shipping facilities (IRF) will commence in July 2025. Mining and ore transportation contractors will arrive on site by the end of the year, with production scheduled to start in Q1 2026. The company expects to achieve its first shipment in H1 2026 and will update the JORC mineral resource and reserve assessment by the end of July.

- According to data on June 27, the total weekly bauxite arrivals at domestic ports were 4.8992 million mt, an increase of 698,300 mt from the previous week; the total weekly bauxite port departures from major ports in Guinea were 2.5635 million mt, a decrease of 500,300 mt from the previous week. The impact of Guinea's rainy season is expected to gradually manifest, with the average weekly port departures being 3.54 million mt in the four weeks of May and 3.32 million mt in the four weeks of June, down 220,000 mt WoW. The total weekly bauxite port departures from major ports in Australia were 1.0797 million mt, a decrease of 244,600 mt from the previous week.

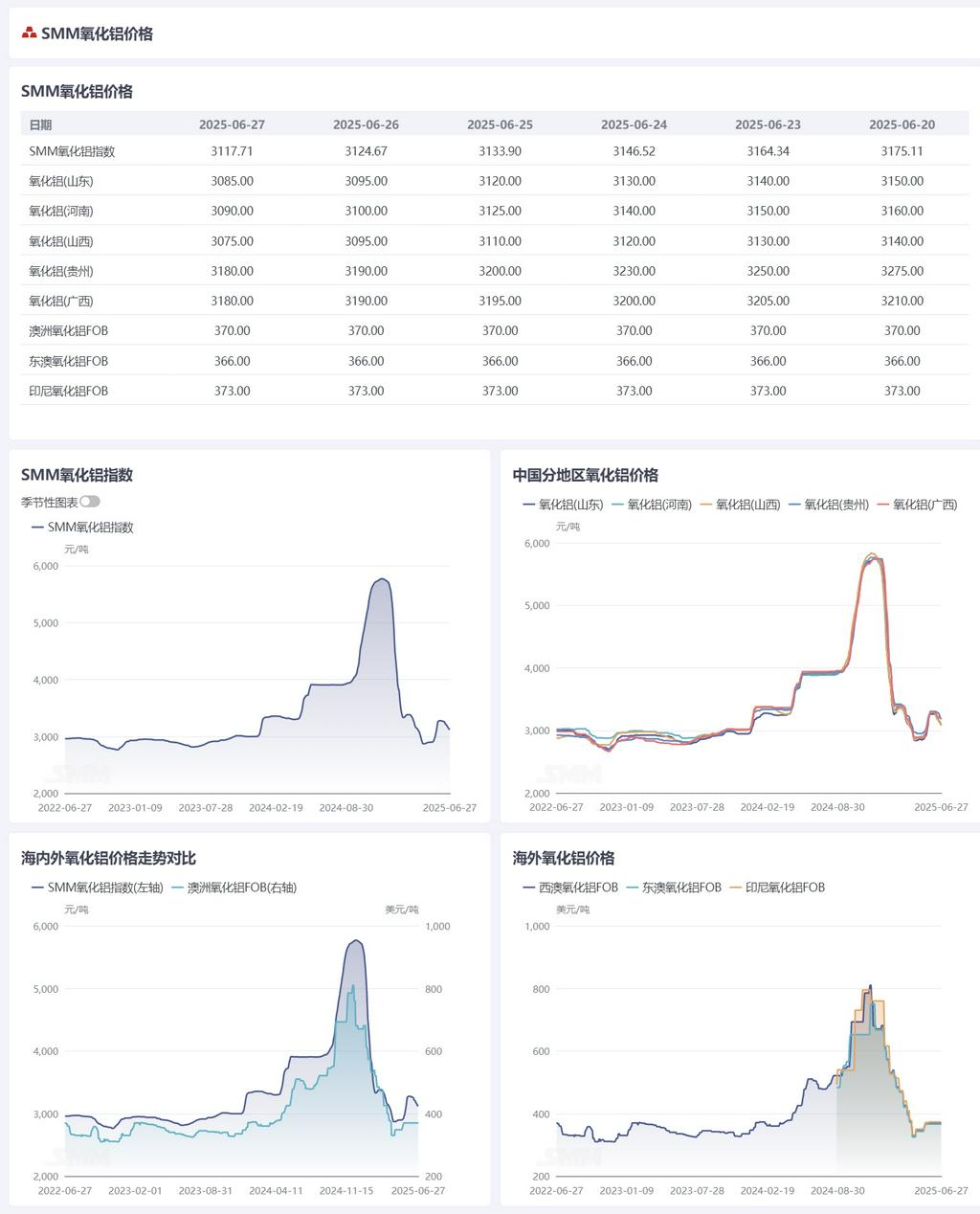

Spot-Futures Price Spread Daily Report: According to SMM data, on June 27, the SMM alumina index had a premium of 151.71 yuan/mt against the latest transaction price of the most-traded contract at 11:30 a.m.

Warrant Daily Report: On June 27, the total registered alumina warrants decreased by 3,617 mt from the previous trading day to 30,300 mt. The total registered alumina warrants in the Shandong region remained unchanged at 0 from the previous trading day, in the Henan region remained unchanged at 0 from the previous trading day, in the Guangxi region remained unchanged at 2,701 mt from the previous trading day, in the Gansu region remained unchanged at 0 from the previous trading day, and in the Xinjiang region decreased by 3,617 mt from the previous trading day to 27,600 mt.

Overseas Market: As of June 27, 2025, FOB Western Australia alumina prices stood at $370/mt, with ocean freight rates at $21.9/mt and the USD/CNY selling rate hovering around 7.19. This pricing translates to approximately 3,263 yuan/mt at domestic main ports, exceeding domestic alumina prices by 145 yuan/mt. The alumina import window remains closed.

Summary: In the short term, alumina operating capacity is expected to remain high, while spot market supply stays relatively loose, exerting downward pressure on spot alumina prices. Cost-wise, long-term contract prices for bauxite in Q3 are expected to stabilize or decline, with alumina production costs projected to remain stable with a slight decrease overall. As alumina prices continue to decline, cost support is anticipated to gradually emerge. In the near term, spot alumina prices are expected to fluctuate within a range.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should exercise caution in decision-making and shall not rely on this as a substitute for independent judgment. Any decisions made by clients are unrelated to SMM.]