SMM News on June 27: Amidst a continuous decline in the US dollar and an overall positive macro environment, the main contract of silicon metal futures continued to rise this week. On June 27, the silicon metal futures surged over 4% amid a sudden production cut by silicon enterprises in Xinjiang at the supply end. By the close of the day session, the main contract of silicon metal futures closed at 8,030 yuan/mt, up 4.02%, with an intraday high of 8,050 yuan/mt, hitting a new one-month high since May 20.

In the spot market, according to SMM spot quotes, as of June 27,oxygen-blown #553 silicon (east China)spot quotes rose to 8,200-8,400 yuan/mt, with an average price of 8,300 yuan/mt, up 150 yuan/mt from the low of 8,150 yuan/mt on June 25, representing a 1.84% increase.

》Click to view SMM silicon product spot quotes

According to SMM, on June 26, news of production cuts by large plants in Xinjiang spread in the market, with a rapid pace of reduction, cutting over 20 units more than the previous week. The daily production impact is estimated to be around 1,500-1,700 mt, and the duration of the production cuts remains uncertain. Due to the sudden news of this large-scale production cut, SMM has revised down its previous forecast for the national supply in July. Driven by this news, the silicon metal futures closed up 2.66% on June 26, and today, driven by factors such as a positive macro environment and news, the gains continued to expand.

Specifically, on the macro front, geopolitical conflicts have cooled down, while market expectations for a US Fed interest rate cut in the second half of the year have risen, coupled with market disruptions caused by rumors of a "change in leadership" at the US Fed. The US dollar index has hovered near its lowest point since March 2022, with the US dollar remaining at a low level, providing support for the non-ferrous metals industry. Domestically, today, the National Bureau of Statistics (NBS) stated that it would thoroughly implement the decisions and deployments of the Party Central Committee and the State Council, implement more proactive and effective macro policies, focus on strengthening the domestic big cycle, enhance innovation-driven development, and steadily promote high-quality industrial development, laying a solid foundation for the recovery of industrial enterprise benefits. The overall macro environment is positive.

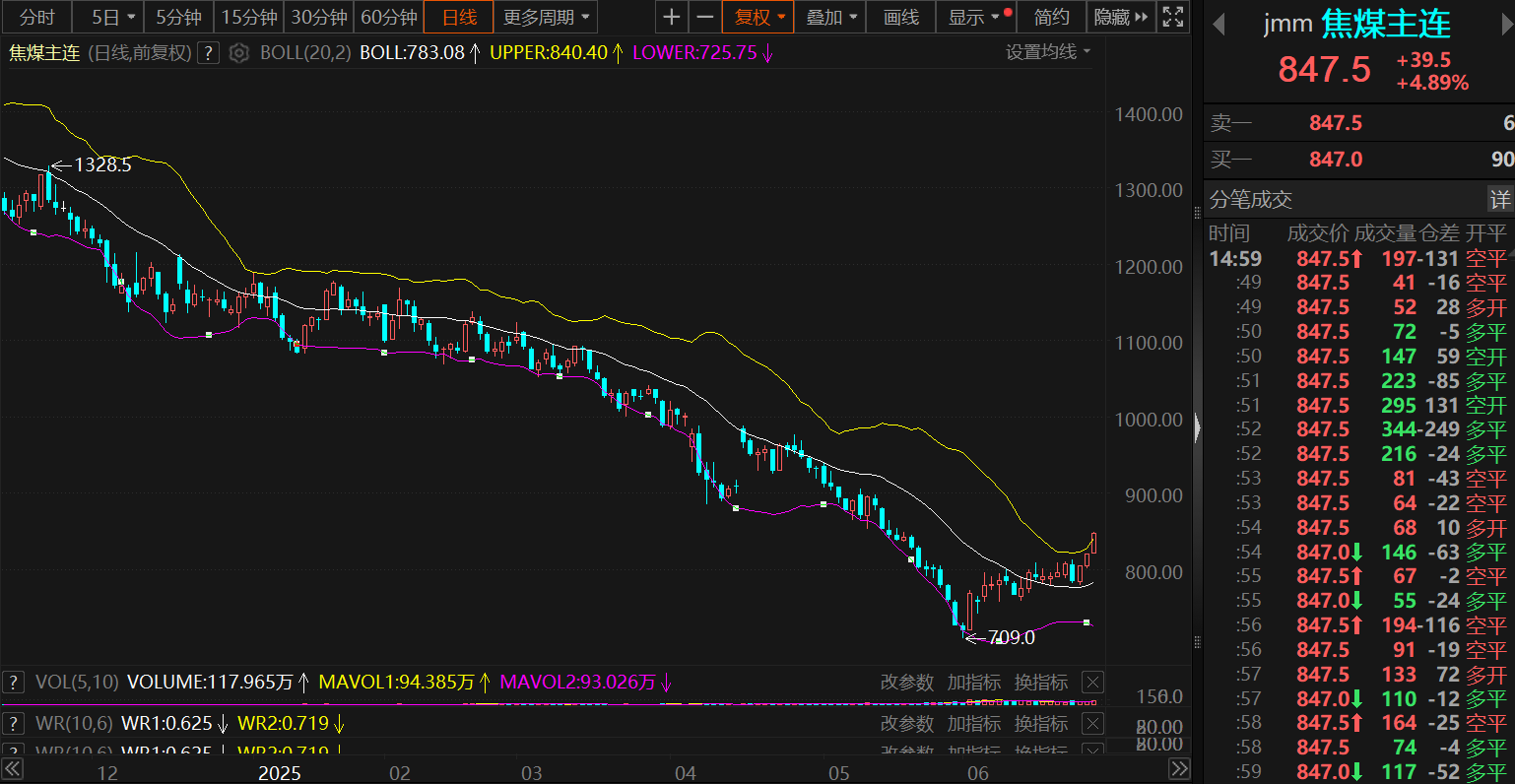

Moreover, the futures price of coking coal, a cost component for silicon metal, has also risen for three consecutive trading days, closing up 4.89% on June 27. The rise in coking coal prices may drive up electricity prices to a certain extent, providing cost support for silicon metal prices.

As for the downstream consumption end, in terms of polysilicon, according to SMM, the weekly production of polysilicon decreased slightly MoM this week, partly due to the delayed commissioning of a new capacity and partly because production resumptions have not yet yielded output. However, the polysilicon market is currently focused on the production schedule for July. There are numerous "speculations" in the market, and large plants currently have limited confirmed production directions. SMM believes that the production schedule for July remains uncertain, but overall, polysilicon enterprises are likely to increase production in July, and it is expected that the subsequent demand for silicon metal will also increase accordingly.

In contrast to polysilicon, the performance of the silicone and aluminum-silicon alloy sectors has been relatively mediocre. In the silicone sector, according to SMM, the operating rate remained largely stable this week, with DMC weekly production hovering around 49,000 mt, basically flat WoW. In the aluminum-silicon alloy sector, affected by weak demand during the off-season and cost-side pressures, the operating rate declined slightly MoM this week.

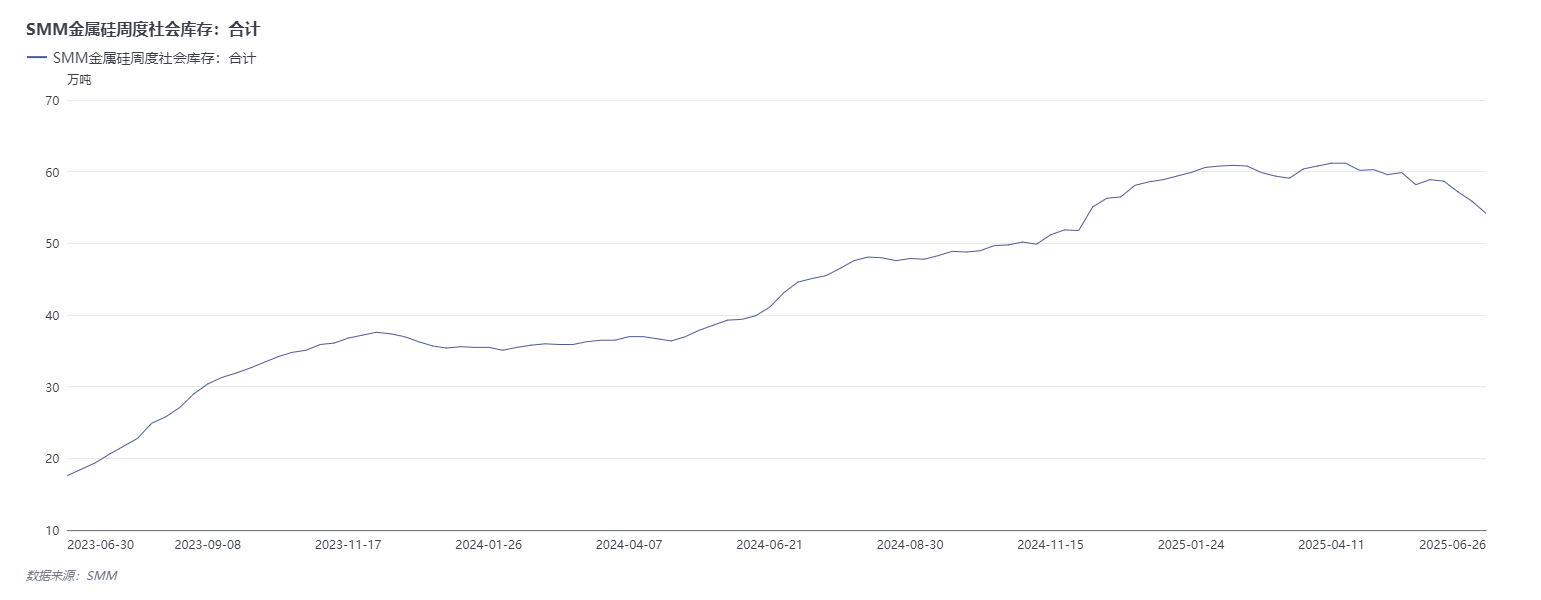

In terms of inventory, according to SMM data, domestic silicon metal inventory has shown a destocking trend since June 5. As of May 26, SMM's weekly silicon metal inventory totaled 542,000 mt, a destocking of 42,000 mt from June 5.

Therefore, overall, factors such as a warm macro atmosphere, sudden news of production cuts by silicon enterprises in Xinjiang, expectations for production increase in polysilicon, and support from the cost side have jointly driven the continuous rise in silicon metal futures prices in recent trading days. Looking ahead, the actual timing of production cuts by large plants in Xinjiang on the supply side remains uncertain, and the recent supply-side performance has fallen short of expectations. On the demand side, there may be expectations for production increase in polysilicon in July, with supply decreasing and demand increasing providing support for short-term silicon prices. However, currently, the inventory of the silicon metal industry remains at a high level, and overcapacity still exists. Therefore, continuous attention needs to be paid to the specific performance of the supply and demand sides in the future.

Institutional Commentary

Guotai Junan Futures stated that production cut news has disrupted the futures market, and short-term attention should be paid to the upside potential. Market news indicates that upstream factories have reduced production, coupled with expectations for production resumptions in the downstream polysilicon sector, which has lifted the futures market from the bottom. However, after the futures market rose, it could also be seen that factories in Xinjiang gradually began to hedge. If the market rises further, hedging positions from factories in south-west China will also start to appear, which will pose a limit to the upside of the futures market. From a supply and demand perspective, although the short-term production resumption in polysilicon brings expectations for improved demand, due to the high inventory pressure on silicon metal, the slope of warrant liquidation has slowed down, weakening the driving force for further upside in the futures market. However, in the short term, due to the continuous rise in coking coal prices, silicon metal may exhibit resistance to decline, with significant amplification in futures market volatility. Subsequent attention should be paid to the registration information of silicon metal futures warrants. If warrants start to be registered in large quantities, short positions can be established at high levels.

Donghai Futures stated that silicon metal is holding up well, driven by news of production cuts by large plants in Xinjiang and the rise in coking coal prices. Both supply and demand are weak, with the fundamentals remaining loose. Last week, the weekly production of silicon metal was 70,434 mt, up 2.5% MoM, with a total of 235 furnaces in operation. Sichuan increased by 4, Xinjiang increased by 4, Yunnan decreased by 2, and Gansu decreased by 1. The operating rate during the rainy season in south-west China has risen, but it is significantly lower than the same period in previous years. In terms of price, it is driven by the rebound in coal prices due to the conduction of raw material silicon coal, but the rebound is relatively weak. Operationally, it is recommended to wait and see in the short term and go short in the medium term.