SMM June 27 News:

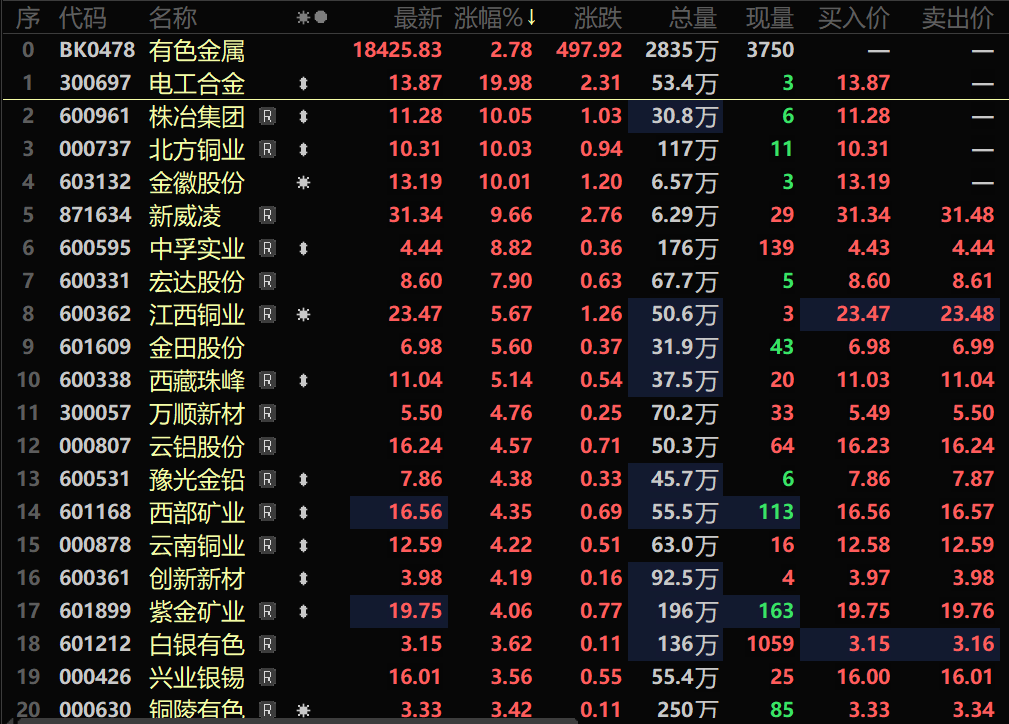

Affected by factors such as the intensification of domestic policies aimed at stabilizing growth, poor US economic data, market concerns over the independence of the US Fed policy leading to the US dollar index hovering near a three-year-plus low, fundamental support from tightening copper raw material supply, a rebound in market risk appetite due to the easing of geopolitical conflicts, and the influx of some market funds, the prices of non-ferrous metals such as copper, tin, and zinc have risen, driving the non-ferrous metals sector higher. As of 13:12 on the 27th, SHFE copper, SHFE aluminum, SHFE zinc, SHFE tin, and SHFE nickel all showed upward trends. It is worth mentioning that LME copper hit a new high since March 27th at $9,917/mt during the trading session on the 27th. Along with the rise in non-ferrous metal futures prices, domestic stocks in the non-ferrous metals sector also strengthened collectively. As of 13:23 on the 27th, the non-ferrous metals sector rose by 2.78%. Among individual stocks, Diangong Alloy, Zhuzhou Smelter Group, North Copper, and Jinhui Stock all hit their daily limits. Xinweiling, Zhongfu Industrial, Jiangxi Copper Corporation, and Jintian Stock were among the top gainers.

Copper

》Click to view SMM Metal Industry Chain Database

In terms of spot copper: Affected by the US dollar index falling to a new low since March 2022 and the policy uncertainty surrounding the US's proposed tariff hike on imported copper, copper prices continued to rise. According to SMM quotes, the average price of SMM #1 copper cathode on June 27th was 80,125 yuan/mt, up 1.5% from the previous trading day, hitting a new high in nearly three months. According to SMM data, as of Thursday, June 26th, SMM copper inventories in major regions across the country increased slightly by 500 mt to 130,100 mt compared to Monday, and decreased by 15,800 mt compared to Thursday last week. Currently, inventories are only 10,000 mt higher than the previous low, and there is a possibility of hitting new lows in the future. According to SMM, due to smelters' export actions leading to reduced shipments, coupled with limited supplementary imports of copper, copper inventories in east China have declined. Although consumption increased in Guangdong this week, the increase in supply was even greater. As the year-end approached, some suppliers had a need to liquidate their holdings, leading to an increase in the amount of copper shipped to warehouses, which caused the total inventories in Guangdong to rise. In contrast, inventories in the southwest and north China regions increased due to poor consumption. It is expected that next week, both imported and domestically produced copper arrivals will be relatively low, and total supply will be less than last week. In terms of downstream consumption, with year-end settlements completed, consumption is expected to be better next week than this week. Therefore, SMM believes that next week will see a situation of reduced supply and increased demand, and weekly inventories may continue to decline, which will further strengthen the support of inventories for copper prices. In the short term, the market still needs to pay attention to the competition between the US dollar trend and tariff policies. If the US tariff policy is implemented or the US Fed's interest rate cut exceeds expectations, copper prices may continue to rise. In the medium and long term, attention still needs to be paid to the impact of fundamental factors such as the release pace of domestic secondary copper capacity and disruptions in the global copper ore supply side.

Tin

》Subscribe to view SMM metal spot historical prices

Tin spot market: The US Q1 GDP final reading was revised down to a 0.5% contraction, while initial jobless claims came in below expectations. Market expectations for US Fed interest rate cuts strengthened, weakening the US dollar index and boosting dollar-denominated commodity prices. Domestically, growth-stabilizing policies were intensified as the central bank and six other departments launched 19 consumption-boosting measures, raising metal consumption expectations and rebounding risk appetite. Fundamentals side: **Tight tin ore supply**: Myanmar's Wa region production resumptions lagged (less than 50% of tunnel repairs completed), compounded by Thailand restricting Myanmar tin ore transit shipments. China's tin ore imports continued to decline in June. **SHFE tin may hover at highs in the short term**. Risks of faster-than-expected Myanmar production resumptions and weaker-than-expected consumer electronics demand warrant caution.

Institutional Viewpoints

[Goldman Sachs: Tariffs Trigger Supply Risks, Raise 2025 H2 Copper Price Forecast]On June 25 (Wednesday), investment bank Goldman Sachs stated in a report that copper prices will average $9,890/mt in H2 2025 due to US tariffs raising concerns about global supply tightness. Goldman predicts copper prices will peak at $10,050/mt in August as tariff threats reduce copper inventories outside the US. The bank expects prices to retreat to $9,700/mt by December. Goldman emphasizes the market has not yet priced in potential 25% US copper import tariffs, recommending a trading strategy exploiting US-UK copper market price spreads. For 2026, Goldman lowered its copper price forecast from $10,170/mt to $10,000/mt, with prices projected to reach $10,350/mt by December 2026.》Click for details

Zheshang Securities believes copper prices have strong support, as full-year supply growth has slowed significantly due to Chile's massive power outages, declining mine grades, and Indonesian mine maintenance. On the demand side, power investment mega-cycles, energy transition dynamics, and emerging market growth are expected to drive steady expansion, confirming a tightening supply-demand scenario.