SMM News on June 26:

Metal Market:

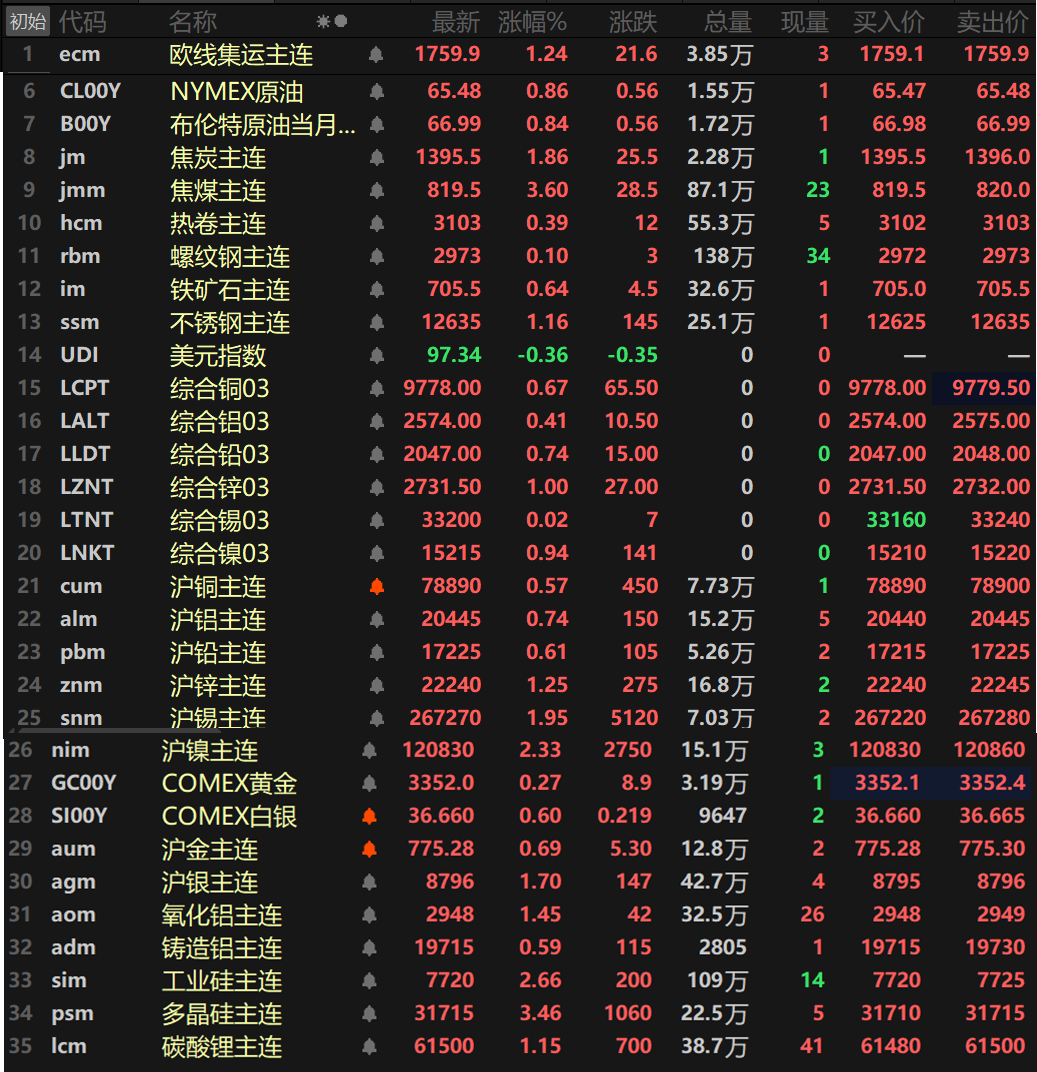

As of the daytime close, domestic market base metals collectively rose, with SHFE nickel leading the gains at 2.33%. SHFE tin and SHFE zinc both rose over 1%, with SHFE tin up 1.95% and SHFE zinc up 1.25%. The remaining metals all rose less than 1%. The main alumina contract rose 1.45%, recording a four-day winning streak. The main aluminum casting contract rose 0.59%.

In addition, the main lithium carbonate contract rose 1.15%. After hitting record lows in the previous trading sessions, the main polysilicon contract staged a strong rebound, closing up 3.46%. Silicon metal rose 2.66%, also recording a four-day winning streak. The European Containerized Freight Index rose 1.24% to 1759.9.

The ferrous metals series also collectively rose, with stainless steel up 1.16% and the remaining metals all rising less than 1%. In the coking coal and coke sector, coking coal rose 3.6% and coke rose 1.86%.

In the overseas market, as of 15:03, overseas market base metals generally rose, with LME zinc up 1% and the remaining metals fluctuating within a 1% gain range.

In the precious metals sector, as of 15:03, COMEX gold rose 0.27% and COMEX silver rose 0.6%. Domestically, SHFE gold rose 0.69% and SHFE silver rose 1.7%.

Market conditions as of 15:03 today

》Click to view SMM Market Dashboard

Macro Front

Domestic Aspect:

[NDRC: Third Batch of Trade-in Funds for Consumer Goods to Be Disbursed in July] Li Chao, Deputy Director of the Policy Research Office of the National Development and Reform Commission (NDRC), stated at the NDRC's June press conference held on the morning of the 26th that the third batch of trade-in funds for consumer goods this year will be disbursed in July. Meanwhile, the NDRC will coordinate with relevant parties to adhere to the principles of greater continuity and balance, formulating a plan for the use of national subsidy funds that is implemented on a monthly and weekly basis across different fields, ensuring the orderly implementation of the trade-in policy for consumer goods throughout the year. Li Chao introduced that the NDRC, in conjunction with relevant departments, recently issued an action plan to strengthen and expand work-relief programs to promote employment and income growth for key groups. Through this incremental policy, support for vulnerable groups will be further enhanced. Since November last year, the NDRC, in collaboration with the Ministry of Finance, has disbursed 16.5 billion yuan in central special investment for work-relief programs in 2025, supporting over 3,900 local work-relief projects and expected to address the employment and income growth needs of 380,000 vulnerable individuals. Building on this foundation, the current action plan proposes to newly arrange a batch of central budgetary investment projects to support regions with a high concentration of key groups. 》Click to view details

[National Development and Reform Commission (NDRC): This Year's Power Supply and Demand Situation During Peak Summer Load Period is Better Than Last Year, Overall Supply-Demand Balance is Generally Guaranteed]Li Chao, Deputy Director of the Policy Research Office of the National Development and Reform Commission (NDRC), stated that summer is the peak period for electricity load throughout the year, and the key to energy supply guarantee lies in electricity. It is expected that during this year's peak summer load period, the national peak electricity load will increase by approximately 100 million kW YoY. In response to this situation, the NDRC has collaborated with relevant parties to focus on power supply guarantee, adopting a series of measures and making early arrangements, providing strong support for power supply guarantee during this year's peak summer load period. Li Chao indicated that, based on the current situation, this year's power supply and demand situation during the peak summer load period is better than last year, and the overall supply-demand balance is generally guaranteed.

US dollar aspect:

As of 15:03, the US dollar index fell by 0.36% to 97.34, with the intraday low reaching 97.23, marking a new low since March 2022. In recent days, several US Fed officials have adopted dovish tones, and expectations for a US Fed interest rate cut in September have intensified. Fed Chairman Powell reiterated on the second day of his testimony before the US Congress on Wednesday that he expects the Trump administration's tariffs to push up inflation, and the Fed should maintain interest rates unchanged. Powell stated on Tuesday that if it weren't for the tariffs, the Fed might have continued to cut interest rates. Fed Vice Chair Bowman and Governor Waller have both recently indicated that the Fed should cut interest rates as soon as possible, increasing the likelihood of further rate cuts. Federal funds futures traders expect a 62 basis point rate cut before the end of the year, up from approximately 46 basis points expected before Waller's remarks last Friday. Traders have fully priced in the expectation of the first rate cut in September.

The market is awaiting the release of US Gross Domestic Product (GDP) data later in the day and the US Personal Consumption Expenditures (PCE) Price Index on Friday. The market currently expects the Fed to cut interest rates by 64 basis points before the end of the year.

Macro aspect:

Today, data such as the final annualized quarterly rate of real GDP for the US Q1, the final quarterly rate of the GDP price index for the US Q1, the final annualized quarterly rate of the core PCE price index for the US Q1, the final annualized quarterly rate of consumer spending for the US Q1, the final seasonally adjusted quarterly rate of the implicit GDP deflator for the US Q1, the preliminary monthly rate of durable goods orders for the US in May, the initial jobless claims for the week ending June 21 in the US, the preliminary monthly rate of wholesale inventories for the US in May, the seasonally adjusted monthly rate of the pending home sales index for the US in May, the CBI retail sales balance for the UK in June, and the Gfk consumer confidence index for Germany in July will be released. Additionally, Bailey, the Governor of the Bank of England, will deliver a keynote speech at the British Chambers of Commerce Global Annual Conference.

Crude oil:

As of 15:03, oil prices in both markets rose simultaneously, with US crude oil up 0.86% and Brent crude oil up 0.84%. The decline in US crude oil inventories was greater than expected, indicating strong demand, while investors remained cautious about the stability of geopolitical situations. Due to the boost in fuel demand during the traditional peak consumption season, coupled with a slowdown in production growth and a decline in net imports, US commercial crude oil inventories have fallen for five consecutive weeks. As of the week ending June 20, total US crude oil inventories, including strategic reserves, stood at 817.632 million barrels, down 5.6 million barrels from the previous week; US commercial crude oil inventories were at 415.106 million barrels, down 5.84 million barrels from the previous week; total US gasoline inventories were at 227.938 million barrels, down 2.08 million barrels from the previous week; and distillate fuel oil inventories were at 105.332 million barrels, down 4.07 million barrels from the previous week. Historically, US crude oil inventories have declined during the peak travel season, with the largest declines occurring from July to September, when end-user demand for oil products is strong, driving a significant destocking trend in crude oil.

Meanwhile, market focus is now shifting to OPEC+'s production levels. OPEC+ began gradually increasing oil production in April this year and further intensified production increases in May, raising oil production by 411,000 barrels per day, a significant increase from the 210,000 barrels per day increase in April. Moreover, OPEC+ has hinted that it may continue to maintain this substantial production increase in August and September this year, with at least a 411,000 barrels per day increase. Early this morning, Russia stated that it is willing to support further production increases at the next OPEC+ meeting if deemed necessary by OPEC+. If approved by the government, the Russian oil industry is ready to increase production again in August. At this rate of production increase, the originally planned total production increase target of 2.2 million barrels per day may be achieved ahead of schedule, by October this year. (Wenhua Comprehensive)

SMM Daily Review