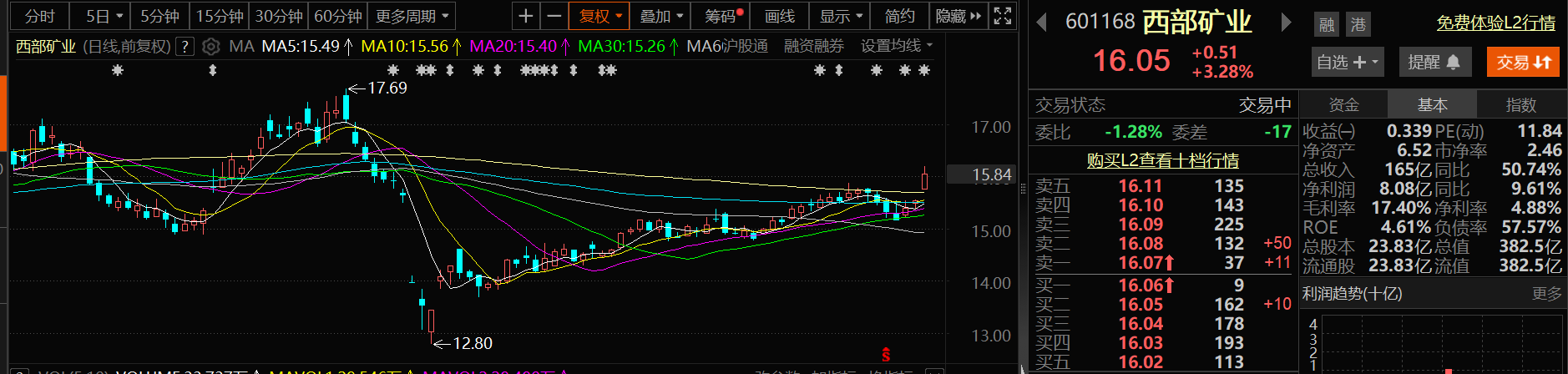

Western Mining Co., Ltd.'s share price saw a significant increase on June 26. As of 11:03 a.m. on June 26, Western Mining Co., Ltd. rose by 3.28%, trading at 16.05 yuan per share.

On the news front, Western Mining Co., Ltd. announced on the evening of June 25 that on June 23, its controlling subsidiary, Tibet Yulong Copper Industry Co., Ltd., received the "Approval Reply from the Development and Reform Commission of Tibet Autonomous Region on the Phase III Project of Yulong Copper Mine of Tibet Yulong Copper Industry Co., Ltd." (Zang Fagai Chan Ye [2025] No. 362). To implement the work deployment of the State Council on ensuring the security of strategic mineral resources and promote the transformation of resource advantages into economic development advantages,the Phase III Project of Yulong Copper Mine was approved, with the copper mine's production scale increasing from 19.89 million mt/year to 30 million mt/year.

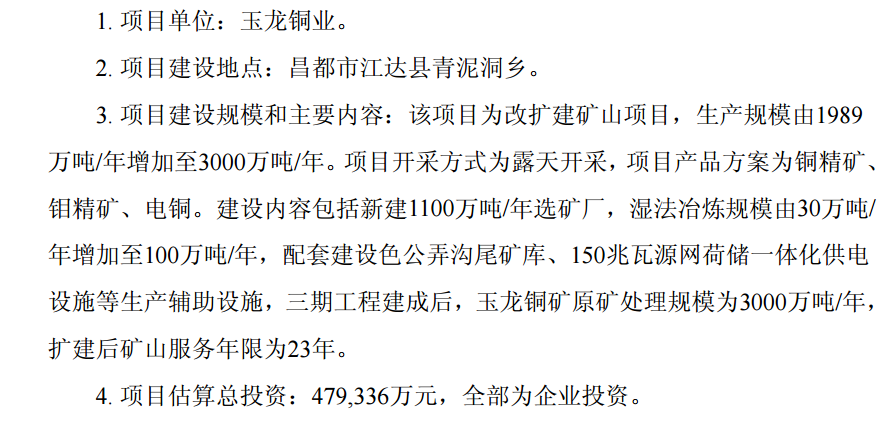

The main content of the approval announced by Western Mining Co., Ltd. is as follows:

This project is a mine expansion project, with the production scale increasing from 19.89 million mt/year to 30 million mt/year. The mining method is open-pit mining, and the project's product plan includes copper concentrates, molybdenum concentrates, and electrolytic copper. The construction includes a new 11 million mt/year beneficiation plant, an expansion of the hydrometallurgy scale from 300,000 mt/year to 1 million mt/year, and the construction of supporting production auxiliary facilities such as the Segonglonggou tailings pond and a 150 MW integrated generation-grid-load-storage power supply facility. After the completion of the Phase III project, the raw ore processing scale of Yulong Copper Mine will be 30 million mt/year, and the mine's service life after expansion will be 23 years. The estimated total investment of the project is 4,793.36 million yuan, all of which is enterprise investment.

Regarding the impact on the company, Western Mining Co., Ltd. stated that Yulong Copper Mine, as the company's main copper mine, with its high-grade ore resources and advanced equipment level, has become the company's largest source of revenue and profit.As of the end of 2024, Yulong Copper Mine had 830 million tons of copper ore resources, with an average copper grade of 0.6%. In 2024, it produced 159,000 mt (metal content) of copper. With the completion and operation of the Phase III project of Yulong Copper Mine, the production scale is expected to reach 30 million mt/year, and the copper metal content will reach 180,000-200,000 mt/year. The overall scale of the company's mineral copper will further increase,which will continuously enhance the company's profitability, consolidate and strengthen the company's market competitiveness in the non-ferrous metal mineral sector, enhance investor confidence, and lay a solid foundation for the company's long-term development.

Western Mining Co., Ltd. also provided a risk warning in the announcement: The construction of the Phase III project of Yulong Copper Mine still requires obtaining relevant procedures from other departments, and the completion time is uncertain. Additionally, the project is located in a high-altitude and hypoxic area with a harsh natural geographical environment, and there may be risks that the project construction may not meet expectations. Forward-looking statements involving future production plans do not constitute substantive commitments from the company to investors. Investors are advised to pay attention to investment risks.

The first quarter report previously released by Western Mining Co., Ltd. showed that from January to March 2025, the company achieved an operating revenue of 16.542 billion yuan, up 50.74% YoY, a total profit of 1.795 billion yuan, and a net profit attributable to shareholders of the parent company of 808 million yuan, up 9.61% YoY. The production of copper ore increased by 14.35% YoY and 5.81% MoM, zinc ore production increased by 18.17% YoY and 6.95% MoM, and lead ore production increased by 38.38% YoY and 32.76% MoM. Details are as follows:

Regarding the reasons for the increase in operating revenue, Western Mining Co., Ltd. stated that the production and sales volumes of smelted copper, smelted lead, and gold ingots increased compared to the same period last year.

The 2024 annual report previously released by Western Mining Co., Ltd. showed that the company achieved an operating revenue of 50.026 billion yuan in 2024, up 17% YoY, a total profit of 5.992 billion yuan, up 27% YoY, and a net profit of 5.294 billion yuan, including a net profit attributable to shareholders of the parent company of 2.932 billion yuan, up 5% YoY. The main reasons were the increase in the prices of non-ferrous metals and the increase in the production and sales volumes of copper ore compared to the same period last year.

The 2024 annual report of Western Mining Co., Ltd. showed that in 2024, the company's affiliated mine units operated at highs according to the annual production and operation plan, achieving significant increases in the production of copper ore, molybdenum ore, and smelted copper, ranking the company among the top domestic super-large mine enterprises. The annual production of copper ore was 177,543 mt (metal content), up 35% YoY, including 159,084 mt (metal content) produced by Yulong Copper, up 39.10% YoY, 4,009 mt (metal content) of molybdenum ore, up 18% YoY, 1,376,891 mt of iron ore concentrates, up 15% YoY, and 130,829 kg of silver in concentrates, up 6% YoY. The smelting units comprehensively optimized and upgraded the smelting system, achieving a production of 263,771 mt of smelted copper, including 178,499 mt produced by Qinghai Copper and 80,617 mt produced by Western Copper Semis. The salt lake chemical enterprises actively participated in the development and utilization of salt lake resources, producing 114,834 mt of high-purity magnesium hydroxide and 39,022 mt of high-purity magnesium oxide.

The main products planned to be produced by Western Mining Co., Ltd. in 2025, as announced in its 2024 annual report, are: 168,208 mt (metal content) of copper ore, 124,581 mt (metal content) of zinc ore, 65,672 mt (metal content) of lead ore, 4,005 mt (metal content) of molybdenum ore, 1,565 mt of nickel ore, 1,457,679 mt of iron ore concentrates, 183 kg of gold in concentrates, 132.92 mt of silver in concentrates, 354,003 mt of smelted copper, 240,008 mt of smelted lead, and 200,000 mt of smelted zinc. The company plans to achieve an operating revenue of 55 billion yuan and a total profit of 5 billion yuan in 2025.

On May 14, Pacific Securities issued a research report, giving Western Mining Co., Ltd. a "buy" rating. The key reasons for the rating include: 1) In Q1 2025, the production of major products increased YoY, with ore production achieving a good completion rate; 2) The company is actively advancing reserve augmentation and expansion construction, with the Yulong Phase III project expected to boost copper ore production; 3) Copper, zinc, and lead prices increased YoY, with a relatively small impact from the decline in smelting-side processing fees. Risk warnings: Risk of volatile prices, unexpected cost increases on the cost side, and production falling short of expectations.

China Galaxy Securities previously released a research report commenting on Western Mining Co., Ltd.'s Q1 results, noting that the company's copper production and prices both increased, the impact on the smelting side was controllable, and asset impairments were eliminated, leading to a significant MoM improvement in performance in Q1 2025: 1) Mine side: In Q1 2025, the company's production of copper ore, zinc ore, lead ore, molybdenum ore, and iron ore concentrates was 4.4, 3, 1.7, 0.1, and 338,000 mt respectively, representing YoY increases of +14.4%, +18.2%, +38.4%, +43.6%, and +14.7%, and MoM increases of +5.8%, +7%, +32.8%, +20.4%, and -13.5%, achieving 26%, 24%, 25%, 31%, and 23% of the planned targets. The average domestic prices of copper, zinc, and lead in Q1 2025 were 77,000, 24,000, and 17,000 yuan/mt respectively, representing YoY increases of +11.5%, +14.5%, and +5.8%, and MoM increases of +2.5%, -5.9%, and +1.0%. 2) Smelting side: In Q1 2025, the company's production of smelted copper (including SX-EW copper), smelted zinc, and smelted lead was 90,000, 34,000, and 44,000 mt respectively, representing YoY increases of +54.8%, +19.2%, and +1752%, and MoM increases of +11.6%, +2.5%, and +30.6%. The significant increase in smelted lead production was mainly due to the infrastructure period of rare and precious metals in 2024, during which smelted lead production was suspended from February to September. Despite the continued pressure on copper smelting processing fees, the company's overall impact on the smelting side was controllable, as most of its raw material purchases were domestic ore and anode plates, and the self-sufficiency rate of Yulong Copper Mine for the company's copper smelting products was relatively high. Benefiting from the increase in both copper production and prices at the mine side and the improvement in smelting-side profitability, the company's gross profit increased by 67% MoM to 2.88 billion yuan in Q1 2025. Key projects are advancing in an orderly manner, with incremental production expected from Yulong Phase III: In the copper sector, with the completion and effectiveness of the renovation and expansion projects of the first and second beneficiation plants at Yulong Copper Mine, the copper ore processing capacity has been increased to 22.8 million mt/year. In 2024, the production of copper and molybdenum ore reached 163,000 mt. Currently, Yulong Copper is in the process of handling the preliminary procedures for a 30 million mt capacity expansion project. In the lead-zinc sector, the lead-zinc system at the Huogeqi Copper Polymetallic Mine successfully completed its upgrade and transformation in 2024 and commenced production as scheduled, with a lead-zinc ore processing capacity of 1.5 million mt/year and an annual production of lead and zinc ore exceeding 40,000 mt. In the iron sector, the Shuangli No. 2 Iron Mine is advancing the renovation and expansion project from open-pit to underground mining, with a designed annual mining and beneficiation capacity of 3.4 million mt/year. The company's most-traded mine, the Yulong Copper Mine, is expected to commence production in its future Phase III expansion project, with copper production from ore likely to experience a simultaneous increase in both volume and price, driving the company's performance growth. Risk warnings: 1) The risk of a significant decline in copper prices; 2) The risk of global economic recovery falling short of expectations; 3) The risk of the US Fed's interest rate cut falling short of expectations; 4) The risk of overseas geopolitical changes; 5) The risk of the impact of tariff hikes between China and the US exceeding expectations.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)