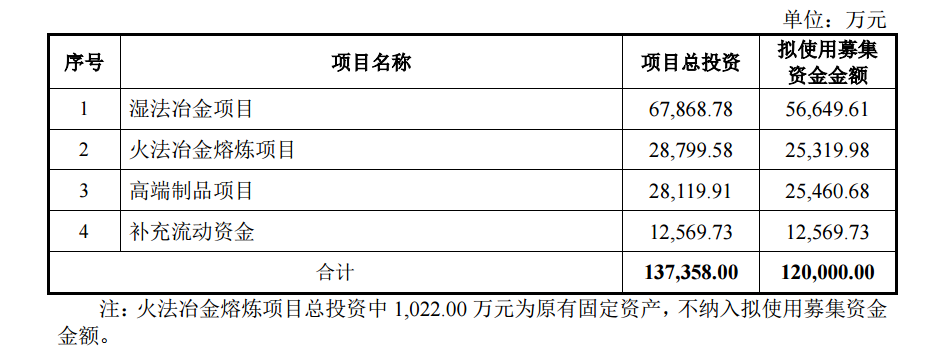

The private placement plan announced by Dongfang Tantalum Industry on June 24th indicates that the company intends to issue no more than 151 million shares to no more than 35 specific investors, including China Nonferrous Metals Mining (Group) Co., Ltd., the actual controller, and CNMC (Ningxia) Dongfang Group Co., Ltd., the controlling shareholder, raising a total of no more than 1.2 billion yuan. Among them, China Nonferrous Metals Mining (Group) Co., Ltd., the actual controller, will subscribe for 105 million yuan, and CNMC (Ningxia) Dongfang Group Co., Ltd., the controlling shareholder, will subscribe for 480 million yuan. The total amount of funds raised from this private placement of A-shares will not exceed 1.2 billion yuan. After deducting the issuance expenses, the funds will be invested in three construction projects and used to supplement working capital. The specific situation is as follows:

Before the raised funds from this issuance are in place, the company will use self-raised funds to make initial investments in the projects funded by the raised funds according to market conditions, and replace these investments with the raised funds after they are in place. If the net amount of the actually raised funds is lower than the planned investment amount for the projects funded by the raised funds, the company's shareholders' meeting will authorize the company's board of directors and its authorized personnel to adjust and ultimately decide on the priority order of the investment of the raised funds and the specific investment amounts for each project, etc., based on the actual net amount of the raised funds and the urgency of the projects. Any shortage of raised funds will be covered by the company's self-raised funds.

Dongfang Tantalum Industry has announced an analysis of the necessity of the projects funded by the raised funds:

(1) It is conducive to practicing the domestic large-scale circulation and ensuring the security of the national industry chain

The Fifth Plenary Session of the 19th Central Committee of the Communist Party of China clearly proposed to accelerate the construction of a new development pattern with the domestic large-scale circulation as the mainstay and the mutual promotion of domestic and international dual circulations. The economic cycle driven by domestic demand is becoming the core engine of economic growth. The company's products have a significant impact on the core competitiveness of the country in technology, national defense industry, and other fields. The products such as K2TaF7 and niobium oxide produced by the hydrometallurgy project are important basic raw materials for subsequent pyrometallurgy and product production. The products from the pyrometallurgy smelting project and the high-end product project are supplied to key industries such as high-temperature alloys, semiconductors, high-energy physics, national defense industry, and aerospace. By implementing the projects funded by the raised funds, the company can achieve the self-supply of key materials in the above-mentioned industries, solve the technical bottlenecks in related fields in China, reduce dependence on foreign imports, and thus ensure national security.

(2) It is conducive to optimizing the product structure and realizing the company's industrial upgrading and development

In recent years, the tantalum-niobium industry has undergone profound changes, and the company urgently needs to optimize its product structure and increase investment in new demand areas. Currently, the production equipment capacity of the hydrometallurgy, pyrometallurgy, and product manufacturing branches cannot meet the growing downstream demand. Therefore, it is urgent to promote new construction and renovation projects. It is expected that after the completion of the projects, the company will establish a strategic layout of a "three-tier product echelon": ensuring the security of the supply chain with primary raw materials such as K2TaF7, tantalum oxide, and niobium oxide; building competitive advantages centered around products like tantalum/niobium smelting, semiconductor targets, and superconducting niobium materials; and cultivating new tantalum-niobium compound products, superconducting wires, large-sized tubes, etc., as future growth points, while consolidating the market position of traditional tantalum-niobium and alloy products such as chemical corrosion resistance and capacitors. Through this systematic layout, the company will achieve a full-chain upgrade from raw material security to traditional product security, and then to breakthroughs in high-end products.

(3) Improving the industry chain, filling capacity gaps, and continuously enhancing competitive strength

Among the three fundraising projects this time, K2TaF7 and niobium pentoxide from the hydrometallurgy project are important basic raw materials for subsequent pyrometallurgy and product manufacturing; the smelted tantalum and niobium from the pyrometallurgy smelting project are important additives for high-temperature alloy materials and important basic raw materials for tantalum-niobium products in the high-end product project. With the rapid development of strategic emerging industries such as high-temperature alloys, semiconductors, high-energy physics, defense industry, and aerospace, market demand will exhibit a "bottom-up" transmission effect, driving the collaborative development of the "products-pyrometallurgy-hydrometallurgy" entire industry chain of Ningxia Orient Tantalum Industry Co., Ltd. The company's tantalum-niobium hydrometallurgy branch has been in operation for 27 years since its commissioning in 1998. With urban development, the existing hydrometallurgy production line is relatively close to the urban area, and due to limitations in early safety, environmental protection technologies, and facilities, the existing production line cannot meet the requirements for expansion or new construction at the original site in terms of wastewater, waste gas, and waste residue treatment. The construction content of this hydrometallurgy project is to build a new hydrometallurgy production line to address the issues of outdated equipment and insufficient capacity. The substantial demand for high-temperature alloy materials has led to a severe shortage in the production capacity of the pyrometallurgy production line. The production line for the high-end product project is a co-line production for multiple varieties and grades, which cannot meet the rapidly growing product requirements. At the same time, it lacks dual backups for key equipment, making it unable to meet semiconductor supply requirements. In summary, by increasing investment in the construction of these fundraising projects, it will help quickly fill the product capacity gaps in various key links, further enhance equipment and facility levels, optimize existing production processes, improve product quality and production efficiency, and achieve the effect of supplementing and strengthening the existing entire industry chain, activating the company's competitive advantages in the entire industry chain.

(4) Increasing high-value-added products to support the company's performance growth

Some of the products involved in this project have the characteristic of high added value. With the development of downstream industries such as semiconductor targets, superconducting niobium, defense industry, and aerospace, the market demand for these products has steadily increased. After the implementation of the project, the company will be able to expand the production scale of high value-added products, effectively improve sales revenue and profit levels, significantly enhance the company's profitability, and create greater value for shareholders.

China National Nuclear Corporation (CNNC) Orient Tantalum Industry Co., Ltd. also introduced the basic situation of the construction planning for the projects funded by the raised capital: (1) Tantalum-Niobium Hydrometallurgy Digital Factory Construction Project ① Basic Project Information This project will be implemented in the Shizuishan Economic and Technological Development Zone, Ningxia Hui Autonomous Region. It plans to build new production lines for K2TaF7 (1,100 tons/year), niobium pentoxide (1,700 tons/year), high-purity niobium pentoxide (150 tons/year), high-purity tantalum pentoxide (50 tons/year), tantalum-niobium compounds (209.5 tons/year), and by-product tin concentrates (90 tons/year). The project construction mainly includes the construction of new main production plants and auxiliary production plants, as well as the purchase of supporting process equipment and auxiliary equipment. The total investment for this project is 678.6878 million yuan, with a construction period of 27 months. The project construction entity is CNNC Orient Tantalum Industry Co., Ltd. (2) Tantalum-Niobium Pyrometallurgy Smelting Product Production Line Renovation Project ① Basic Project Information This project will be implemented in Dawukou District, Shizuishan City, Ningxia Hui Autonomous Region. The project construction includes the capacity expansion and renovation of the existing smelting and carbon reduction production lines, as well as the supporting construction of power supply, water supply, gas supply, heating, and living auxiliary facilities, material procurement, and equipment installation. It is expected that after the project is completed and reaches full production, there will be an additional annual production capacity of 860 tons of smelted niobium, 80 tons of smelted tantalum, 74 tons of niobium and niobium alloy bars, and 240 tons of tantalum and tantalum alloy bars (rods). Among these, niobium and niobium alloy bars, as well as tantalum and tantalum alloy bars (rods), are intermediate products used in the pyrometallurgy production line process and do not generate economic value through external sales. The total investment for this project is 287.9958 million yuan, with a construction period of 28 months. The project construction entity is CNNC Orient Tantalum Industry Co., Ltd. (3) Tantalum-Niobium High-End Products Production Line Construction Project ① Basic Project Information This project will be implemented in Dawukou District, Shizuishan City, Ningxia Hui Autonomous Region. The project construction includes the arrangement of main equipment, plant renovation, supporting facility construction, equipment renovation and procurement, relocation, and installation within the third span on the west side of the existing products workshop. It is expected that after the project is completed and reaches full production, the capacity of tantalum-niobium plate and strip products will increase by 145 tons/year. The total investment for this project is 281.1991 million yuan, with a construction period of 24 months. The project construction entity is CNNC Orient Tantalum Industry Co., Ltd.

Regarding the impact of this issuance on the company's operation and management and financial situation, CNNC Orient Tantalum Industry Co., Ltd. stated: (I) Impact of this issuance on the company's operation and management The investment projects funded by the raised capital in this issuance mainly revolve around the company's main business, aligning with relevant national industrial policies and the company's overall strategic development direction in the future, which is conducive to enhancing the company's comprehensive strength. The investment projects funded by this capital raising have good market development prospects and economic benefits, capable of enhancing the company's profitability, further strengthening its core competitiveness, achieving long-term sustainable development, consolidating and elevating its industry position, and realizing its strategic goals. (II) Impact of this offering on the company's financial situation Upon completion of this offering, the company's total assets and net assets will increase simultaneously, and the asset-liability ratio will decline, which is conducive to enhancing the company's ability to withstand financial risks, further optimizing its asset structure, reducing financial costs and risks, and strengthening its future sustainable operating capacity. With the completion of the investment projects funded by the capital raising, the scale of the company's main business can be further expanded, and the project benefits will gradually become apparent, further improving the company's financial situation.

On June 25, when answering investors' questions on the interactive platform, China National Tantalum & Niobium Co., Ltd. (hereinafter referred to as "CNTC") stated that the company has always been paying attention to the application of tantalum and niobium and their alloy materials in emerging fields, continuously increasing R&D investment and scientific research efforts, constantly improving the technological content and market competitiveness of its products, creating new growth points for emerging tantalum and niobium products, and promoting the company's high-quality development.

On June 25, when answering investors' questions on the interactive platform, CNTC stated that the company's capacity utilization is sufficient, and its current production and operation are normal.

CNTC previously released its Q1 performance announcement, stating that in Q1 2025, its revenue was approximately 338 million yuan, up 30.83% YoY; net profit attributable to shareholders of publicly listed firms was approximately 56.5 million yuan, up 13.62% YoY; and basic earnings per share were 0.1125 yuan, up 14.33% YoY.

CNTC's 2024 annual report shows: In 2024, the company achieved a total operating revenue of 1.281 billion yuan, up 15.57% YoY; and a net profit attributable to the parent company of 213 million yuan, up 13.94% YoY. The production and sales volumes of the company's processing and manufacturing products increased by 60.71% and 48.6%, respectively. By product, revenue from tantalum and niobium and their alloy products increased by 15.8%, and revenue from titanium and titanium alloy products increased by 81.94%.

In its research report commenting on CNTC, China Post Securities pointed out: Product structure optimization drives performance growth, with a steady increase in gross profit margin. The company's performance growth is mainly driven by the optimization of its product structure. Despite the downward pressure in the market for its leading products, tantalum powder and tantalum wire, the company has continued to increase its market development efforts in fields such as high-temperature alloys, semiconductors, and superconductors. In terms of profitability, the company's gross profit margin in 2024 was 18.32%, an increase of 0.48 percentage points from 2023. Project construction is in full swing, with the pyrometallurgy project fully commenced and the hydrometallurgy project entering the approval stage. (1) Completed Projects: The technical transformation project for the production line of tantalum-niobium plate and strip products, with an annual output of 100 niobium superconducting cavities, has been completed and put into operation. (2) Projects Under Construction: The production line for tantalum-niobium pyrometallurgy melting and casting products, the new intelligent production line with an annual output of 400 niobium superconducting cavities, the disposal site for waste slag from tantalum-niobium hydrometallurgy, and the construction project for the high-purity tantalum powder experimental line have all commenced. (3) Planned Projects: The feasibility study for the construction project of a digital factory for tantalum-niobium hydrometallurgy has been completed and is currently in the approval stage. Emphasis is placed on R&D investment. The performance contributions of Dongfang Superconducting and Western Materials Institute have declined, but are expected to recover by 2025. Risk Warnings: Price fluctuation risks; risks of project progress falling short of expectations; risks of downstream demand falling short of expectations; discrepancies between model assumptions and reality; policy risks exceeding expectations, etc.

Minsheng Securities' research report on Dongfang Tantalum Industry Co., Ltd. indicates that downstream demand is flourishing in multiple areas, and the expansion of production capacity is beginning to contribute incremental growth, with the tantalum-niobium main business continuing to grow rapidly. Looking ahead to 2025, orders in emerging fields remain hot, and the tantalum powder and tantalum wire businesses are expected to continue to recover. Meanwhile, the expansion of production capacity is expected to be released in a concentrated manner, with promising performance growth. Military product demand is slowing down in line with the industry, and the performance of Western Materials Institute is being dragged down, leading to a decline in investment income. In 2024, Western Materials Institute achieved a profit of approximately 230 million yuan, contributing 64.46 million yuan in investment income based on a 28% equity stake, representing a YoY decrease of 15.99%. This is mainly due to the overall slowdown in military demand and the impact of delivery schedules. As the military sector is expected to hit bottom and recover, the income of Western Materials Institute is expected to grow steadily. The company actively returns dividends to the capital market, demonstrating its confidence in its operations. As a representative of traditional state-owned enterprises, the company is implementing both market-oriented incentive reforms and continuous R&D innovation, continuously delivering results in improving quality and efficiency. As the leader in the domestic tantalum-niobium-beryllium industry, the company's main businesses of tantalum wire and tantalum powder are stabilizing and recovering, with flourishing demand in high-end emerging application fields. Along with the imminent release of expanded production capacity from the private placement project, promising performance growth is anticipated. Risk Warnings: Demand falling short of expectations, progress of new products falling short of expectations, risks of raw material price fluctuations, etc.

![Hunan Shizhuyuan Nonferrous Metals tendered today for 800 mt in physical content of bismuth concentrates in July [SMM Bismuth Market Tracking Report]](https://imgqn.smm.cn/usercenter/mLwgx20251217171723.jpeg)

![Three consecutive rare earth price rises and zirconium price adjustments push minor metals sector higher at open; Oriental Zirconium, China Rare Earth Nonferrous hit limit up [SMM Flash]](https://imgqn.smm.cn/usercenter/YhgvU20251217171725.jpg)