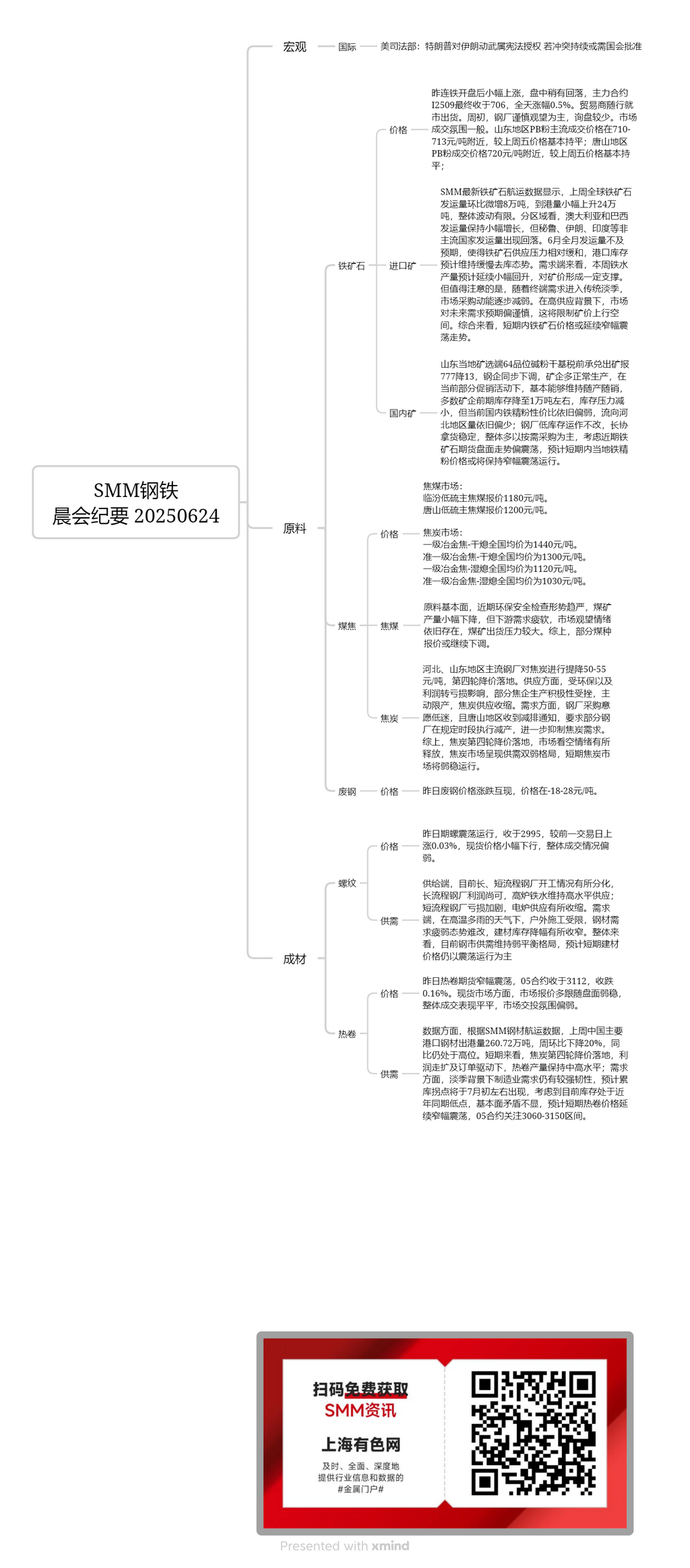

Domestic ore:

In Shandong, the ex-mine price (dry basis, pre-tax, acceptance) of 64-grade alkaline concentrate from local mines and beneficiation plants was reported at 777 yuan/mt, down 13 yuan/mt. Steel mills followed suit with price reductions. Most miners maintained normal production. Under the current sales promotions, they could basically maintain the practice of selling as they produce. The inventory of most miners had decreased to around 10,000 mt in the early stage, reducing inventory pressure. However, the cost-effectiveness of domestic iron ore concentrates remains relatively weak, and the volume flowing to Hebei remains low. Steel mills continue to operate with low inventory levels and maintain stable procurement under long-term agreements, mostly purchasing as needed. Considering the recent fluctuating trend in the iron ore futures market, it is expected that the local iron ore concentrate prices will remain rangebound in the short term.

Imported ore:

Yesterday, after the opening of the DCE Iron Ore futures, prices rose slightly before pulling back slightly during the session. The most-traded I2509 contract eventually closed at 706 yuan/mt, up 0.5% for the day. Traders sold according to market conditions. At the beginning of the week, steel mills were cautious and adopted a wait-and-see approach, with fewer inquiries. The market trading atmosphere was average. The mainstream transaction prices of PB fines in Shandong were around 710-713 yuan/mt, basically flat compared to last Friday. The transaction price of PB fines in Tangshan was around 720 yuan/mt, also basically flat compared to last Friday. According to the latest iron ore shipping data from SMM, global iron ore shipments increased slightly by 80,000 mt WoW last week, while port arrivals rose slightly by 240,000 mt, with limited overall fluctuations. By region, shipments from Australia and Brazil maintained a slight increase, while shipments from non-mainstream countries such as Peru, Iran, and India pulled back. The full-month shipments in June fell short of expectations, easing the supply pressure on iron ore. Port inventory is expected to maintain a slow destocking trend. On the demand side, pig iron production is expected to continue a slight rebound this week, providing some support for ore prices. However, it is worth noting that as end-use demand enters the traditional off-season, market purchasing momentum is gradually weakening. Against the backdrop of high supply, the market remains cautious about future demand expectations, which will limit the upside room for ore prices. Overall, iron ore prices may continue to fluctuate rangebound in the short term.

Coking coal:

The quoted price of low-sulphur coking coal in Linfen is 1,180 yuan/mt. The quoted price of low-sulphur coking coal in Tangshan is 1,200 yuan/mt. Regarding the fundamentals of raw materials, the recent tightening of environmental safety inspections has led to a slight decrease in coal mine production. However, downstream demand remains weak, and the wait-and-see sentiment in the market persists, resulting in significant pressure on coal mine sales. In summary, the quoted prices of some coal types may continue to decline.

Coke:

The nationwide average price of premium metallurgical coke (dry quenching) is 1,440 yuan/mt. The nationwide average price of high-grade metallurgical coke (dry quenching) is 1,300 yuan/mt. The nationwide average price of premium metallurgical coke (wet quenching) is 1,120 yuan/mt. The nationwide average price of high-grade metallurgical coke (wet quenching) is 1,030 yuan/mt. Mainstream steel mills in Hebei and Shandong regions proposed a price reduction of 50-55 yuan/mt for coke, marking the implementation of the fourth round of price cuts. In terms of supply, affected by environmental protection measures and the shift from profit to loss, the production enthusiasm of some coke enterprises was dampened, leading to voluntary production restrictions and a contraction in coke supply. On the demand side, steel mills' purchase willingness remained low. Additionally, the Tangshan region received an emission reduction notice, requiring some steel mills to implement production cuts during specified periods, further suppressing coke demand. In summary, with the implementation of the fourth round of coke price cuts, the bearish sentiment in the coke market has been somewhat released, and the coke market is exhibiting a pattern of weak supply and demand. In the short term, the coke market is expected to remain in the doldrums.

Rebar:

Yesterday, rebar futures fluctuated rangebound, closing at 2995, up 0.03% from the previous trading day. Spot prices declined slightly, with overall trading activity remaining weak. On the supply side, there is currently a divergence in the operating status of BF and EAF steel mills. Blast furnace steel mills are maintaining moderate profits, with pig iron production from blast furnaces remaining at a high level. In contrast, EAF steel mills are experiencing intensified losses, leading to a contraction in electric furnace supply. On the demand side, under high-temperature and rainy weather conditions, outdoor construction activities are restricted, and the weak trend in steel demand is difficult to reverse. The decline in construction material inventory has narrowed. Overall, the current steel market maintains a weak balance between supply and demand. It is expected that in the short term, construction material prices will continue to fluctuate rangebound.

HRC:

Yesterday, HRC futures fluctuated rangebound, with the 05 contract closing at 3112, down 0.16%. In the spot market, market quotes mostly followed the weak and stable trend in the futures market, with overall trading performance remaining mediocre and market trading sentiment remaining weak. In terms of data, according to SMM steel shipping data, port departures of steel from China's main ports last week reached 2.6072 million mt, down 20% WoW, but still at a high level YoY. In the short term, with the implementation of the fourth round of coke price cuts, driven by expanded profits and order demand, HRC production is expected to remain at a medium-to-high level. On the demand side, against the backdrop of the off-season, manufacturing demand still exhibits strong resilience. It is expected that the inventory buildup inflection point will appear around early July. Considering that current inventory levels are at a low point compared to the same period in recent years, with no significant contradictions in the fundamental situation, it is expected that in the short term, HRC prices will continue to fluctuate rangebound, with the 05 contract focusing on the 3060-3150 range.

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)