On June 21, the 2025 SMM (4th) Electric Drive System Conference & Drive Motor Industry Forum, jointly hosted by SMM Information & Technology Co., Ltd., Hunan Hongwang New Material Technology Co., Ltd., Louxing District People's Government, and the National-level Loudi Economic and Technological Development Zone, successfully concluded in Loudi, Hunan!

This conference encompassed a main forum, automotive electric drive system forum, eVTOL electric drive system forum, as well as various segments such as product launches, supply and demand matching meetings, and industry award ceremonies. Industry leaders, authoritative experts from research institutes, and elites from the entire industry chain gathered to engage in intense intellectual exchanges centered around the theme of "New Quality Drive, Low-Altitude Takeoff."The conference was rich in content, presenting technological developments and market trends from multiple dimensions. Participants shared forward-looking and practical insights on global industrial trends and technological breakthroughs in niche areas.In terms of market analysis, guests discussed topics such as "Global NEV Market Dynamics and Post-2025 Trends" and "China's Low-Altitude Economy Policy Advantages and Commercialization Pathways," analyzing the synergistic development relationship between the NEV and eVTOL markets in the context of global carbon neutrality goals and local industrial planning. For the low-altitude economy sector, they focused on challenges such as "Airworthiness Standards for Low-Altitude Electric Aircraft" and "Integration Difficulties in Power Systems for Multi-Rotor Flying Cars," highlighting technological challenges in the industrial scale-up process. At the technological innovation level, they shared material innovation achievements like "Industrialisation Breakthroughs in Ultra-Thin Soft Magnetic Materials" and "Lightweight Design of Magnesium Alloy Electric Drive Housings," as well as explored process upgrade issues such as "High-Voltage Platform Motor Insulation Detection Technology" and "High-Frequency Drive Motor Design Patterns." In the electric control domain, they analyzed "Inverter Brick Technology Roadmap Planning" and "Combined Application of Multi-Energy Systems in eVTOLs," outlining technological development directions from hardware design to system integration. In the industrial collaboration segment, senior analysts provided in-depth interpretations of cost structures by considering price changes in electric drive metals like copper and aluminum and supply chain security issues. They proposed comprehensive solutions for low-altitude economy data management challenges, ranging from industry chain collaboration to flight data compliance, offering practical market references for enterprises' technological upgrades and strategic planning.

Based on technology sharing, the conference analyzed challenges in implementing application scenarios, built a cross-domain collaboration platform through industrial ecosystem dialogues, and focused on development opportunities for NEV and eVTOL electric drive systems in areas such as technological iteration, industrial collaboration, and market expansion. It aimed to break down technological barriers, promote deep collaboration across the upstream and downstream of the industry chain, accelerate the ecological takeoff of the low-altitude economy and new energy transportation sectors, and inject new momentum into the high-quality development of the industry.

》Click to watch the live video of this conference

》Click to view the live photos of this conference

》Click to view the special report on this conference

Opening Remarks of the Conference

Zhou Bo, Executive Vice President of SMM

》Click to view the details of the remarks

Dai Huilei, Assistant to the Chairman of Hongwang Holding Group Co., Ltd.

》Click to view the details of the remarks

Zeng Chaoqun, Secretary of the Loudi Municipal Committee

》Click to view the details of the remarks

Award Ceremony

The 2025 SMM Electric Drive Quality Supplier List is officially released!

》Click to view the award details

The 2025 SMM Electric Drive Strategic Alliance Units are unveiled!

》Click to view the award details

Guest Speaker Presentations

June 20

Main Forum

Presentation Topic: Analysis and Future Outlook of the Global New Energy Vehicle Market

Guest Speaker: Cui Dongshu, Secretary General of the Automobile Market Research Branch of the China Automobile Dealers Association

Presentation Topic: Development and Outlook of the Low-Altitude Economy in China

Guest Speaker: Xu Changdong, President of the Western Returned Scholars Association Entrepreneurship Association, Chairman of the China Overseas-Educated Scholars Development Foundation, and Chairman of the Board of Directors of the US-China Investment Fund

Presentation Topic: Opportunities and Challenges in the Development of Low-Altitude Electric Aircraft

Guest Speaker: Yan Feng, Professor at the Civil Aviation Flight University of China and Director of the Low-Altitude Aircraft Airworthiness Verification Engineering Technology Center

Presentation Topic: Industrialisation Breakthroughs in Ultra-Thin Soft Magnetic Materials for High-Efficiency Drive Motors

Guest Speaker: Liu Huidan, Vice President of Hongwang Holding Group Co., Ltd. and Executive Director of Hunan Hongwang New Material Technology Co., Ltd.

Presentation Topic: Price and Cost Analysis of Electric Drive Metal Materials

Guest Speaker: Ye Jianhua, GM of the SMM Industry Research Department

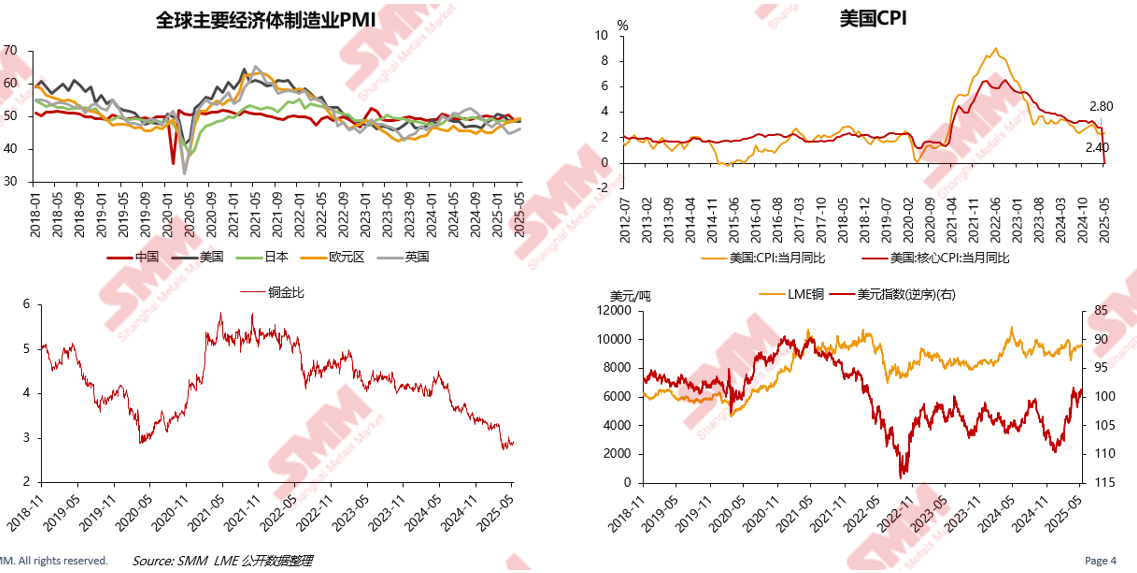

Macro - Unpredictable and Complex

The second round of high-level talks between China and the US took place in London, with the market awaiting the outcomes of the new round of talks

►SMM Analysis

ØOn May 12, substantive progress was made in the China-US economic and trade talks in Geneva, and a joint statement was issued. The content of the trade agreement exceeded market expectations, alleviating the previous market tensions. In addition, the current negotiations between the US and countries such as India and Japan have shown a mild momentum, which is conducive to the global economic recovery and has boosted copper prices.

ØOn the evening of June 5, President Xi Jinping had a scheduled phone call with US President Trump.

ØOn June 9, the second round of high-level talks between China and the US took place in London. The market expects a short-term easing of trade tensions. Currently, the first round of talks has concluded, with the US releasing positive signals and China temporarily avoiding over-committing, both leaving room for subsequent negotiations.

The manufacturing PMI of major global economies remains below 50. Affected by geopolitical conflicts and the US tariff policy, the decline in the copper/gold ratio indicates strong risk-aversion sentiment in the market.

It conducted an analysis by considering the trend changes in the manufacturing PMI of major global economies, the US CPI, the copper/gold ratio, LME copper, and the US dollar index.

The "stagflation" and "recession" in the US economy are disrupting global asset prices.

It conducted an analysis by considering factors such as the yields on US long-term and short-term government bonds, the previous value of the change in US non-farm payrolls, the University of Michigan Consumer Sentiment Index, the University of Michigan Consumer Current Conditions Index, the University of Michigan Consumer Expectations Index, the US: Markit Manufacturing PMI (final), and the US: Markit Services PMI: Business Activity (final).

Major economic indicators in Europe have begun to improve, and large-scale infrastructure investment funds have been established to boost the economy.

It provided an introduction from the perspectives of the gradual reduction in eurozone interest rates and the slowdown in the decline of construction and retail confidence in the eurozone.

The domestic consumer market needs further stimulation, the export market will face greater challenges, and local government bond issuance has been rapid.

It interpreted the data changes from China's export situation, consumer confidence, the sustained growth in household savings, the monthly total issuance of local government bonds, the inventory area, construction area, and completion area of the real estate industry.

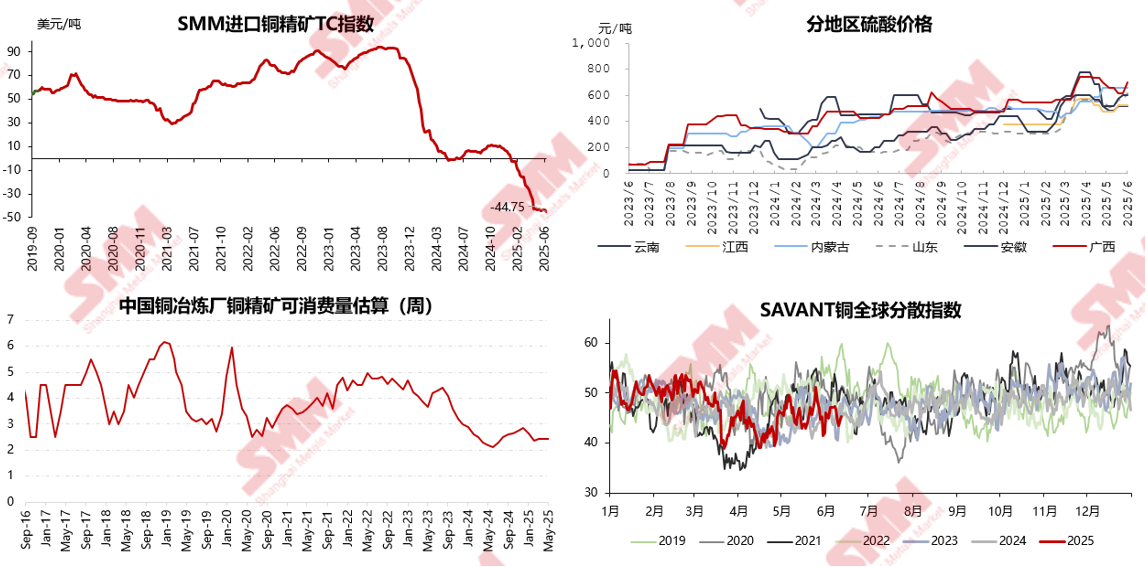

Copper and Aluminum Supply

The increase in global copper mine production mainly comes from expansion projects.

It elaborated on the expected increase in new expansion and newly commissioned projects of major global copper mines from 2020 to 2023.

The rapid global expansion of copper smelter capacity makes it difficult to change the tight raw material supply situation.

Domestically, the growth rate of refined copper capacity in the future will still be higher than that of crude copper capacity, and the resulting gap theoretically needs to be filled by copper anodes and copper scrap.

Overseas, although there will be an expansion in copper anode capacity in the future, it is fundamentally a transfer of copper concentrate raw materials. Due to the interference of copper concentrate raw material shortages, it is difficult to achieve the goal of increasing crude copper capacity, which may lead to a decline in global crude copper production and an expansion of the actual gap with refined copper capacity.

The shortage of copper concentrates intensifies, and the deterioration of the supply-demand structure in the short term is difficult to reverse.

It conducted an analysis by considering data such as the expected global copper concentrate supply-demand balance results from 2021 to 2030 (including supply and demand-side interference rates), the annual long-term contract benchmark TC for copper concentrates, and the comparison of advantages in copper smelting raw materials.

Under the tight supply of copper concentrates, processing fees continue to decline, and smelter losses expand.

It conducted an analysis by considering factors such as the SMM Import Copper Concentrates TC Index, regional sulphuric acid prices, estimates of the consumable amount of copper concentrates by Chinese copper smelters, and the SAVANT Global Copper Dispersion Index.

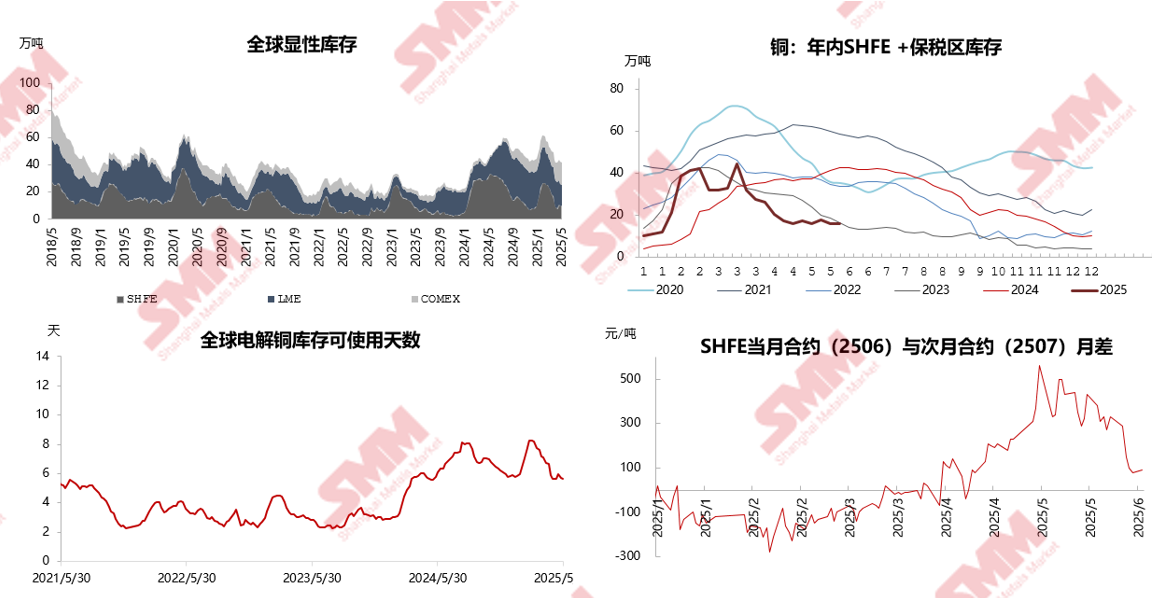

In late April, the LC price spread widened again, with some imported B/Ls being re-exported to the US.

In late April, the LC price spread widened again. The US continued to attract supply, while the supply gap in Chile and logistical issues in the DRC will continue to push up China's spot aluminum premium. A large number of LME Asia warrants were canceled, providing support for the LME backwardation structure.

Supply tightness expectations are being realized, and the risk of copper futures squeeze has increased.

As of May 2025, global visible inventory has further declined, and the number of available days for global copper cathode has continued to decrease. The market has strong borrowing funds. Under the risk of a squeeze, both domestic and overseas copper prices may rise in stages.

In May, aluminum cost dropped back slightly, while in June, the cost breakdown showed mixed performance.

According to SMM data, the average tax-inclusive full cost of China's aluminum industry in May 2025 was 16,333 yuan/mt, down 0.3% MoM and 5.1% YoY. During the period, disruptions in the bauxite sector in mid-May boosted alumina futures prices rapidly, with spot prices following with a slight delay. Moreover, the alumina spot price trend was lower in the first half of the month and higher in the second half. Therefore, the average monthly alumina price increase in May was limited, and it is expected to rise significantly in June.

►SMM Analysis

As of June 2025, the upward momentum for the average monthly alumina price still exists; auxiliary material costs are weakening; and electricity costs are declining. Overall, the aluminum cost may show a slight downward trend.

In summary, SMM expects the average tax-inclusive full cost of China's aluminum industry in June 2025 to be around 16,000-16,300 yuan/mt.

June 21

Automotive Electric Drive System Forum

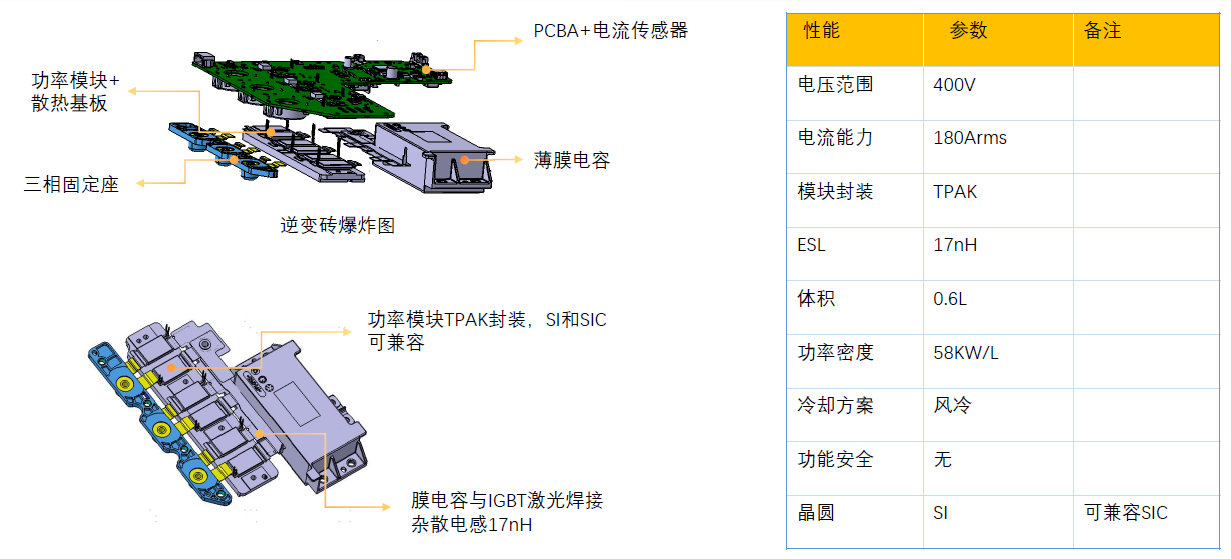

Speech Topic: Technical Planning for Electric Control Inverter Brick

Guest Speaker: Zhong Jingwen, Drive Module Expert, Joynext Powertrain Systems Co., Ltd.

I. Inverter Brick Planning

II. Inverter Brick Gen1 Display

Inverter Brick Gen1 Display (Low Power Segment TPAK)

He also analyzed the Inverter Brick Gen1 Display (Medium Power Segment TPAK Parallel), Inverter Brick Gen1 Display (High Power Segment HPD), Inverter Brick Gen1 Display (Dual Electric Control), and other contents.

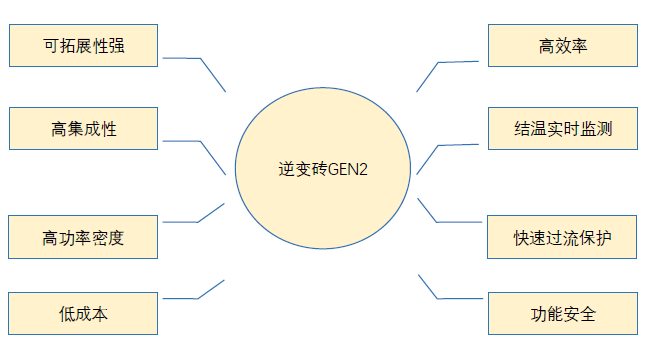

III. Inverter Brick Gen2 Display

Inverter Brick-Gen2 Demand Analysis

Performance Improvement Requirements for Gen2 Inverter Brick:

• Low stray inductance to reduce switching losses and adapt to SIC applications;

• Platform-based design with high compatibility (voltage platform, SIC & IGBT);

• Improved accuracy and effectiveness of junction temperature monitoring;

• Rapid overcurrent protection to adapt to SIC applications;

• Efficient heat dissipation and high power density;

• Improved junction temperature resistance of power modules;

• Cost optimization.

Inverter Brick - Gen2

Medium-power Platform Inverter Brick (<150kW):

• Compatible with 400V and 800V platforms;

• Compatible with IGBT and SIC power modules.

High-power Platform Inverter Brick (<250kW)

• Compatible with 400V and 800V platforms;

• Compatible with IGBT and SIC power modules.

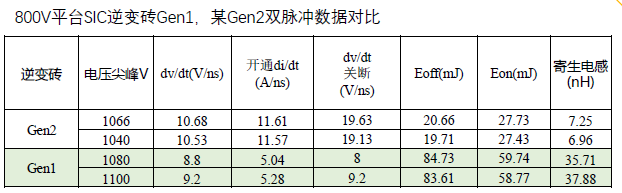

Inverter Brick Gen2 - Low Stray Design and Integrated Capacitor Potting

Low Stray Design: The DC-Link capacitor optimizes the busbar and core design, with stray inductance controlled at <2nH. Laser welding technology is used for the power module terminal connections, with overall stray inductance controlled at <5nH.

Integrated Capacitor Potting: The DC-Link capacitor and the housing water channel are integrally potted, effectively reducing costs, minimizing volume, and enhancing the core's heat dissipation capacity.

• The stray inductance of the Gen2 inverter brick system can be reduced to 8nH, a 75% reduction compared to Gen1. Under the same voltage critical peak conditions, switching losses are reduced by 70%, significantly improving the efficiency and output capacity of the SIC module.

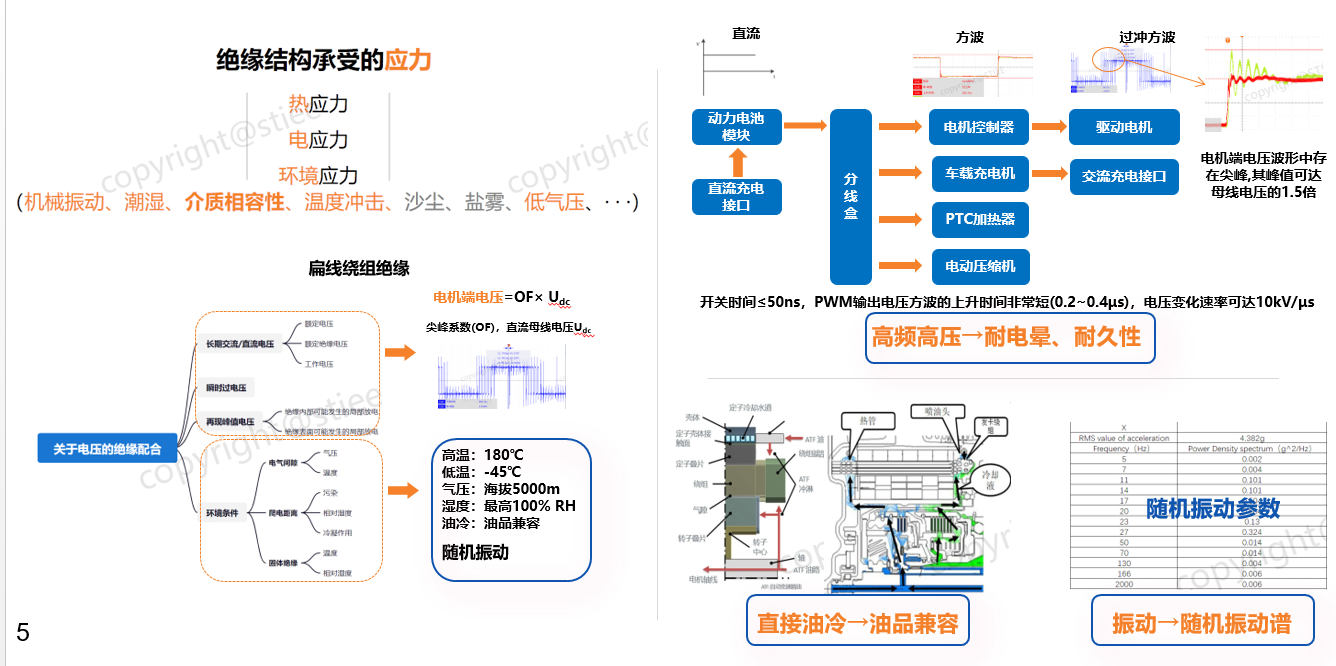

Speech Topic: Discussion on the Detection and Evaluation Technology of Drive Motor Insulation under High-voltage Platforms

Guest Speaker: Wang Shuangcan, Technical Director, Technology Development Department, STIEE - Transportation Energy Division, Shanghai Electrical Apparatus Research Institute (Group) Co., Ltd.

Characteristics of Drive Motor Insulation under High-voltage Platforms

1. Stresses and Characteristics Borne by Insulation

Stresses Borne by Insulation System: Thermal stress, electrical stress, and environmental stress.

Standard Dynamics of Insulation Detection and Evaluation

2. Standard Dynamics: Development History

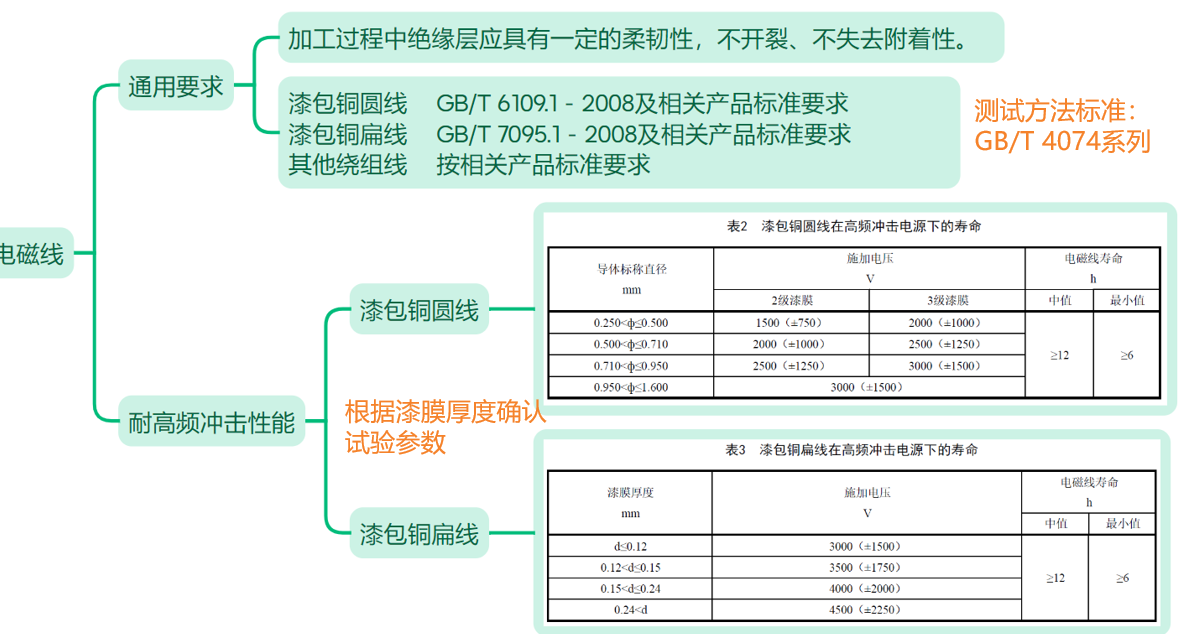

2017: The group standard "Technical Requirements for Insulation Structure of Drive Motors for New Energy Vehicles" was initiated.

2018: A series of research and verification tests were conducted on oil compatibility, round wire resistance to high-frequency impact, insulation structure heat resistance, and voltage durability.

2019: The 2019 edition of "Technical Requirements for Insulation Structure of Drive Motors for New Energy Vehicles" was released.

2022: With rapid technological iterations, especially the rapid application of flat wire insulation structures, the "Technical Specification for Insulation Structure of Drive Motors for New Energy Vehicles" was revised.

2023: A series of research and verification tests on oil compatibility of flat wire insulation structures, round wire resistance to high-frequency impact, insulation structure heat resistance, and voltage durability were conducted, and the 2023 edition was formed.

2025: The national standard GB/T "Technical Specification for Insulation Structure of Drive Motors for New Energy Vehicles" was initiated.

2-Standard Updates: Standard Architecture

It introduces the GB/T technical specification for the insulation structure of NEV drive motors.

2-Standard Updates: Technical Requirements for Magnet Wires

2-Standard Updates: Technical Requirements for Insulating Component Materials

It elaborates on insulating component materials and insulation structures.

2-Standard Updates: Technical Requirements for Oil Resistance of Insulating Components

• After the oil resistance test of the insulation structure, there should be no visible damage to the appearance.

Presentation Topic: Development of Magnesium Alloy Electric Drive Housings and Lightweight Design

Guest Speaker: Ph.D. from Shanghai Jiao Tong University Xu Bin

Development Background of Magnesium and Electric Drive Housings

Development Background of Magnesium

• Magnesium materials are a key support for emerging industries.

• Production Resources: Rich in ore reserves, with good supply availability.

China has proven reserves of dolomite exceeding 4 billion mt; magnesium is low-cost and can be controlled in the long term.

National Guidance: An emerging metal strongly supported by the Ministry of Science and Technology and the Ministry of Industry and Information Technology (MIIT)

In the past, innovation in magnesium alloy automotive parts was mainly driven and developed by high-end internal combustion engine vehicle manufacturers such as BMW, Mercedes-Benz, and Ford, but the scale of their applications was relatively small. Even now, the most widely produced magnesium alloy parts in global vehicles are still mainly used in dry areas of the vehicle.

For NEVs, the demand for lightweighting is more urgent.

New Technological Developments

Principle of Magnesium Alloy Semi-Solid Injection Molding

The magnesium alloy semi-solid injection molding process falls under the category of thixocasting technology. Magnesium particles enter the barrel from the hopper under the action of gravity or negative pressure. Inside the barrel, the rotation of the screw, combined with the heat provided by an external heater (the barrel is usually divided into 5 to 7 sections, with the temperature gradually increasing from the feed inlet to the nozzle), heats and shears the magnesium alloy particles as they are conveyed forward. In the middle of the barrel, the magnesium alloy undergoes thermoplastic deformation due to the compression of the screw's compression section, achieving densification. When it continues to reach the storage section at the front end of the screw, it has transformed into a semi-solid slurry that is partially molten and contains spherical solid phases. This slurry possesses excellent liquidity and mold-filling properties. Subsequently, the slurry is injected into the mold at high speed through the nozzle, rapidly cooling and solidifying under high speed and pressure, thereby forming parts with a certain shape and size. After the injection is completed, the frontmost part of the nozzle cools down to form a cold plug for self-sealing, enabling continuous molding operations without the need for protective gas or complete melting.

Magnesium Alloy Semi-Solid Injection Molding (Thixomolding) Technology

Advantages of magnesium alloy semi-solid injection molding technology compared to traditional liquid die casting:

(1) High safety. Magnesium alloys are flammable in their liquid state. However, the semi-solid injection molding process integrates thixotropic slurry making and molding under self-sealed conditions, eliminating the need for high-risk magnesium melting furnaces and the step of transferring molten magnesium, thus ensuring the safe production of magnesium alloy parts.

(2) Environmentally friendly. Traditional casting processes generate a large amount of volatile gases when melting magnesium alloys and require the additional use of SF6 as a protective gas, which can cause environmental damage and limit the application and development of magnesium alloys. In contrast, the semi-solid injection molding process does not require complete melting or protective gas during the production of magnesium alloy parts, and does not produce melting waste slag, making it a green manufacturing technology.

(3) Fewer oxide inclusions. The temperature of the semi-solid molding process is lower than that of traditional casting processes, significantly reducing the risk of oxidation. Meanwhile, since the injection molding method prevents the molten magnesium from directly contacting the external air, the probability of introducing oxide inclusions during the molding process is almost eliminated.

(4) Fewer gas porosity defects. Liquid magnesium tends to form turbulent flow when filling the mold cavity, leading to the generation of porosity defects. In contrast, semi-solid magnesium alloys exhibit non-Newtonian fluid characteristics and are more inclined to fill in a laminar flow manner, effectively reducing the gas porosity phenomenon during the molding process and resulting in denser castings.

(5) Superior mechanical properties. Magnesium alloys formed by semi-solid injection molding exhibit a non-dendritic solidification structure. Under high cooling rate conditions, their average grain size and second phase size are extremely fine. Additionally, due to the reduction in defects such as porosity and inclusions, they possess superior strength and toughness.

(6) High dimensional accuracy. Semi-solid magnesium alloys have good molding capabilities, enabling near-net-shape forming of complex thin-walled structures. With relatively small solidification shrinkage and improved resistance to hot cracking, the dimensional accuracy of the castings produced is high.

(7) Long mold life. The molding temperature of the semi-solid process is nearly 100℃ lower than that of traditional die casting processes, significantly reducing the thermal shock of the molten magnesium on the mold and thereby extending the mold life. For example, when producing some thin-walled parts, the service life of semi-solid molds can reach over 200,000 to 400,000 mold cycles.

(8) High material utilization rate. Magnesium alloy parts prepared by die-casting process generally have a raw material utilization rate below 50% due to the inclusion of a large amount of gating and runner systems. In contrast, the semi-solid forming process can significantly reduce the size of the sprue and simplify structures such as runners and overflow channels, thereby increasing the raw material utilization rate to over 70%.

(9) High product yield. The semi-solid injection molding process precisely controls the temperature of magnesium alloy, ensuring stable material filling quality and eliminating pre-crystallization issues that may occur during die-casting. With fewer defects, this directly translates to high internal and surface quality of the product, which maintains a high yield even after subsequent processing.

(10) Reduced energy consumption. The semi-solid forming process for magnesium alloy is equally efficient in terms of cycle time as the die-casting process. Thanks to the advantages of not requiring a furnace and lower forming temperatures, the semi-solid forming process can save at least half of the electrical energy compared to liquid die-casting production.

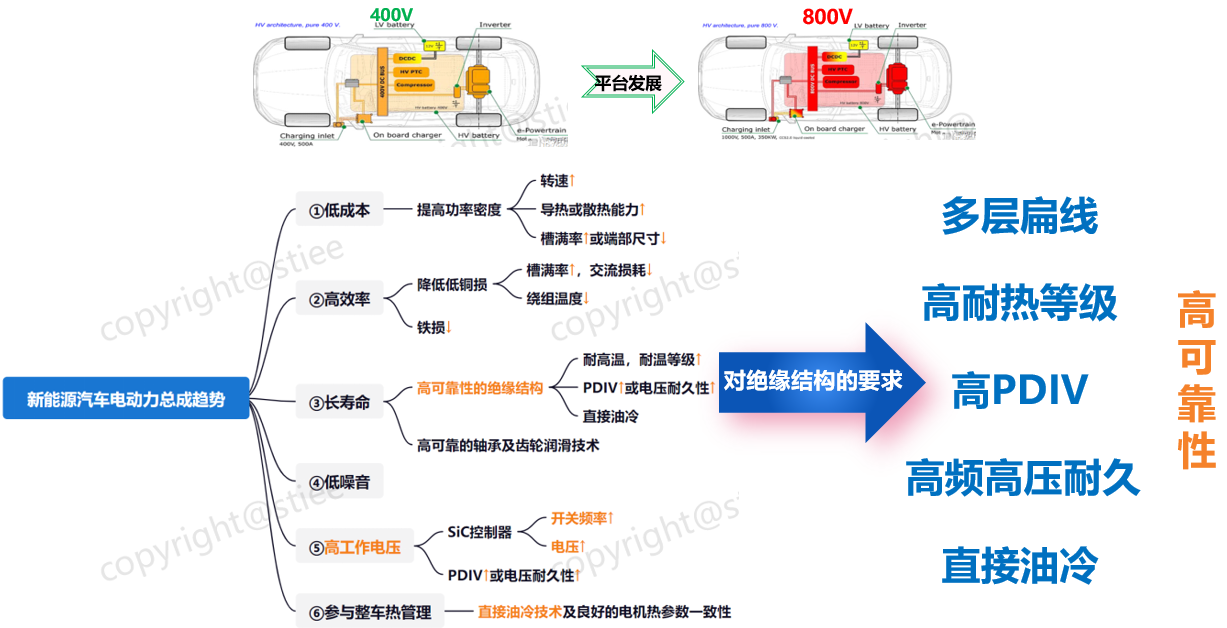

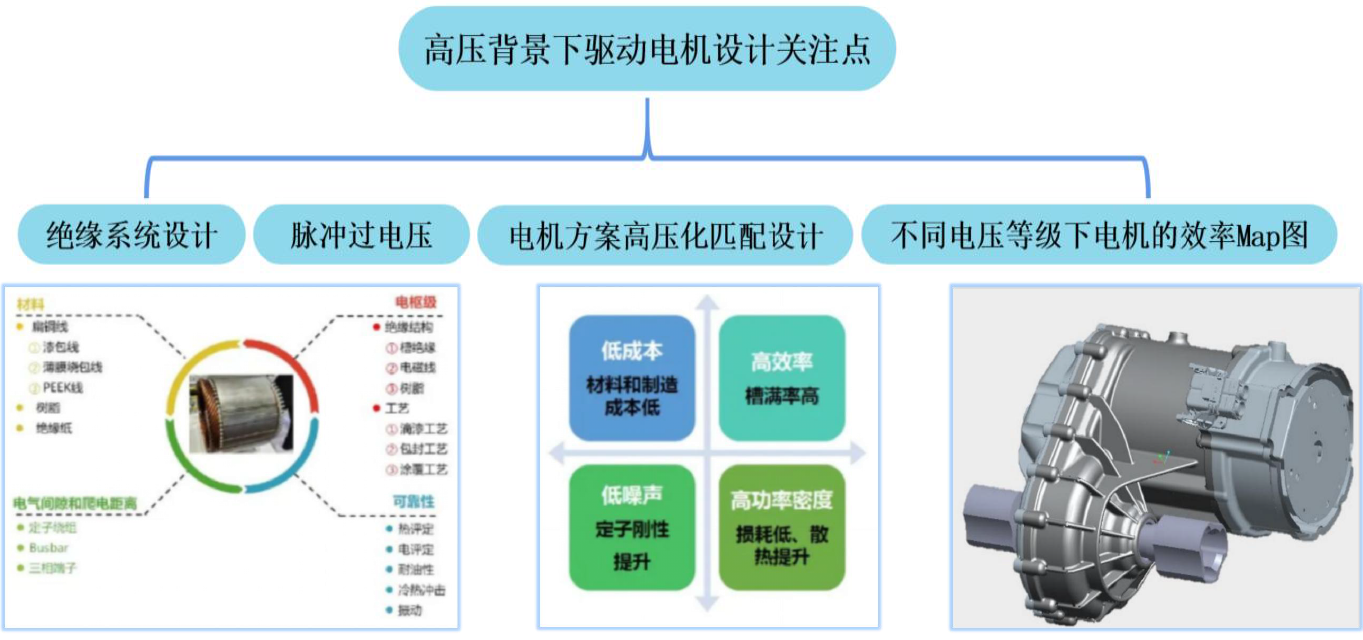

Speech Topic: Design Characteristics of Drive Motors in the Context of High Voltage and High Frequency

Guest Speaker: Jia Yuqi, Deputy Dean of the Research Institute, Zhejiang Electric Drive Innovation Center

Background and Challenges

1.1 Background - Policy/Industry

The drive motor of EVs has a wide speed range and requires frequent acceleration and deceleration during driving, making the operating conditions much more complex than those of general speed control systems. The electric drive system is crucial for determining the power performance of EVs.

• US Department of Energy (DOE) 2025 EV Development Plan;

• Increasing consumer focus on driving range and performance;

• Best practices of local automotive brands in "overtaking on curves" in the global automotive industry;

• An important approach to achieving "low-carbon environmental protection, carbon peak, carbon neutrality, energy conservation, and emission reduction";

Requires the electric drive system to be lighter, more compact, more efficient, and more reliable, with increasing demand for power density.

1.1 Background - Electric Drive System Solutions/Components and Windings

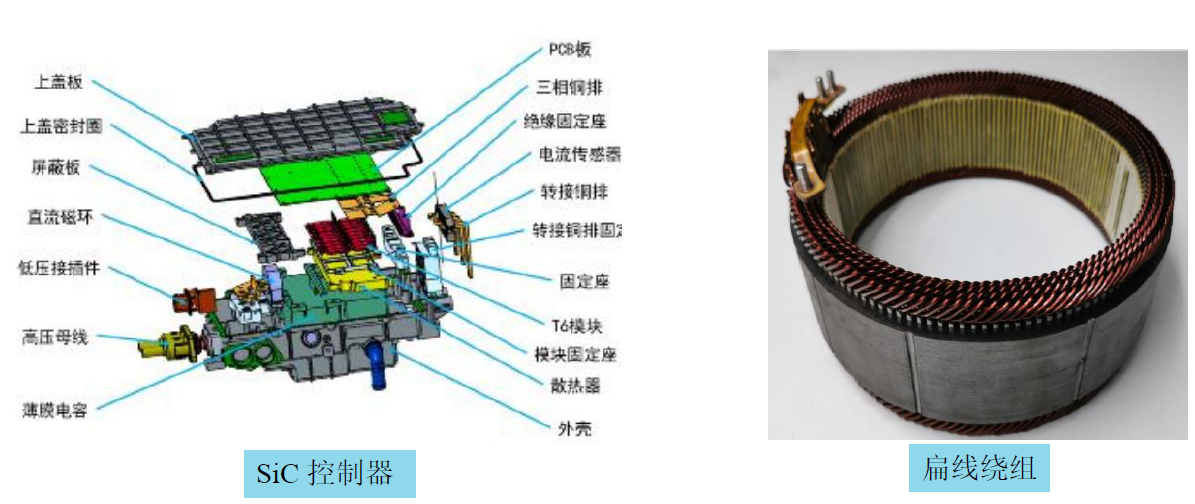

SiC inverters feature high switching frequency, low losses, and high working voltage, contributing to increased drive motor speed and power density;

Flat wire windings have high slot fill factor, low DC resistance, and good thermal conductivity, contributing to improved motor efficiency and power density under medium and low-speed operating conditions;

1.1 Background - Electric Drive System Solutions

Mainstream solution for electric drive systems in new energy vehicles: SiC inverter + flat wire winding permanent magnet synchronous motor;

1.2 Technical Difficulties and Challenges - High Voltage and High Frequency

High voltage increases dielectric losses in insulating materials and raises the risk of partial discharge;

High frequency increases AC losses in flat wire windings, and the distribution of losses within the slot is uneven, leading to local hot spots;

Under high voltage and high frequency conditions, the effect of high-frequency parasitic parameters exacerbates uneven voltage distribution between coil turns, causing insulation damage and failure;

1.2 Technical Difficulties and Challenges - Countermeasures

Fully consider the uneven distribution of losses, heat, and voltage stress during the early design stage;

Use high-temperature and high corona-resistant insulating varnish, insulating materials, and enamelled wire;

Comprehensive countermeasures from multiple aspects, including new motor topologies, new winding structures, new materials, new processes, and efficient thermal management systems;

Key Considerations in Drive Motor Design under High Voltage

2 Key Considerations in Drive Motor Design under High Voltage

2.1 Insulation System Design - Materials

Under high-frequency and high dv/dt excitation, the winding insulation will be subjected to significant electrical and thermal stresses. Given the demand for high power density and high reliability, the insulation safety margin of the motor gradually approaches the allowable limits of material parameters. Therefore, it is necessary to conduct safety analysis and determination of turn-to-turn insulation in the motor during the initial design stage. To ensure insulation safety margin and avoid damage and premature failure, measures such as increasing insulation thickness, using insulation materials with higher temperature resistance ratings, and corona-resistant insulation materials can be adopted to ensure insulation safety. For example, the corona-resistant PEEK wire developed by Furukawa Electric and used in Honda's iMMD drive motor can achieve higher PDIV and better thermal conductivity.

2.1 Insulation System Design - Cooling

As the power density of the motor increases, the loss density inevitably increases as well. Coupled with the effects of proximity and skin effects under high-frequency conditions, this can easily lead to uneven heat source distribution within the motor slots, resulting in localized overheating.

The lifespan of motor insulation materials is closely related to temperature. Therefore, attention should be paid to the motor's thermal management plan, and the development of efficient cooling structures, such as cooling within the winding slots and direct winding cooling, should be strengthened.

2.2 Pulse Overvoltage - Causes and Calculation Models

Due to the inconsistency in characteristic impedance among the inverter, transmission cables, and motor, according to the wave reflection principle, PWM pulse waves will be reflected multiple times between the inverter and motor windings. The superposition of reflected and incident voltages will generate pulse oscillation voltages at the motor winding ends that are higher or lower than the bus voltage, thereby generating pulse voltages. Among these, the peak voltage is the most dangerous factor leading to partial discharge in motor insulation.

Roundtable Discussion: Development Path of Electrification Technology for New Energy Vehicles

Moderator: Song Zhihuan, Chief Expert of Huayu Electric System Co., Ltd.

Guest Speaker: Liu Shucheng, Electric Drive Technology Director of Shenxiang Technology Co., Ltd., Deputy General Manager of Changxing Shenxiang Technology Co., Ltd.

Fang Weirong, Chief Transmission System Engineer of SAIC Motor Commercial Vehicle Technical Center

Zhang Guangjie, Chief Engineer of New Energy Powertrain Product Platform of Zhuzhou Gear Co., Ltd.

Liu Pingzhou, Former Chief Engineer of Neta Auto

》Click to View Interview Details

eVTOL Electric Drive System Forum

Speech Topic: Key Technologies for the Development of Multi-Rotor Flying Cars

Guest Speaker: Han Yi, Professor of Chang'an University/Postdoctoral Fellow of Tsinghua University

Speech Topic: Application of Diversified Energy Systems in eVTOLs

Guest Speaker: Wang Yunzhong, Chief Engineer of R&D Headquarters of Dongfeng Motor Group Co., Ltd.

01 Opportunities and Challenges in the Development of the Low-Altitude Economy

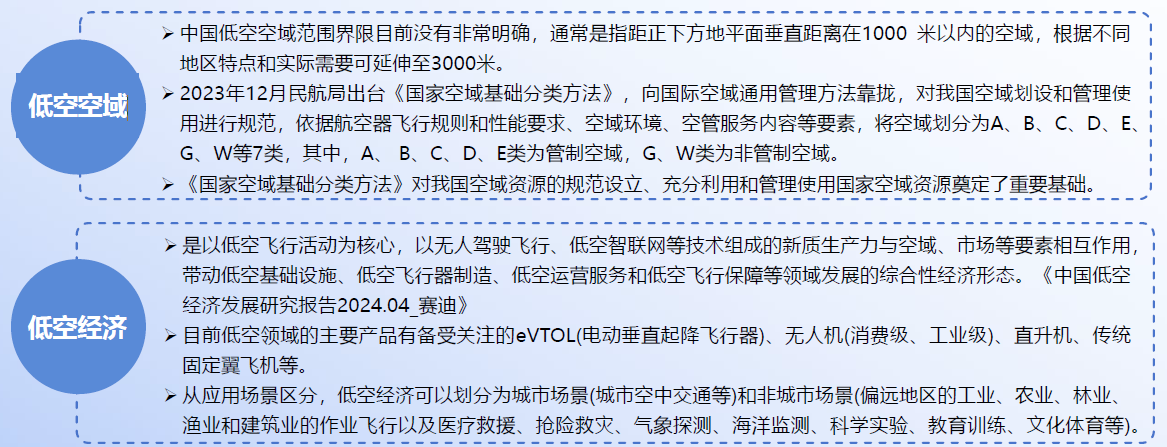

Opportunities and Challenges in the Development of the Low-Altitude Economy - Definition of the Low-Altitude Economy

The low-altitude economy is a comprehensive industrial form driven by multi-scenario low-altitude flight activities, composed of new quality productive forces such as low-altitude aircraft and low-altitude intelligent networking technologies, which radiates and promotes the integrated development of industries including low-altitude manufacturing, low-altitude flight, low-altitude support, and comprehensive services.

The airspace height range involved in the low-altitude economy is below 1,000 meters, and can be extended to within 3,000 meters according to the characteristics and practical needs of different regions. The flight altitude of manned vertical takeoff and landing aircraft is generally below 300 meters.

Opportunities and Challenges in the Development of the Low-Altitude Economy - Three Major Aircraft in the Low-Altitude Economy

The manufacturing of low-altitude aircraft is the most important physical industry among the four major sectors of the low-altitude economy. Low-altitude aircraft mainly include traditional helicopters, various drones, and flying cars.

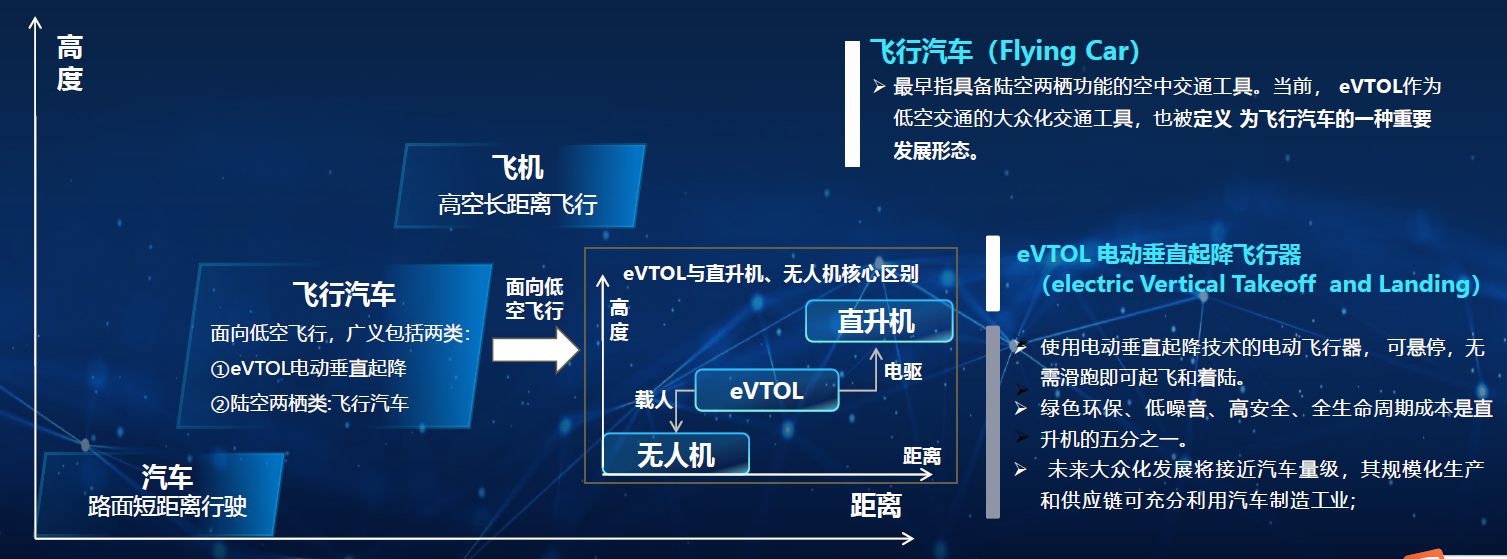

In a broad sense, flying cars refer to vehicles designed for low-altitude intelligent transportation and three-dimensional smart transportation, mainly including two major types: amphibious cars and electric vertical takeoff and landing aircraft (eVTOL) (excerpted from the "White Paper on the Development of Flying Cars").

Flying Car

Originally referred to air vehicles with amphibious functions on land and in the air. Currently, eVTOL, as a popular means of transportation for low-altitude travel, is also defined as an important development form of flying cars.

eVTOL (electric Vertical Takeoff and Landing)

An electric aircraft that uses electric vertical takeoff and landing technology, capable of hovering and taking off and landing without a runway.

It is environmentally friendly, low-noise, highly safe, and its total life cycle cost is one-fifth that of a helicopter.

In the future, its popularization will approach the scale of automobiles, and its large-scale production and supply chain can fully leverage the automotive manufacturing industry.

Drones, helicopters, and eVTOLs (Electric Vertical Take-off and Landing, eVTOL) are the three major physical carriers for realizing the low-altitude economy.

Compared to drones, eVTOLs have a wider range of functions on the basis of carrying passengers and cargo. Compared to helicopters, eVTOLs have advantages such as low carbon emissions, low noise, low cost, no need for runways, and good stability, gradually becoming the mainstream solution for urban air mobility.

Opportunities and Challenges in the Development of the Low-Altitude Economy - Low-Altitude Application Scenarios

It lists scenarios such as production operations, public services, and aviation consumption.

Commercialization path: Prioritize rigid demands in non-urbanized scenarios, conduct pilot projects in urban scenarios first, and achieve full-domain integration in the later stage.

Opportunities and Challenges in the Development of the Low-Altitude Economy - Development Opportunities

The low-altitude economy has received significant attention from national policies, with frequent policy releases and the gradual opening of low-altitude airspace to promote its development.

It aligns with the future development trends of three-dimensional, electric, and intelligent transportation, representing a blue ocean market that urgently needs to be developed.

High altitude: Aircraft ⇒ Flight (Considering safety factors and aviation control requirements, it is difficult to significantly increase the flight speed of civil aviation);

Low altitude: None ⇒ Flying car (Point-to-point solution for the last mile, addressing urban congestion and improving traffic efficiency);

Ground: Cars, public transportation, rail transportation ⇒ Unchanged (but with an expanded scope of personalization, deeper intelligence, widespread Internet of Things, and urban smartization);

Underground: Subway ⇒ Subway (It is predicted that there will be relatively small changes within the next 30 years);

The transportation form in the next 10-20 years will be a "highly intelligent three-dimensional transportation network dominated by new energy."

The advancement of electrification and intelligent technologies in NEVs has propelled the development of low-altitude flight vehicles toward electrification and intelligence.

The large-scale production capabilities, mature industry chain, and application of electrification technologies in the automotive sector can significantly reduce the cost of flight vehicles, making mass adoption and widespread use a future possibility.

Opportunities and Challenges in the Development of the Low-Altitude Economy—Challenges

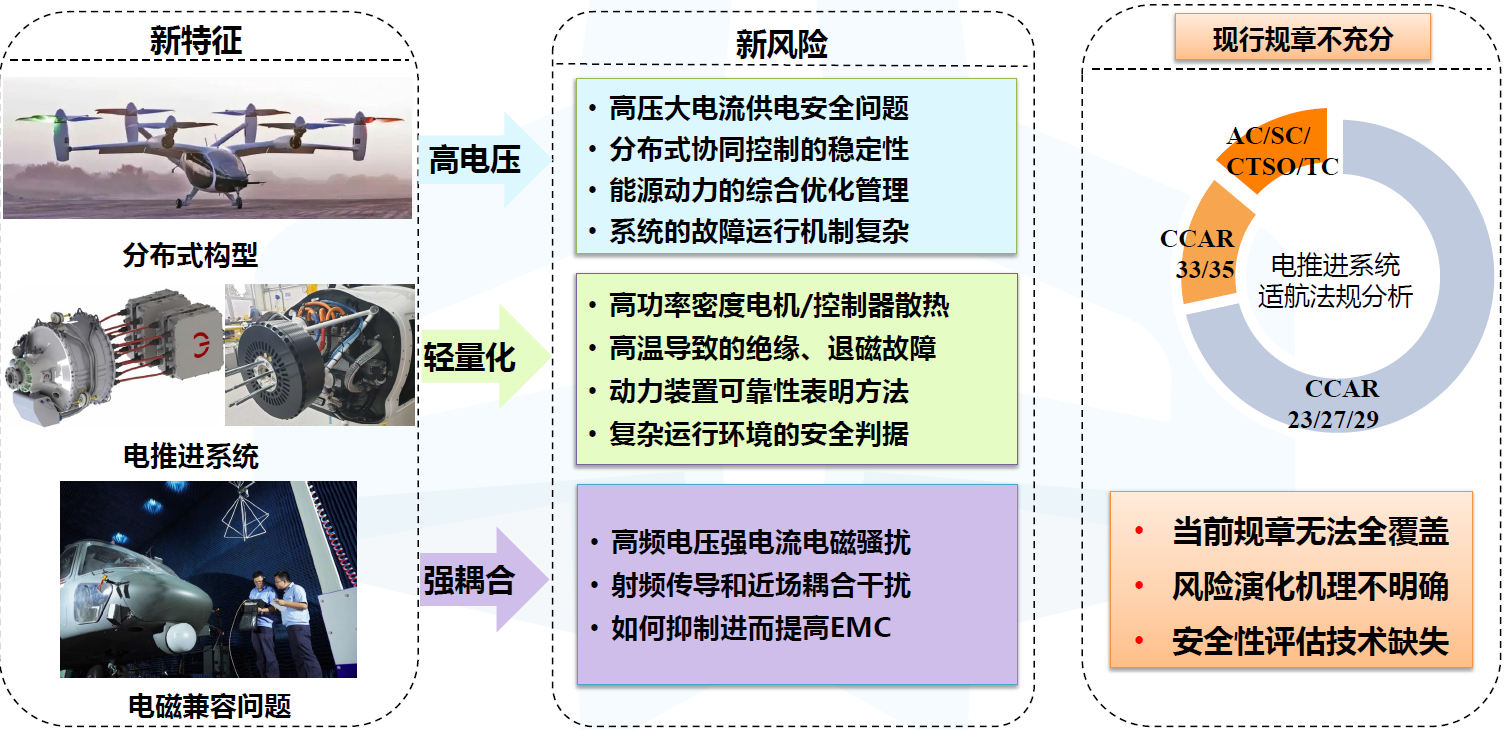

►As a cross-industry integrated product, eVTOL faces unclear regulatory responsibilities, lacking unified regulations, standards, and airworthiness certification, among other common challenges.

Currently, each project is evaluated on a case-by-case basis under civil aviation airworthiness conditions, with specific requirements tailored individually, resulting in lengthy cycles. There is an urgent need for relatively unified certification standards.

►Technological breakthroughs are still required, with insufficient market traction and supporting infrastructure, and business models yet to be explored.

Key technological bottlenecks include inadequate driving range, weak communication security, and insufficient safety, obstacle avoidance, and noise reduction technologies.

Infrastructure shortages encompass airspace management, takeoff and landing site construction, and energy support networks.

Lack of market traction stems from insufficient consumer awareness, high market prices, and limited application scenarios.

Insufficient industry integration involves communication, navigation, and surveillance systems, incomplete operational supervision and management, and inconsistent cross-industry standards.

In the early stages of development, national and local governments need to provide more policy guidance and support to promote industry growth and infrastructure improvement.

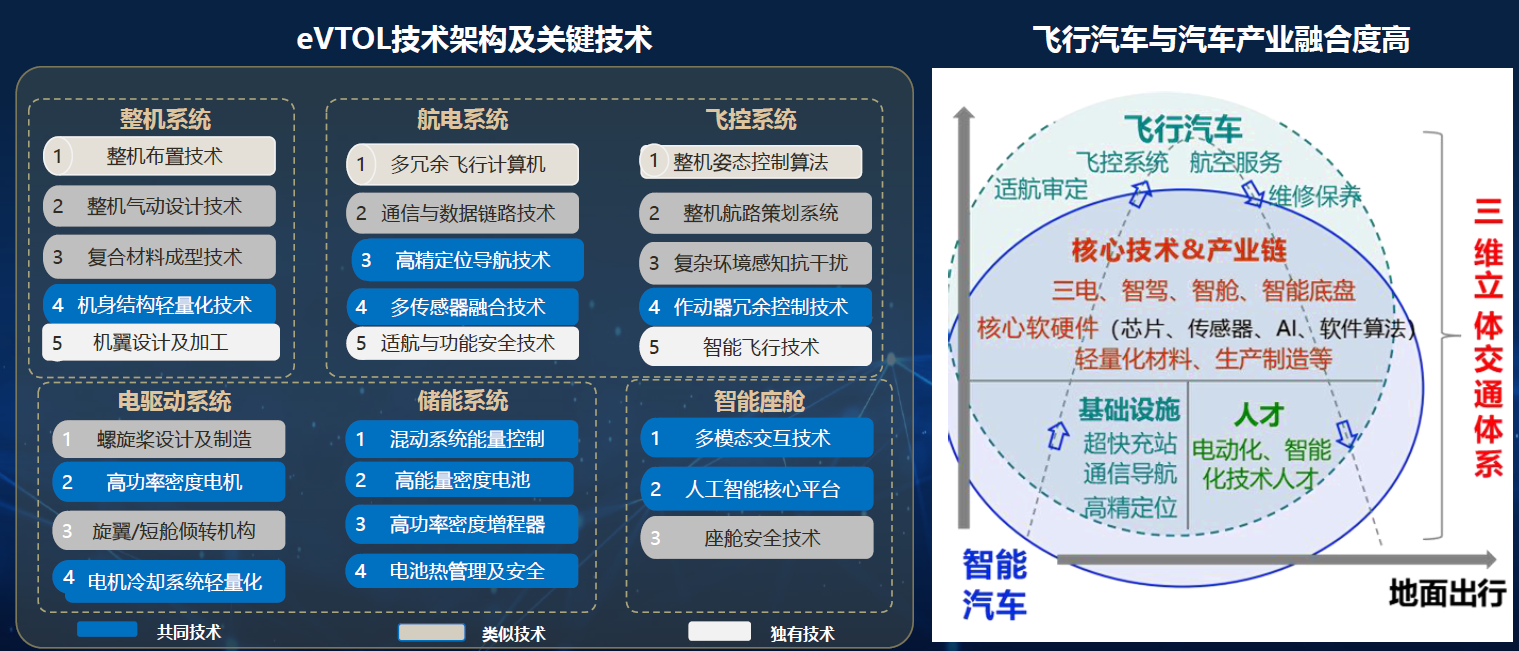

02 eVTOL Technical Pathways and Key Technologies

eVTOL Main Technical Pathways and Key Technologies—Technical Pathways

Technical pathways and configurations will be selected based on different application scenarios and stages of technological development, with multiple pathways and configurations coexisting.

From a technological development trend perspective, tiltrotors are gradually becoming mainstream, and as the industry and technology further advance, they will evolve toward land-air integration.

eVTOL Main Technical Pathways and Key Technologies—Technical Architecture

Smart cabins, autonomous driving, power and ESS share commonalities with NEV technologies, enabling complementary advantages in the industry chain, integrated innovation, and collaborative development.

The automotive industry's supply chain and economies of scale help reduce eVTOL costs, while established sales channels facilitate broader adoption.

Automakers are emerging as key players in the flying car sector, not only enhancing brand value through cross-industry ventures but also investing in flying car development and low-altitude operations.

Amid cut-throat competition in the NEV industry, companies are positioning themselves early for future transportation paradigms, seeking opportunities to "overtake on a new track," with flying cars representing a critical future direction.

Speech Topic: Rethinking the Industry Chain and Data Management Challenges in the Low-Altitude Economy

Guest Speaker: Li Gang, Deputy General Manager of the Low-Altitude Economy Division at Rudong Information Technology Services (Shanghai) Co., Ltd., and Certified Expert by the China Federation of Logistics & Purchasing (CFLP)

I. Connotation and Strategic Value of the Low-Altitude Economy

Concept Definition and Industry Landscape

• The low-altitude economy is a comprehensive economic form driven by various low-altitude flight activities involving manned and unmanned aircraft, which radiate and promote the integrated development of related industries.

• The low-altitude economy relies on low-altitude airspace, with general aviation as the leading industry, and has a strong driving effect and a long industry chain. It is closely integrated with high-tech innovations such as scenario innovation, new material applications, and artificial intelligence.

• The low-altitude economy is widely reflected in the primary, secondary, and tertiary industries, and will play an increasingly important role in promoting economic development, strengthening social security, and serving national defense undertakings.

• The essence of developing the low-altitude economy at present: transforming low-altitude elements into scenarios and scenarios into economic activities.

• Characteristics of the low-altitude economy: It is an industry chain-based economy with multi-domain, cross-industry, and full-chain characteristics. It integrates new-type low-altitude production and service methods with traditional general aviation formats, relying on information and digital management technologies. The development of the low-altitude economy plays an important role in promoting economic development, strengthening social security, and serving national defense undertakings.

Main Categories of Low-Altitude Airspace Flights

• Low-altitude passenger and cargo transportation: Whether it is manned or cargo transportation by fixed-wing aircraft or helicopters, it offers significant advantages such as flexibility, convenience, efficiency, and accuracy, making it an important tool for future urban and rural transportation and rapid logistics. Vertical takeoff and landing drones will be the primary method for the last-mile delivery of rapid cargo transportation in mountainous, remote, and sparsely populated areas.

• Low-altitude operational flights: Such as industrial construction operations, smart agriculture, airborne medical instruments, spraying systems, aerial remote sensing systems, and hoisting systems.

• Aviation emergency rescue: Ensuring safety, speed, and accessibility.

• Low-altitude tourism and leisure: Emphasizing safety, practicality, and economy.

The low-altitude economy will become an important engine for new growth in the national economy

It will become a new growth point for high-quality development of China's national economy in the 21st century

• China has 689 general aviation enterprises, with 3,173 registered general aviation aircraft and 451 general airports. In 2023, there were 1.357 million hours of operational flights, with an average annual growth rate of over 12% in the past three years.

• There are approximately 2,000 drone design and manufacturing units, over 20,000 operating enterprises, and more than 1.3 million domestically registered drones, with 23.11 million hours of flight time.

• In 2023, the scale of China's low-altitude economy reached 500 billion yuan, and it is expected to exceed 2 trillion yuan by 2030.

Global Low-Altitude Economy Layout and Competition

Overall, China and the US are the most advanced in the development of the low-altitude economy. The US has accumulated rich aviation experience through its vast general aviation industry and affiliated sectors, particularly holding significant advantages in areas such as route planning and aircraft design. China shares the same advantages as the US in the fields of general aviation and unmanned aerial vehicles (UAVs). Meanwhile, China has a late-mover advantage in developing the low-altitude economy, enabling it to rapidly expand infrastructure tailored to the characteristics of low-altitude flight.

Current Status of Domestic Low-Altitude Economy Development

• Against the backdrop of new quality productive forces, the central government's top-level design and relevant policies are vigorously promoting airspace reform, with the continuous emergence of new aircraft, and strategic emerging industries boosting new domestic demand momentum.

• The concept of the domestic low-altitude economy is not a recent one. As early as 2010, the central government had already proactively planned reforms for China's low-altitude industry and airspace. After 2022, the pace of policy introduction significantly accelerated, with the synergy of basic research, product implementation, and policy guidance providing fertile ground for the implementation and rapid development of the low-altitude industry.

National Airspace Management Pilots Are Advancing in an Orderly Manner, with the Scope of Pilots Expected to Expand Further in the Future

• The reform process of airspace management directly impacts the prosperity and development of the low-altitude economy. In December 2023, the National Air Traffic Control Commission organized the formulation of the "National Airspace Basic Classification Method," adding Class G airspace below a true altitude of 300 meters and Class W airspace below a true altitude of 120 meters, providing legal low-altitude airspace for eVTOLs, light and small UAVs, and general aviation. In November 2024, the Central Air Traffic Control Commission announced the launch of eVTOL pilots in six cities: Hefei, Hangzhou, Shenzhen, Suzhou, Chengdu, and Chongqing.

• The pilot documents include relevant planning for routes and regions, with some local governments authorized for airspace below 600 meters. The first batch of pilot provinces and cities for the low-altitude economy possess obvious advantages in terms of geographical location, natural conditions, economic foundation, industrial support, and policy environment, providing strong support and guarantees for the development of the low-altitude economy.

• In the future, with the further improvement of policies and the continuous growth of the market, these regions are expected to achieve more significant results in the low-altitude economy. It is anticipated that the second batch of pilot cities will be announced soon, and the utilization rate of domestic low-altitude airspace is expected to improve.

Speech Topic: EVK High-Performance Flat Wire Propeller Drive Motor Technology

Guest Speaker: Cao Hongfei, Co-founder/General Manager of Anhui EVK Motor Technology Co., Ltd.

1 Characteristics of Motors for Low-Altitude Aircraft Powertrains

► Classification of eVTOL Powertrains:

• Pure Rotor: Single-layer rotor, upper and lower dual-layer rotors;

• Compound Wing;

• Tilt-Rotor Compound Wing.

►Electric Propeller System

Summary:

1. There are various forms of power systems, and none can be said to be an inevitable trend at present.

2. Lifting propeller motors are basically external rotor motors; channel motors are generally internal rotor motors.

3. The motor and propeller system are directly integrated, and there is no precedent for integrating the motor and electronic control system.

1 Load Characteristics and Technical Requirements of Propeller Motors for Low-Altitude Aircraft

►Technical Requirements and Characteristics of Propeller Motors:

a. According to the load characteristics of the propeller, there is no requirement for constant power field weakening of the drive motor, and whether it has a reluctance torque ratio is meaningless.

b. The motor speed range is narrow; generally, the maximum speed is within 1.4 times the rated speed.

c. Due to the strength of the propeller blades and the requirement that their linear speed must be lower than the speed of sound, the operating speed of the drive motor is relatively low.

d. The drive motor for low-altitude aircraft is generally directly connected to the propeller, which can improve the reliability of the system. At the same time, a drive motor with a relatively short axial dimension is generally selected.

e. On the premise that the controller frequency of the motor is controllable, increasing the number of pole pairs of the motor as much as possible can effectively reduce the thickness of the stator and rotor yokes and the end size of the motor windings. Combined with the relatively low operating speed, the motor generally has a relatively large number of pole pairs, and a permanent magnet concentrated winding scheme is generally chosen.

f. Given the high reliability requirements of propeller motors (especially for manned models), the design of related powertrains generally prioritizes reducing the failure rate or providing redundant functions.

》EVK High-Performance Flat Wire Propeller Drive Motor Technology [Electric Drive System Conference]

Speech Topic: Research on Electric Propulsion Systems for Powered Lift Aircraft

Guest Speaker: Gao Jie, Associate Professor, Ph.D., Research Laboratory for Safety and Airworthiness Technology of Electric Propulsion Systems, Civil Aviation University of China

Technical Characteristics of Electric Propulsion Systems

►Main Types of Key Technologies for Electric Propulsion Systems

Axial flux motor vs. radial flux motor; internal rotor vs. external rotor; direct drive vs. gearbox drive; air cooling vs. liquid cooling vs. hybrid cooling; propeller: variable pitch, reversible pitch, feathering, etc.

►Research Starting Points

Analysis of Existing Regulations Domestic and Overseas

A brief analysis of regulations for electric propulsion systems, including FAA: Type Certification - Powered Lift, EASA, EHPS Certification Guidelines, Type Certificate-Pipistrel E-811, Type Certificate-Safran ENGINeUS100B1, and Special Conditions by the Civil Aviation Administration, etc.

It also elaborated on the construction of group standards.

General Requirements for Electric Propulsion Systems

Conformity Verification

XX.3327 Overspeed

(a) As defined in paragraph (g)(2) of clause XX.3375, rotor overspeed must not result in rotor burst, deformation, or damage that could lead to hazardous electric motor consequences. Compliance with the requirements of this clause must be demonstrated through testing, valid analysis, or a combination of both. The applicable set speed for overspeed must be declared and its rationale explained.

(b) The rotor must possess sufficient strength and have an adequate burst margin under conditions exceeding the certified operating conditions and failure conditions that could lead to rotor overspeed. The burst margin must be demonstrated through testing, valid analysis, or a combination of both.

(c) The electric motor must not exceed the speed limit that could affect the structural integrity of the rotor.

XX.3519 Durability

Original text of the clause: The design and construction of each part of the propeller must minimize the occurrence of any unsafe conditions in the propeller between overhaul periods.

Clause analysis: From the aspects of design, manufacturing, testing, use, and maintenance, it must be ensured that each part of the propeller will not experience failures affecting propeller safety during its overhaul period, guaranteeing the propeller's ability to operate safely between overhaul cycles. The key points can be broken down as follows:

a) Design: Involves material selection considering the propeller's operating environment, stress levels, and the selection of materials for propeller components. It also involves structural, strength, stiffness, deformation, and fatigue performance. Fatigue tests must be designed to ensure that no fatigue-induced failures occur in the propeller between overhaul intervals, and the overhaul interval must be determined.

b) Testing and analysis: Conduct static tests, fatigue tests, durability tests, functional tests, and other tests (such as bird strike, lightning strike, over-rotation and over-torque, propeller control system components, hydraulic components, etc.) and analyze the results.

c) Use and maintenance: Use and maintain the propeller in accordance with the manual's requirements.

Factory Tour (Limited Capacity) – Hunan Hongwang New Material Technology Co., Ltd.

Park Tour – Louxing Industrial Development Zone – National-Level Loudi Economic Development Zone

Launch Event

Networking

On-Site Highlights

》Click to View More Exciting Moments

With this,the 2025 SMM (4th) Electric Drive Systems Conference & Drive Motor Industry Forumhas successfully concluded!

Thank you for your attention and support for this summit. Let's meet again next year!

》Click to view the special report on the 2025 SMM (4th) Electric Drive System Conference & Drive Motor Industry Forum