June 16, 2025

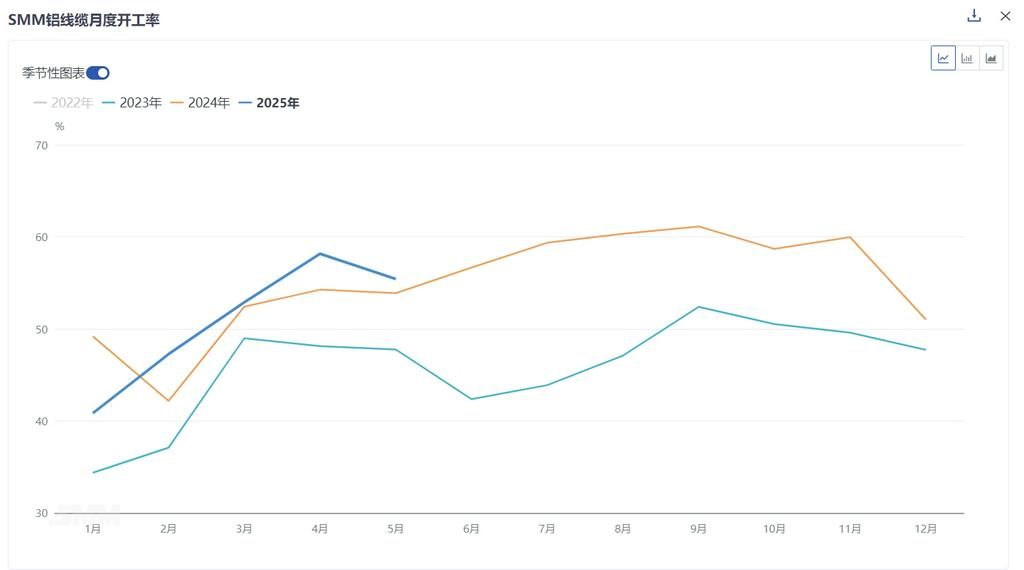

According to SMM statistics, the comprehensive operating rate of China's aluminum wire and cable industry reached 55.42% in May 2025, down 2.75% MoM from April, indicating a slight overall decline, but up 1.16% YoY from April last year. By enterprise size, the operating rate of large enterprises decreased 2.59% MoM to 70.98%, medium-sized enterprises fell 2.29% MoM to 48.92%, and small enterprises dropped 6.78% MoM to 27.12%.

Enterprise-wise, early June saw a divergence in industry operating rates. Leading enterprises, supported by rational production scheduling based on orders on hand, demonstrated strong resilience despite MoM declines, maintaining relatively high levels. In contrast, small and medium-sized enterprises showed marked weakness due to the end of intensive delivery cycles and dampened production sentiment amid rebounding aluminum raw material prices. Raw material inventory side, post-peak delivery periods led to reduced procurement enthusiasm and slower inventory digestion. Finished product inventory side, pressure remained relatively small despite nearing the end of prior order deliveries.

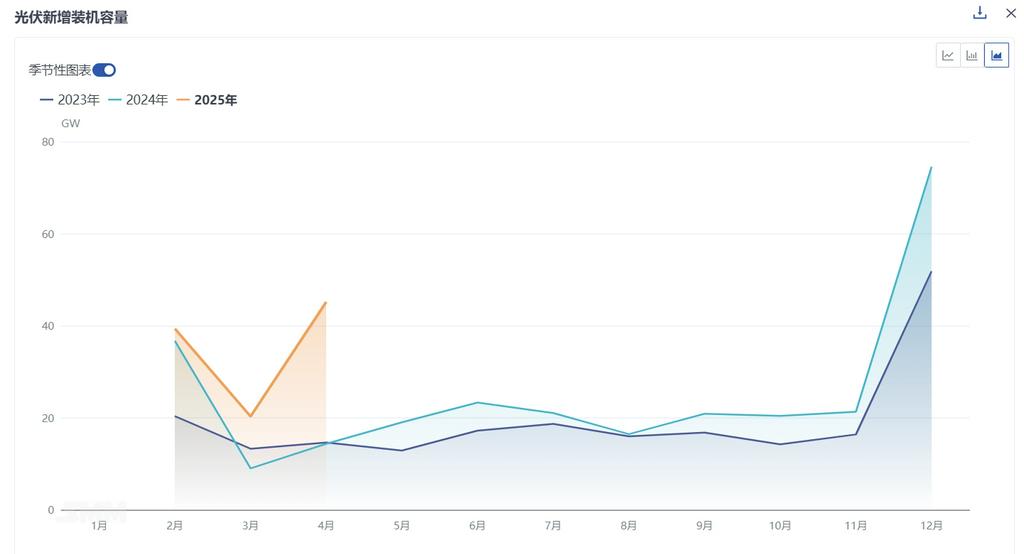

Order perspective, State Grid recently launched the third batch of power transmission and transformation tenders, releasing 128,000 mt of aluminum-core conductor and ground wire orders with delivery periods spanning August 2025-March 2026. Provincial grid distribution network framework agreements also continued to release orders, providing stable demand expectations for H2. However, the current market is in a transitional gap between concluding prior deliveries and awaiting large-scale new order implementations, exhibiting divergent weakness. While some State Grid orders remain in delivery, demand for overhead lines and PV new orders declined in certain provinces, failing to strongly boost immediate production. The first batch of UHV and third batch of transmission orders will enter delivery phases from August 2025, concluding around March 2026, forming medium and long-term order continuity based on existing backlogs. Other orders side, despite a PV installation rush during January-April with 45.2GW new installations (up 122% MoM) boosting aluminum alloy cable consumption, vigilance is warranted regarding potential order impacts post the "531" policy period as installation momentum may weaken.

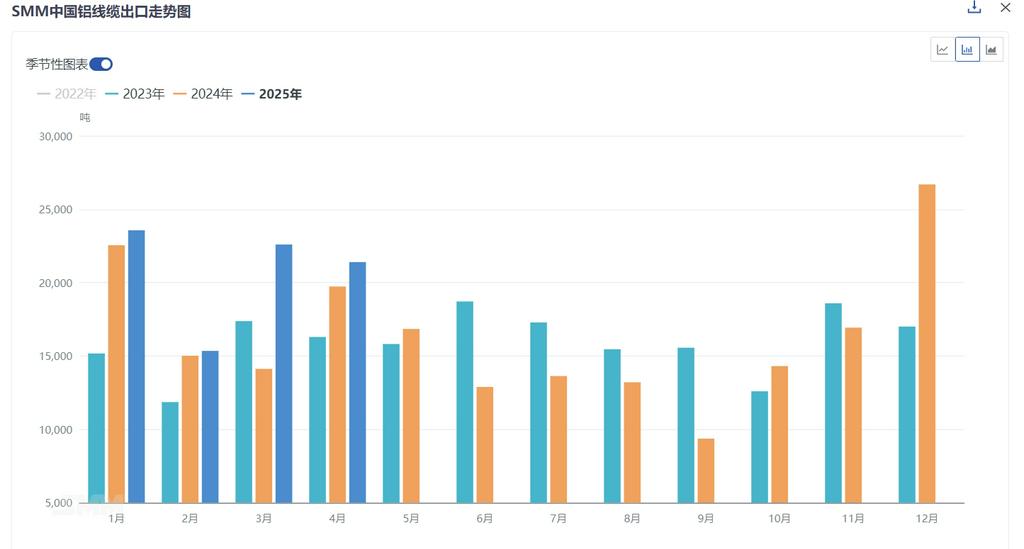

Exports side, customs data showed China's aluminum wire and cable exports reached 21,300 mt in April 2025, down 5.3% MoM but up 8.43% YoY. Cumulative January-April exports totaled 82,800 mt, a 16.08% increase from 71,400 mt during the same 2024 period. By product structure, steel-core aluminum stranded wire accounted for 72.7% (15,500 mt), while aluminum stranded wire represented only 27.3% (5,800 mt). Exports remained high, reflecting the continued resilience in overseas power grid renovation demand. However, export orders related to new energy infrastructure and other sectors showed some weakness.

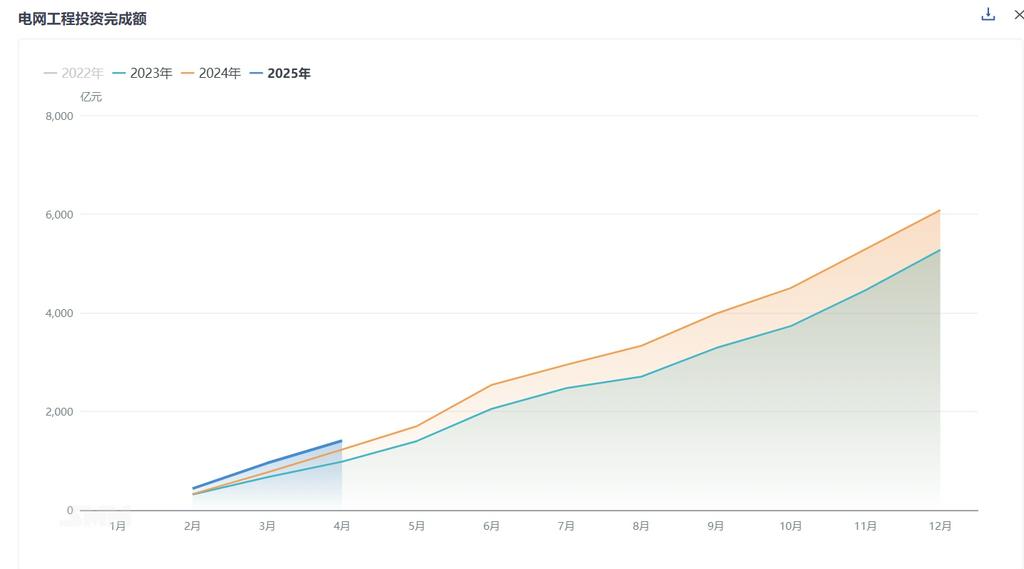

According to statistics from the National Energy Administration, in April, the investment completed in power grid projects reached 46.3 billion yuan, up 47% YoY and 5% MoM. From January to April, the total investment completed in power grid projects was 122.9 billion yuan, up 25% YoY. SMM believes that the operating rate of the aluminum wire and cable industry is expected to remain in the doldrums in the short term. The industry is currently undergoing an adjustment phase following the conclusion of the previous concentrated delivery period. Leading enterprises are able to sustain production due to the resilience of their orders, but small and medium-sized enterprises are under significant pressure. Market attention is focused on the timing of the next concentrated delivery cycle and whether orders in segments such as PV, wind power, automotive wiring harnesses, and infrastructure will recover. With the gradual implementation and execution of State Grid tender orders in H2, the industry's operating rate is expected to regain upward support, but in the short term, it is anticipated to exhibit a range-bound trend.