》Check SMM aluminum product quotes, data, and market analysis

》Subscribe to view historical spot prices of SMM metals

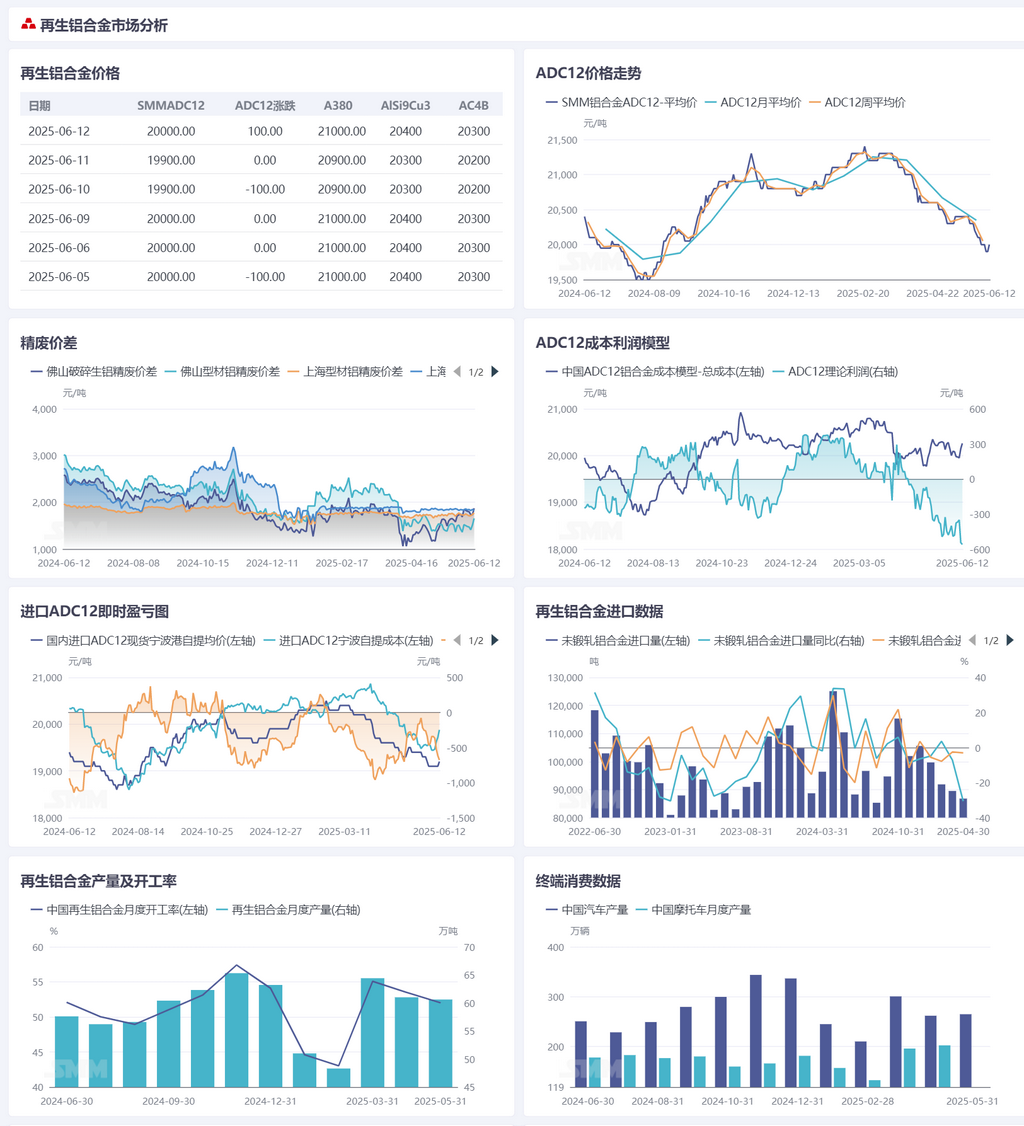

Secondary Aluminum Raw Materials:

This week, the domestic aluminum scrap market in China continued to fluctuate at highs. Spot primary aluminum prices first declined and then rose. As of June 12, SMM A00 aluminum ingot prices closed at 20,650 yuan/mt, a significant increase of 400 yuan/mt from last Thursday. Aluminum scrap prices generally followed the upward trend, but there was significant differentiation among varieties: the supply of aluminum tense scrap remained tight, with quotes for shredded aluminum tense scrap rising from 15,500-17,000 yuan/mt to 15,900-17,400 yuan/mt (tax excluded), providing solid support. Wrought aluminum alloy scrap, such as baled UBC, slightly increased from 15,000-15,500 yuan/mt to 15,150-15,650 yuan/mt (tax excluded). Although influenced by primary aluminum, regional price differences widened. East China (Shanghai, Jiangsu, Shandong) closely tracked aluminum prices, with daily adjustments as high as 200-250 yuan/mt, while price adjustments in South China (Jiangxi, Foshan) were delayed, with adjustments of only 100-150 yuan/mt. The price difference between A00 aluminum and aluminum scrap fluctuated rangebound. The price spread between mechanical casting aluminum scrap and A00 aluminum in Shanghai narrowed to 1,826 yuan/mt, while the price spread between aluminum extrusion scrap and A00 aluminum in Foshan widened to 1,655 yuan/mt. Affected by the off-season, downstream secondary aluminum enterprises faced weak order releases, with purchases mainly driven by immediate needs. Operating rates remained low, as cost pressure continued to compete with weak end-use demand. It is expected that the aluminum scrap market will continue to fluctuate at highs. The tight supply of aluminum tense scrap is unlikely to change, providing solid price support. Wrought aluminum alloy scrap will continue to fluctuate rangebound with primary aluminum, but the risk of a high-level correction in primary aluminum, combined with weak off-season demand, may suppress upside room. The operating rates of downstream secondary aluminum enterprises may remain low, with an ongoing struggle between costs and orders. In addition, after the listing of cast aluminum alloy futures, arbitrage activities may temporarily boost market activity, increasing the price sensitivity of aluminum scrap, a core raw material. Short-term volatility risks should be monitored.

Secondary Aluminum Alloy:

This week, aluminum prices held up well, but the price increase of secondary aluminum alloy remained sluggish. As of June 12, SMM ADC12 prices remained unchanged from last week, trading within the range of 19,900-20,100 yuan/mt. On the cost side, aluminum scrap prices closely followed the upward trend of aluminum prices, leading to a continuous rise in the production costs of secondary aluminum alloy and an expanding theoretical loss in the industry, exacerbating cost-side pressure. Demand remained weak, with low purchase willingness from downstream buyers. In terms of social inventory, on June 12, the social inventory of secondary aluminum alloy ingots in major domestic consumption areas was 18,013 mt, an increase of 1,647 mt from last Thursday, with the inventory buildup trend continuing. In terms of imports, overseas ADC12 quotes increased by 40 USD/mt from last week to 2,410-2,450 USD/mt this week. Domestic import spot prices rose by 100 yuan/mt to 19,100-19,300 yuan/mt. Due to the higher increase in overseas prices compared to the domestic market, the immediate loss from imports expanded again to 500-700 yuan/mt from last week. On Tuesday (June 10) this week, futures for cast aluminum alloy were officially listed for trading on the SHFE. Driven by the need to narrow the spot-futures price spread, as the listing benchmark price of 18,365 yuan/mt was significantly lower than the spot price, the main futures contract surged strongly at the opening bell, with prices gradually climbing to around 19,500 yuan/mt over the next two days. In the early stages of futures listing, market sentiment was characterized by a wait-and-see approach, with most participants still in the phase of waiting for trading opportunities. Overall, the current traditional off-season characteristics are prominent, with persistent weakness on the demand side constraining the upside room for ADC12 prices. However, the rapid increase in raw material prices on the cost side has provided support. It is expected that ADC12 prices will mainly undergo narrow adjustments in the short term, and the discount pattern relative to A00 will continue.