On June 4th, the ASEAN Tin Industry Conference 2025, part of Indonesia Critical Minerals Conference & Expo 2025, hosted by SMM Information & Technology Co., Ltd. (SMM), supported by the Indonesian Ministry of Foreign Affairs as a government supporter, and co-organized by the Association of Indonesia Nickel Miners (APNI), the Jakarta Futures Exchange, and Sxcoal, successfully concluded in Jakarta, Indonesia! The conference brought together industry leaders, experts, scholars, and enterprise representatives from around the globe. In-depth discussions were held on core topics such as the development trends of China's tin market, the future development of Indonesia's tin industry policies, achieving sustainable development through innovation - Arsari Tambang's vision for the future of the green critical minerals industry, the role of the futures market in enhancing the resilience of the tin supply chain, trading pure tin bars through futures exchanges, trade, tariffs, taxes, and restrictions - strategic metals and the new reality, risks and responses in the tin commodity market amid economic restructuring, the role and value of the entire industry chain of tin ingots from resources to market, analysis and judgment of China's tin price trends, the role of Southeast Asia's tin industry in the "Belt and Road" Initiative, analysis of the current situation and development prospects of Africa's tin ore market, analysis of the current situation of tin ore supply in Myanmar and its policy impacts, and the Indian tin solder market: a game of opportunities and risks. From empowering supply chain resilience through the futures market to revolutionizing mining paradigms with spiral chute separation technology; from strategically anchoring Southeast Asia's tin industry within the "Belt and Road" framework to the game of opportunities in India's tin solder market, multidimensional wisdom is sparking, seeking new development opportunities and charting a new future for the global tin industry amid the wave of economic restructuring!

Opening Remarks

Liu Luke, Chairman of Yunnan Tin Co., Ltd.

In his remarks, Liu Luke stated that Southeast Asia, as one of the regions richest in global tin resources, holds a pivotal position in the development of the tin industry. In recent years, the strategic value of multiple Southeast Asian countries, represented by Indonesia, in the development of the tin industry has been increasing. Global upstream and downstream partners in the tin industry have continuously strengthened their cooperation with Southeast Asian countries, actively participating in the Southeast Asian market and contributing to the development of the tin industry. The joint hosting of the 2025 Southeast Asia Tin Industry Conference by JFX and SMM has built a bridge of communication for upstream and downstream enterprises in the tin industry, enabling many industry partners to deeply collaborate and integrate through this bridge, and jointly discuss the development of the tin industry. Yunnan Tin hopes to join hands with more industry peers in Southeast Asia to carry out more in-depth exchanges and cooperation in resource exploration and development, smelting and comprehensive recovery technologies, international trade, and market maintenance!

Novi Muharam, Head of Commercial Strategy at MIND ID, a state-owned mining company in Indonesia

Novi Muharam, mentioned in his speech: As a major global producer of tin resources, Indonesia has a long and distinguished history of supporting global industrial progress. In the face of industrial transformations in the new era, we urgently need to promote the extension of the tin industry from traditional mining to a high-value industry chain through deeper information sharing and partnerships. This means transforming tin resources into innovative products that align with the trends in electronic technology, artificial intelligence, and green development. Let us work together to build an innovative, responsible, and forward-looking tin industry ecosystem!

Stephanus Paulus Lumintang, CEO of the Jakarta Futures Exchange (JFX)

Today, the global tin market is undergoing rapid changes. The demand for semiconductors is growing, with widespread penetration into electronics, energy, and green technology sectors. At the same time, the market is demanding higher transparency, accountability, and Environmental, Social, and Governance (ESG) standards in procurement processes. Buyers not only need to optimize supply chain management but also align with international trends in clean production and sustainable development.

The Jakarta Futures Exchange in Indonesia consistently exceeds market expectations by understanding the needs of stakeholders. While implementing the government's strategy for the development of the downstream commodity industry, the exchange is committed to promoting market transparency and helping to build a modern and efficient tin trading system that balances efficiency and responsibility.

Guest Speeches

Keynote Speech: Development Trends of the Tin Market in China

Speaker: Zhang Chi, Deputy Manager of the Market Operations Center at Yunnan Tin Co., Ltd.

Keynote Speech: The Future Development of Indonesia's Tin Industry Policies

Speaker: Stephanus Paulus Lumintang, CEO of the Jakarta Futures Exchange

Introduction to JFX

The Jakarta Futures Exchange (JFX) is the first futures exchange in Indonesia. Established on August 19, 1999, its foundation aims to bring significant benefits to the business community and serve as a hedging tool. The primary role of JFX is to provide facilities for its members to trade futures contracts at set prices through effective interactions based on supply and demand within an electronic trading system. JFX was established based on Law No. 32 of 1997 on Commodity Futures Trading. JFX is committed to providing the best solutions and services for the futures trading industry (PBK). The process of converting and utilizing the latest information technologies has been optimized to respond to market demands and the dynamic business environment. JFX consistently innovates, develops products, enhances the capabilities and competencies of all functions and areas within the organization, and provides commodity trading infrastructure on an international scale. JFX is honored to be part of the system driving transactions in the domestic and global commodity industries.

Outlook for Indonesia's Tin Industry Policy

►Current Policies: Restrictions on raw tin exports to encourage domestic smelting; licensing and supervision from government agencies; environmental and community impact assessments required for operational activities.

►Drivers for Policy Change: Economic diversification and downstream industrial development; environmental sustainability and global ESG standards; strengthening Indonesia's position in the global commodity market.

►Future Policy Directions: Incentives for tin refining and alloy development; expansion of strategic reserves and the listing of futures contracts; integration of digital tools to enhance transparency and efficiency.

JFX's Role in Supporting Tin Policy Formulation

Promoting the establishment of a transparent and efficient tin trading platform; collaborating with regulators and industry stakeholders; launching new tin futures contracts to support pricing and hedging.

Impact of the Tin Exchange

Keynote Speech: Innovating for Sustainability: Arsari Tambang's Vision for a Green Critical Mineral Industry Future

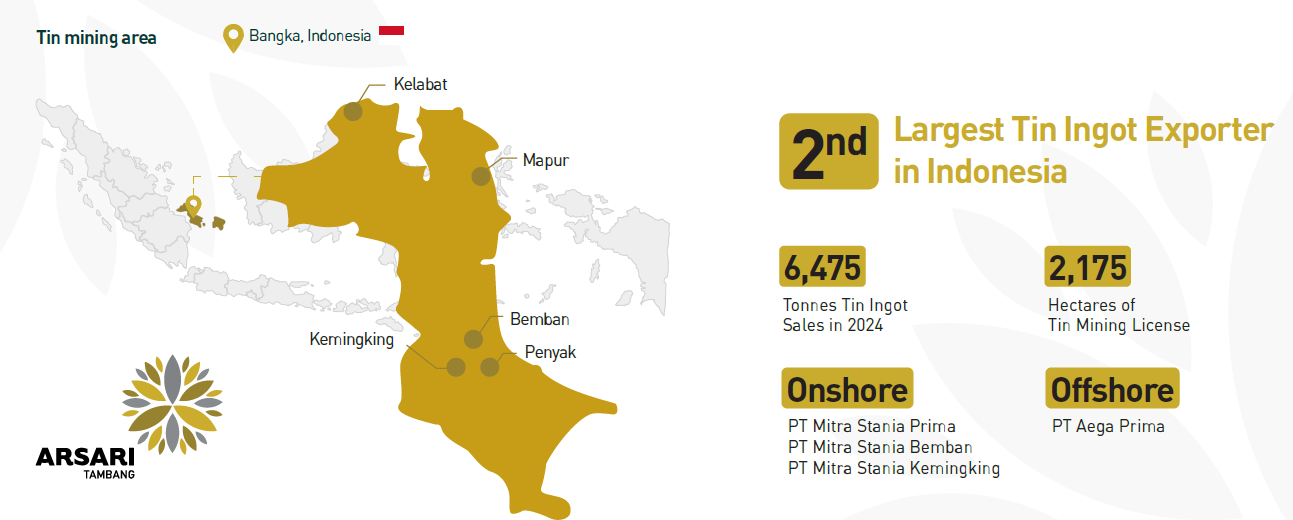

Speaker: Aryo Djojohadikusumo, CEO of PT Arsari Tambang

►The Roots of Indonesia's Tin Industry

PT Timah Tbk, established in 1976 as a state-owned enterprise (BUMN), marks a significant milestone in Indonesia's tin industry.

Arsari Tambang is Indonesia's largest private tin mining company, holding a 2,175-hectare mining concession on Bangka Island.

Arsari Tambang is an integrated tin mining company covering the entire tin production chain, from exploration, mining, smelting, refining to tin metal production, and beyond to more downstream tin products. Its tin solder production line just commenced operations in June 2025, with plans to develop tin plate products in the future.

Arsari Tambang is an end-to-end integrated tin mining company and the first private enterprise to lead post-mining ecological restoration in Bangka Belitung Province.

Arsari Tambang sells high-grade tin ingots while adhering to environmental and safety standards.

Arsari Tambang's Commitment to Sustainable Development: Embracing the Net-Zero Challenge and Promoting Community Development.

It also elaborated on the company's environmental restoration plans and provided relevant case studies.

►Arsari Tambang is Poised to Become Indonesia's First Tin Mining Company to Achieve Net-Zero Emissions

Transitioning to renewable energy (REC) electricity certified by Indonesia's state electricity company (PLN); to achieve sustainable tin ingot production, the company is shifting its fuel source to electric furnaces and utilizing renewable electricity sources such as hydropower and geothermal energy; transitioning to renewable energy-based power generation.

Carbon capture to reduce carbon emissions and increase carbon credits

Commitment to developing the downstream tin industry

Arsari Tambang is committed to developing the downstream tin industry, which is in line with the initiative of President Prabowo Subianto of the Republic of Indonesia to promote the downstream processing of natural resources for the benefit of the Indonesian people.

Global surge in downstream tin demand

It is projected that downstream tin demand will grow by approximately 25% by 2030, primarily driven by demand for solder. By 2030, the world will require an additional 61,000 mt/year of tin solder, with 17,000 mt/year coming from ASEAN countries.

Keynote Speech: The Role of the Futures Market in Enhancing the Resilience of the Tin Supply Chain

Speaker: Edric Koh, Head of Corporate Sales, Asia, London Metal Exchange

Keynote Speech: Physical trading of pure tin ingots through the Futures Exchange

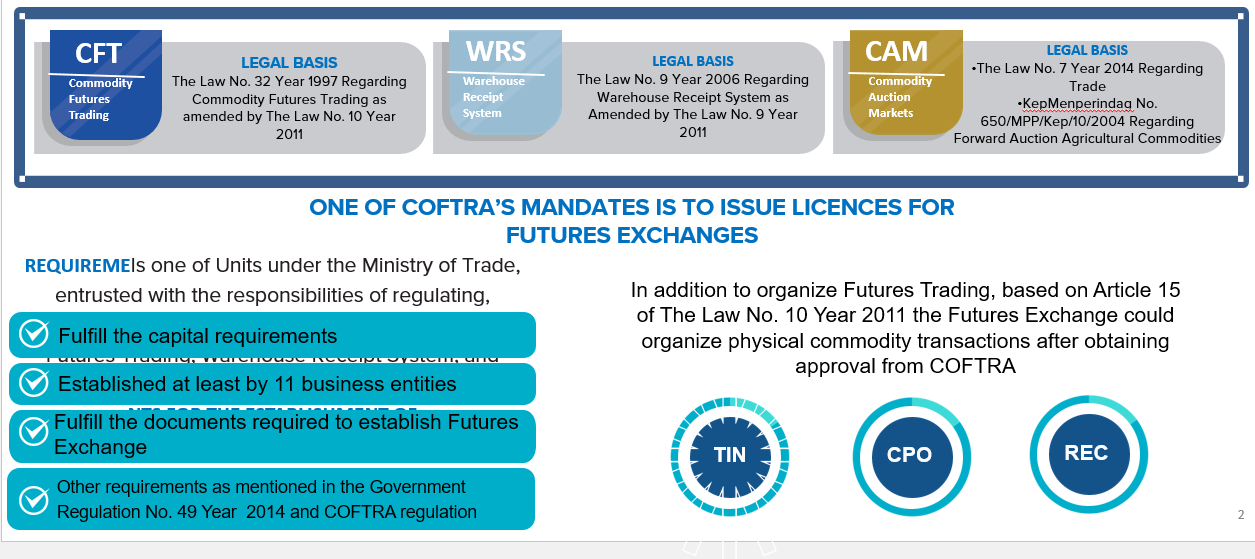

Speaker: Mrs. Ima Siti Fatimah, Director of Commodity Futures Trading Regulatory Agency (COFTRA) of Indonesia

What is COFTRA?

COFTRA is a unit under the Ministry of Trade of Indonesia, responsible for regulating, developing, supervising, and monitoring commodity futures trading, warrant systems, and commodity auction markets.

Legal Basis for Trading of Pure Tin Ingots

Constitution: Law No. 32 of 1997 on Commodity Futures Trading (as amended by Law No. 10 of 2011).

MOT Regulation: Regulation of the Minister of Trade No. 23 of 2023 on Export Policies and Regulations.

COFTRA Regulation: COFTRA (Commodity Futures Trading Regulatory Agency) Regulation No. 11 of 2019 on Technical Guidelines for Trading of Pure Tin Ingots via the Tin Exchange, as amended by COFTRA Regulation No. 6 of 2024.

Purpose of Export Regulation for Pure Tin Ingot Trade

As the world's largest tin exporter, it is significant for Indonesia to establish a national tin exchange based on the following considerations:

Sovereignty and Pricing Independence: The sovereignty and independence to determine domestic tin prices autonomously.

Resource Conservation and Utilization: Ensuring and utilizing limited mineral resources to protect natural resource development, environmental sustainability, and sustainable economic development.

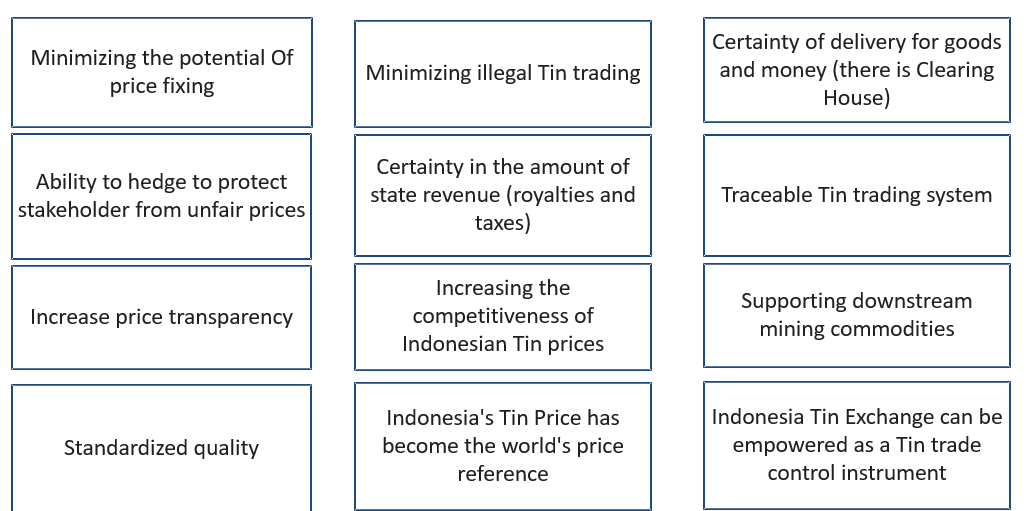

Benefits of Tin Trading on the Futures Exchange

Principles of Tin Trading on the Exchange

Trading on the exchange adheres to the principles of "free and fair trade," which specifically include:

Clarity and Transparency:Integrity in Trading: Ensuring honest and fraud-free tin trading processes, eliminating improper practices such as fraud and market manipulation, and safeguarding the legitimate rights and interests of all trading parties.

Transparency:Information Disclosure: Publicly release information related to export taxes, royalties, and foreign exchange to ensure traceable and supervised transaction data, enhancing market trust.

Price Discovery:Transparent and Traceable Pricing Mechanism: Establish tin prices through open bidding to ensure a transparent price formation process with traceable accountability, providing the market with price signals that genuinely reflect the supply-demand relationship.

Bargaining Power:Strengthening Seller Market Influence: By aggregating multiple buyers, create a seller-dominated market structure to enhance the bargaining power of tin suppliers in transactions, avoiding low-price competition.

Price Reference:International Price Benchmark: The prices formed on the exchange can serve as a key reference for global tin prices, boosting Indonesia's pricing influence in the international tin market.

Good Corporate Governance:Healthy and Sustainable Business Practices: Require trading participants to adhere to high governance standards, promoting sustainable development in the tin industry across environmental, social, and governance (ESG) dimensions while mitigating systemic risks.

Pure Tin Ingot Contract

Pure tin ingots fall under the commodity tariff code / HS code 8001.10.00.

Keynote Speech: Trade, Tariffs, Taxes and Restrictions-Strategic Metals and the New Reality

Speaker: Joseph G. Miller Esq., Strategic and Defense Metals Expert at Intra-Pax LLC

Competition for Strategic Metals

Trade restrictions and tariff measures have evolved over several years, with more metals and products subsequently included (in the scope of taxation).

It covered restrictions on rare earths, chip metals, and other related topics.

Dual-Use Metal Restrictions

Dual-Use Nature: Applicable for both commercial/civilian and military/defense purposes

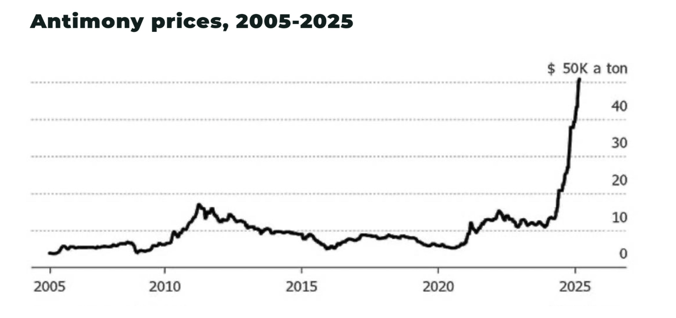

Most metals are used in both categories—some have more specific defense applications, such as antimony, tellurium, rare earths, tungsten, bismuth, indium, molybdenum...

Antimony:Export restrictions implemented in September 2024, a typical "dual-use" metal: 40% used in solar panel glass clarification, antimony trioxide—flame retardant, and for hardening lead in bullets.

Other Metals Subject to Restrictions in 2025

• Tungsten

• Indium, Tellurium, Bismuth, Molybdenum

Keynote Speech: Tin Commodity Market and Countermeasure in Economic Restructuring

Speaker: Wei Sang, Senior Manager of Tin Commodity Department, Minmetals Nonferrous Metals Co., Ltd.

Keynote Speech: From Resources to Market: The Role and Value of the Entire Industry Chain of Tin Ingot

Speaker: Jinqiu Tai, General Manager of Honghe Prefecture Jucheng Industrial Co., Ltd.

2024: Global Refined Tin Capacity

Currently, the global refined tin capacity distribution shows a highly concentrated pattern. The Asian region dominates the global refined tin capacity landscape, with China and Indonesia together accounting for over 65% of the world's total refined tin capacity. Global refined tin production in 2024 was 37.2 mt, a decrease of approximately 10,000 mt from 2023. China's total refined tin production in 2024 was 219,000 mt, accounting for 52% of the global total, up 7.4% YoY.

As the core region of China's refined tin industry, Yunnan accounts for over 57.66% of the country's refined tin production.

It also provides an introduction to the major importing and exporting countries of refined tin.

Challenges and Pain Points

Unstable Trade Policies and Tariff Barriers: 1. Frequent policy adjustments, 2. Risk of trade friction.

Volatile Market Prices: 1. Supply-demand imbalance, 2. Influence of financial attributes, 3. Cost transfer pressure.

Logistics and Transportation Complexity: 1. Challenges in multimodal transportation, 2. Special transportation requirements, 3. Disruptions from geopolitical conflicts.

Stabilizing Raw Material Supply

It elaborates on the shares of mine production and refined production in various countries in 2024 as a proportion of the global total.

Improving Raw Material Quality

Advanced Mining and Beneficiation Technologies to Enhance Tin Ore Grade: Through a combined gravity separation-flotation process, the grade of tin ore can be increased from 0.5%-1.5% in primary ore to 60%-70% in concentrates, significantly reducing smelting energy consumption and impurity content. High-quality tin ore can produce higher-quality tin ingots, meeting the quality requirements of the high-end market for tin ingots, enhancing competitiveness in the international tin ingot trade, and fetching higher trade prices.

Enhancing Tin Ingot Quality

Smart Logistics and Warehousing Inject Vitality into Tin Ingot Trade

►Shortening the Tin Ingot Circulation Cycle and Optimizing Logistics Routes

Intelligent Warehouse Management: Real-time tracking of tin ingot location, inventory quantity, and status, with automated handling of inbound and outbound processes, reducing labour-intensive operations and increasing inventory counting efficiency by over 80%. Automatically planning the optimal delivery routes based on tin ingot transportation requirements (such as weight, transportation distance, and timeliness requirements), avoiding circuitous transportation. Taking long-distance transportation as an example, intelligent dispatching can reduce transportation time costs by 15%-20%.

►Cost Control: Reducing Operating Expenses Across the Entire Supply Chain

Reducing Warehousing Costs: Three-dimensional warehouses and automated shelving increase space utilization, with storage capacity per unit area increasing by 3-5 times compared to traditional warehouses, reducing rental expenses. Automated equipment (such as smart forklifts) replaces manual operations, reducing labour requirements in warehousing by over 50%, while also reducing loss costs caused by human errors (such as tin ingot bumps and handling mistakes).

► Precision Management: Enhancing Supply Chain Controllability

Full-Process Visual Traceability: Combining blockchain technology with the Internet of Things (IoT) to generate a unique "digital identity" for each batch of tin ingots, recording full-process data from production and warehousing, logistics and transportation, to delivery. Leveraging IoT technology to enable real-time monitoring of the location and status of tin ingots during transportation, allowing customers and traders to access cargo information at any time, enhancing trade trust, and reducing trade disputes.

The Role of Solder Manufacturers in Promoting Tin Ingot Trade Across the Entire Industry Chain

► I. Demand Side: Directly Boosting Tin Ingot Consumption

► II. Industry Chain Synergy: Stabilizing Tin Ingot Circulation

Upstream integration ensures the stability of tin ingot supply and reduces the risk of market price fluctuations.

Inventory Adjustment.

► III. Technological Upgrades Driving High-Value-Added Trade

Demand for High-Purity Tin: Lead-free solders (e.g., Sn-Ag-Cu alloys) require higher purity levels (≥99.9%) for tin ingots, driving premium trading of high-grade tin ingots and the development of niche markets.

Recycled Tin Utilization: Increased procurement of recycled tin (e.g., tin recovered from waste PCBs) by solder manufacturers promotes the improvement of the recycled tin trade chain, partially substituting the demand for primary tin ingots.

► IV. Price Transmission and Financialization

Pricing Influence: The concentrated procurement behavior of solder manufacturers may serve as a reference for spot prices of tin ingots, particularly in regional markets (e.g., South China market).

Keynote Speech: Analysis and Forecast of Tin Prices in China

Speaker: Peng Chen, Senior Tin Analyst, SMM

1. Global Distribution of Tin Resources and Supply Landscape

Intensified Resource Scarcity: Static mining lifespan of less than 15 years

China accounts for 22% of global tin ore reserves but contributes 45% of global production, with resource development intensity exceeding critical thresholds.

• Global tin resources are highly concentrated, with China, Indonesia, and Myanmar collectively accounting for over 50%. China, as the largest producer (45% of production), and Indonesia form a dual-core driving force, but with significant differences in resource endowments.

Tin Ore Segment: Global tin ore production is also primarily concentrated in countries with high reserves

• Global tin ore production is mainly concentrated in countries such as China, Indonesia, Myanmar, and the DRC.

• Except during the COVID-19 pandemic, global tin ore production has consistently maintained a level of 300,000 mt in metal content.

Tin Ore Segment: Tin ore imports continued to decline in 2025, with cumulative imports for January-April 2025 down 47.98% YoY. The contraction in tin ore supply from Myanmar has become a long-term trend.

• The market generally expects Wa State to resume production by mid-2025, but the initial increase will not exceed 10,000 mt in metal content, and a 2-3 month transmission period is required. The progress of production resumption will be constrained by Sino-Myanmar mine trade negotiations and the centralization process in Wa State.

Tin Ore Segment: Myanmar's dominance is weakening, and a diversified pattern is accelerating its formation.

• Before 2023: Myanmar accounted for 72%-85% of China's tin ore imports. However, after the implementation of the mine ban policy in Wa State in August 2023, its supply plummeted. By 2024, Myanmar's import share dropped to 48.1%, and further declined to 24%-30% in 2025. The core mining area, Mansang (accounting for 80% of Myanmar's supply), remains shut down.

• Emergence of alternative sources: Imports from Africa (DRC, Nigeria), South America (Peru, Bolivia), and Australia have increased significantly. For example, the DRC's share of China's imports rose to 28% in 2025, Nigeria's share reached 11%, and imports from Australia surged by 101% YoY. The 20-day moving average of recent tin ore import profit margins has stabilized.

►Risk Points Highlighted:

Stability of African supply chain to be verified: Operational risks at Alphamin mine in the DRC (short-term shutdown in April 2025).

The global refined tin landscape features "Asia as the dominant player, South America as a supporter, and Africa as a supplement."

• In the global tin industry chain, smelting and refining operations are mostly concentrated near tin ore production sites. Countries such as China, Indonesia, Malaysia, Peru, Thailand, DRC, Bolivia, and Brazil all have smelters of a certain scale, with China and Indonesia accounting for a relatively high proportion.

The current production resumption process in Wa State, Myanmar, has commenced, but actual increases may fall short of expectations due to the impact of earthquakes and rising policy implementation costs.

The core contradiction in the DRC's tin ore event chain lies in the game between geopolitical conflicts and resource dependence.

Risk Points:

Stability of African supply chain to be verified: As the largest importer, China's refined tin industry chain is significantly affected by disruptions in the DRC, while demand growth in AI, new energy, and other sectors further exacerbates the supply-demand imbalance.

2. Evolution of Global Tin Consumption Structure and Demand

Terminal Segment: Overview of tin consumption structure

• In the global tin consumption structure, tin solder accounts for 48%, tin chemicals 16%, lead-acid batteries 7%, and tin alloys 7%.

• In China's tin consumption structure, tin solder accounts for 67%, tin chemicals account for 12%, lead-acid batteries account for 7%, lead-acid batteries account for 7%, and tinplate accounts for 6%.

Terminal sector: The Philadelphia Semiconductor Index (SOX) shows a significant negative correlation with the real yield of 10-year US Treasury bonds. AI demand has driven the capacity utilisation rate of semiconductor companies to an all-time high.

• In the past two years, the Philadelphia Semiconductor Index (SOX) has shown a significant negative correlation with the real yield of 10-year US Treasury bonds, primarily driven by liquidity expectations and valuation pressures.

• In 2024, the capacity utilisation rate of the US computer and semiconductor sectors remained stable at 76.53%-78.44%, close to the average over the past 10 years (76.72%). In specific segments, the capacity utilisation rate of the semiconductor sector reached 95% in Q1 2025, an all-time high, reflecting supply-demand tightness driven by AI demand.

Panel Discussion: The Role of Southeast Asia's Tin Industry in the Belt and Road Initiative

Moderator: Sang Wei, Senior Manager of the Tin Commodity Department, Minmetals Nonferrous Metals Co., Ltd.

Panelists: Stephanus Paulus Lumintang, CEO of Jakarta Futures Exchange

Yue Min, CFO of Yunnan Tin Co., Ltd.

Chrispin Andereas, Head of Business Development, Tunas Property Group

Novi Muharam, Head of Commercial Strategy, MIND ID (Indonesia's State-Owned Mining Company)

Mamoko Egyu, Smelting Expert, Coordination and Mining Planning Technical Department (CTCPM), Ministry of Mines, DRC

Keynote Speech: Analysis of the Current Situation and Development Prospects of the African Tin Mine Market

Speaker: Mamoko Egyu, Smelting Expert, Technical Mining Coordination and Planning Unit, DRC

Geology and Mineralogy

► Geology

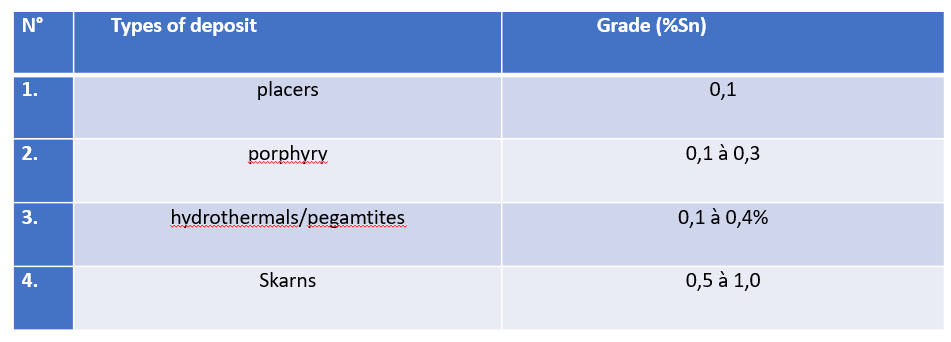

It elaborates on the types of tin deposits worldwide:

Famous tin deposits in Africa include:

Pegmatite-type deposits: Manono (DRC), Bikita (Zimbabwe), and Uis (Namibia);

Vein-type deposits: Jos (Nigeria);

► Placer deposits: Maniema, North Kivu (Bisié), and South Kivu (DRC).

In placer deposits, cassiterite is concentrated by gravity, often associated with tungsten (wolframite) and other common heavy minerals (tantalite).

► Mineralogy

In nature, tin primarily exists in the form of **cassiterite (SnO₂)**. Other minerals are of lower economic significance, ranked as follows:

Cassiterite (SnO₂): tin content of 78.7%; Teallite (PbSnS₂): 30%; Stannite (Cu₂FeSnS₄): 27.6%; Cylindrite (Pb₃Sn₄Sb₂S₁₄): 24.8%, etc.

Tin Industry and Its By-products

Currently known mineral resources: Cassiterite: 80 million mt, Tantalum-niobium ore: 30 million mt, Tungsten ore: 4 million mt.

2024 Production: Cassiterite: 43,000 mt, Tantalum-niobium ore: 2,900 mt, Tungsten ore: 337 mt.

DRC Mineral Statistics, 2024

2024 Tin Ore Industrial Exports (in mt)

It also elaborates on the 2024 artisanal cassiterite exports by province in the DRC, the 2024 artisanal tin concentrate exports by province in the DRC, the total 2024 cassiterite exports, the total 2024 artisanal tantalum-niobium ore exports, the distribution of 2024 artisanal tantalum-niobium ore exports, the 2024 tungsten ore exports, the 2024 artisanal tungsten ore exports, etc.

Changes in Tin Ore Exports from 2020 to 2024 (in mt)

Keynote Speech: Analysis of the Current Situation of Tin Ore Supply in Myanmar and Its Policy Impact

Speaker: Li Mingfu, Director of Gejiu Qiandao Metal Co., Ltd.

Global Distribution of Tin Ore Resources

Overview of Global Tin Ore Reserves and Production

According to USGS, global tin reserves in 2024 were 5.254 million mt, with the top five reserve-holding countries being China (19%), Indonesia (15.23%), Myanmar (13.32%), Australia (11.8%), Russia (8.76%), and Brazil (7.99%).

In terms of production, China (71,000 mt), Indonesia (52,500 mt), Myanmar (24,000 mt), Peru (33,000 mt), and the DRC (26,000 mt) accounted for a combined 71.64% of the total production of the top five producing countries.

Distribution of Tin Ore Resources

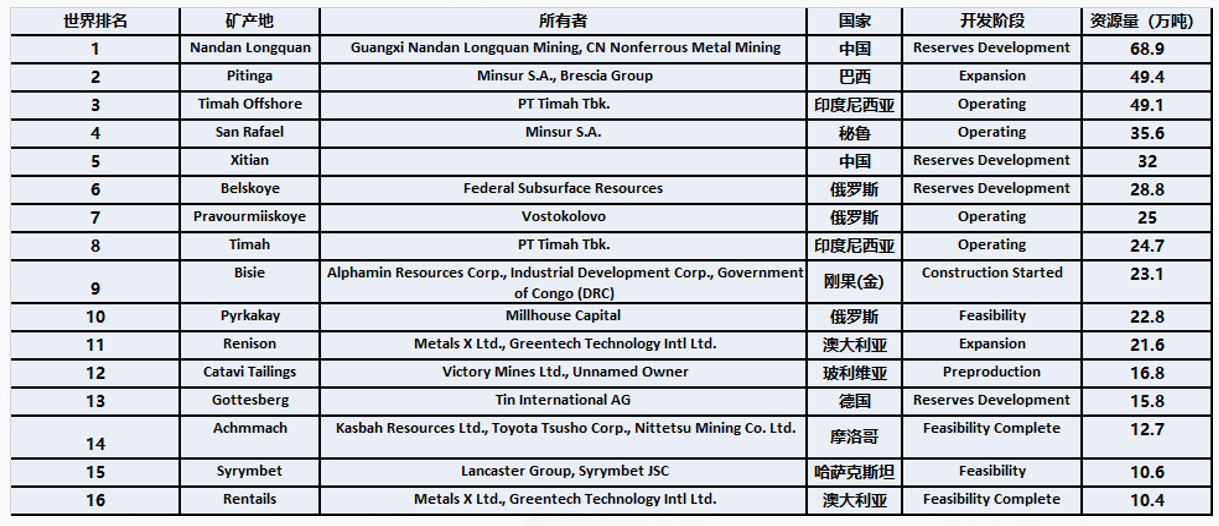

Currently, there are over 70 countries (regions) engaged in the exploration, development, and utilization of tin ore resources globally, with 218 existing tin mines worldwide. Among them, 61 mines have resources exceeding 10,000 mt, and 16 mines have resources exceeding 100,000 mt.

Major Global Tin Mines

The total resources of global tin mines exceeding 100,000 mt amount to 4.47 million mt, accounting for approximately 40-50%.

Current Situation and Development of Tin Mines in Myanmar

Resource Situation in Wa State

The mineral resources in Wa State can be roughly divided into three parts:

1. The Jinchang Mining Area in the Nandeng Special Zone was one of the earliest discovered, with zinc oxide, lead-zinc ore, and zinc sulfide as its main ore types. Other ore types are not found in significant quantities.

2. The Longtan Mining Area primarily features tin ore, lead-zinc ore, and gold ore as its main ore types.

3. The Manxiang (Bangka) Mining Area is currently the largest in scale, with tin ore, lead-zinc ore, and Bangyang antimony ore as its main ore types. Among them, the Bangka tin polymetallic ore and Bangyang antimony ore are newly discovered mining areas in recent years.

Myanmar's Tin Ore Supply and Global Market Share

In 2024, Myanmar imported 21,300 mt of tin ingots in metal content, a 47.54% YoY decrease. As of April 2025, the imported volume in physical content was approximately 3,600 mt, a 20% YoY decrease.

Due to over-mining in the early stages, the grade of tin ore in Wa State has been decreasing year by year. In 2023, after experiencing policy changes, Myanmar's share in the global tin ore supply has dropped to 8%, and further decreased to 3% in Q1 of this year.

Keynote Speech: Application Prospects of Spiral Chute Separation Technology in Tin Ores

Speaker: Li Chun'ou, General Manager of ALICOCO Mineral Technology Co., Ltd.

Features of Spiral Chutes

1. Modular Design for Large-Scale Production, Convenient Transportation, and Installation

The modular design allows the equipment to be disassembled into components for transportation, saving ocean freight costs and enabling rapid assembly at the mining site. Operators can master the equipment with just 2 hours of training, significantly reducing long-distance transportation costs and allowing high-quality, low-cost radiation to the global market.

2. Efficient Separation and High Recovery Rate

The spiral chutes produced using injection molding methods feature a fine groove surface structure that combines smoothness and roughness, achieving efficient separation, especially for fine-grained minerals (such as gold, tungsten, tin, etc.). For example, in tin ore tests, the L-type spiral machine enriched the raw ore tin grade from Sn 0.4% to 10.2% in one pass, achieving a 25-fold enrichment ratio, with a recovery rate comparable to that of shaking tables but with less tailings loss. In a scheelite project in Australia, spiral chutes replaced the flotation process, with spiral gravity separation achieving a recovery rate of over 80% for the raw ore (currently, the recovery rate for scheelite flotation with heating is around 78%).

3. Large Processing Capacity and No Power Requirement

The spiral chute has a simple structure with no moving parts, relying on gravity and water flow for natural separation, eliminating the need for additional power consumption and significantly reducing energy costs. A single unit can process up to 30 mt per hour, making it suitable for large-scale roughing operations in placer mines.

4. Strong Adaptability and Low Operating Costs

The spiral chute exhibits strong adaptability to fluctuations in feed concentration, particle size, and grade, allowing for a wide range of ore concentration variations and reducing the need for pre-treatment. Meanwhile, its nylon/polyurethane material is wear-resistant and corrosion-resistant, with a long service life, significantly reducing the comprehensive ore beneficiation cost compared to traditional flotation processes.

5. Environmental Protection, Energy Efficiency, and Small Footprint

This equipment uses less water and requires no chemical reagents, meeting environmental protection requirements. Compared with traditional ore beneficiation equipment, the spiral chute occupies a smaller area, making it particularly suitable for mine sites with limited space. Meanwhile, the multi-stage separation design further optimizes resource utilization.

Keynote Speech: Modernization and Digital Transformation in Tin-Based Solder Manufacturing

Speaker: Liang Xiaochang, Deputy General Manager of Foshan Juchuang Automation Co., Ltd.

Background and Development Trends of the Tin Solder Industry

Background and Development Trends of the Tin Solder Industry

As one of the crucial materials in electronic manufacturing and assembly processes, the tin solder industry is experiencing a steady upward trend, driven by the growing demand for high-performance and high-reliability solders with the development of industries such as 5G, intelligent manufacturing, and NEVs. Its development is not only driven by the demands of the electronics industry but also deeply influenced by global environmental protection policies, technological innovations, and changes in market demand.

With the advancement of intelligent manufacturing and Industry 4.0, the tin solder industry is undergoing a profound transformation from traditional production to digital and intelligent production.

1. Traditional Tin Solder Production Model:

Production Method: Mainly based on manual experience, with operations heavily relying on human labor

Equipment Level: Single-machine operation with low automation

Data Management: Handwritten records or simple spreadsheets, resulting in information silos

Quality Control: Post-production inspection, with delayed problem identification

Responsiveness: Slow problem response and long adjustment cycles

Customer Service: Reactive approach with low transparency

2. Modernized/Digital Tin Solder Production Model

Production Method: Intelligent manufacturing with automated linkage control

Equipment Level: Intelligent production lines with interconnected equipment

Data Management: Real-time data acquisition and central database management

Quality Control: Process monitoring + predictive maintenance, ensuring stable quality

Responsiveness: Real-time feedback and optimization for rapid iteration

Customer Service: Proactive reporting and traceability systems to enhance trust

Automation and Digitalization Technologies in Tin Solder Production

Automated Alloy Proportioning System: A modern automated alloy proportioning system achieves automated batching through precise sensors, controllers, and PLC systems, ensuring that the chemical composition of tin solder consistently meets standards. The automated feeding equipment adjusts alloy composition in real-time based on system data, significantly enhancing production precision and efficiency.

Keynote Speech: Indian Tin Solder Market: Opportunities and Risks

Speaker: King Fan, Co-founder of Dongguan Jinfang Electronics Technology Co., Ltd.

Future Trends of India's Solder Market

India Aims to Build a $300 Billion Electronics Manufacturing Hub by 2026

$300 Billion Electronics Hub by 2026: Smartphones, EVs, and 5G Infrastructure Drive Demand Growth.

Policy Support:

• "Make in India" and Production-Linked Incentive (PLI) schemes boost domestic manufacturing.

Lead-Free Transition:

• Driven by RoHS (Restriction of Hazardous Substances) and environmental regulations, lead-free solder market share will rise from 60% to 85% by 2030.

Localization Focus:

• By 2030, 40% of tin scrap will be processed domestically; import tariffs continue to rise.

Future Trends of India's Solder Market

Electronics Industry Boom:By 2026, the $300 billion electronics hub will drive solder demand to exceed 5,000 mt annually by 2030 (8-10% CAGR).

Green Transformation: RoHS regulations will push lead-free solder market share to 85% by 2030; Indian government mandates 40% tin recycling utilization rate.

Localization Urgency: 15-20% tariffs incentivize firms to achieve 70% local procurement via "mining→recycling" integration.

Technology-Driven Efficiency: Smart manufacturing reduces defect rates by 30%; tin recovery rate ≥95%, supporting exports surpassing 10,000 mt by 2025.

Seeking Collaborative Suppliers

Tin Ingot Suppliers and Lead Ingot Wholesalers

We seek partnerships with suppliers capable of large-scale high-purity tin and lead ingots (≥99.9%), requiring stable quality compliant with ISO/ROHS standards. Long-term contracts, transparent pricing, and ethical sourcing practices are key to supporting India's electronics and automotive industries.

Keynote Speech: Study on the Applications of Tin Solder in PV Modules

Speaker: Bin Long, Deputy General Manager of Zhongshan Hanhua Tin Co., Ltd.

![The Most-Traded SHFE Tin Contract Opened Lower and Then Traded Stronger, Spot Market Recovers Amid Downtrend [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/WWXJU20251217171753.jpg)

![The most-traded SHFE tin contract fluctuated rangebound during the night session, with downstream enterprises mostly following up with small-lot transactions. [SMM Tin Morning Brief]](https://imgqn.smm.cn/usercenter/bYFQn20251217171752.jpg)