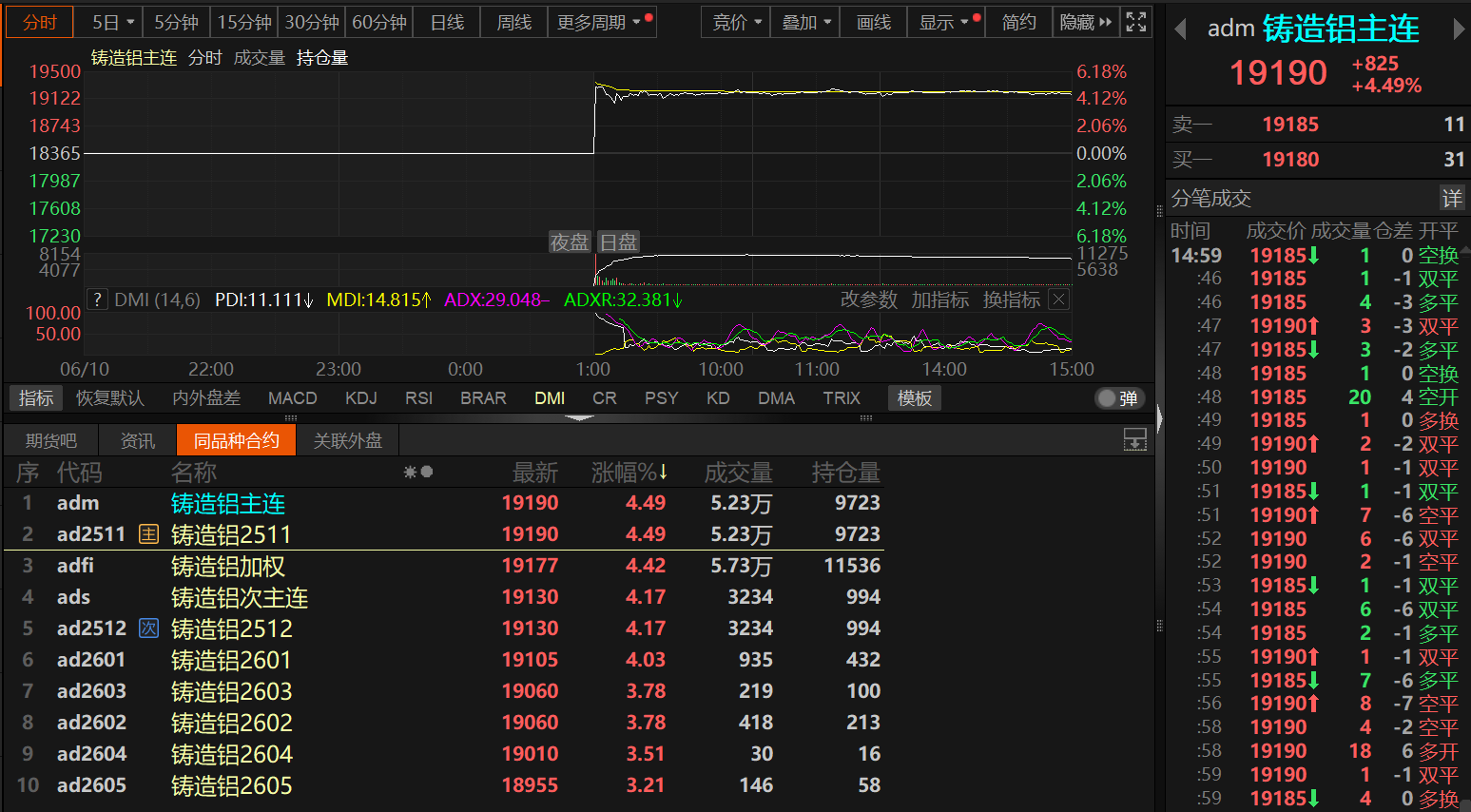

SMM News on June 10: At 9:00 a.m. on June 10, cast aluminum alloy futures were officially listed on the Shanghai Futures Exchange (SHFE). The benchmark listing prices for the AD2511, AD2512, AD2601, AD2602, AD2603, AD2604, and AD2605 contracts were set at 18,365 yuan/mt. During the morning opening, the main contract of cast aluminum alloy futures surged by over 5% at one point. Although the gains subsequently pulled back slightly, they remained at around 4%. By the end of the day session, the main contract closed at 19,190 yuan/mt with a gain of 4.649%.

Regarding the reasons for the significant increase in the opening price of cast aluminum alloy futures, it is widely believed within the industry that the benchmark listing price was significantly lower than the spot price, driven by a clear bullish market sentiment. SMM suggests monitoring the 19,000-19,500 yuan/mt range on the first day.

In terms of spot prices, according to SMM's spot quotes, as of June 10,the spot quote for SMM ADC12 aluminum alloyfell by 100 yuan/mt to 19,800-20,000 yuan/mt, with an average price of 19,900 yuan/mt.

》Click to view SMM's spot quotes for aluminum products

It is not difficult to see the differences between the two from the comparison of futures and spot prices. Funeng Futures also expects that the reasonable valuation range for cast aluminum alloy futures in the early stages of listing will be 19,000-20,000 yuan/mt. Guolian Futures believes that the unilateral price of cast aluminum alloy futures is expected to follow the trend of SHFE aluminum futures, with limited short-term fluctuations both upwards and downwards. The price spread between the market price of ADC12 and that of aluminum ingot A00 fluctuates within the range of -1,000 to 1,000 yuan/mt. The price spread not only has clear upper and lower bounds but also exhibits significant seasonal fluctuations, often following a V-shaped pattern throughout the year.

According to publicly available information, cast aluminum alloy is an aluminum alloy produced through the casting process to form blanks or parts, using aluminum scrap as the main raw material, after smelting with copper, silicon, etc. Cast aluminum alloy is also the primary means of recycling aluminum scrap. The SHFE stated that the upstream of cast aluminum alloy mainly includes aluminum scrap recycling enterprises, aluminum product producers, and aluminum scrap trading enterprises. The downstream mainly includes die-casting plants, automotive parts plants, and automotive OEMs. Downstream products are widely used in fields such as automobiles, motorcycles, machinery equipment, communication equipment, electronic appliances, and hardware lighting.

From the perspective of the current fundamental performance of secondary aluminum, according to SMM, the fundamental support for secondary aluminum alloy is currently weak, and weak demand will continue to suppress the spot price of ADC12. Specifically, on the demand side, there has been little improvement in consumption since June, with the characteristics of the off-season becoming increasingly apparent and downstream purchasing sentiment remaining low. As an important downstream application area for secondary aluminum, the automotive market experiences reduced orders from May to August due to a sluggish sales market, leading enterprises to correspondingly reduce production. Therefore, it is currently the off-season for automotive production. The deepening of the traditional consumption off-season in downstream sectors and the reduction in terminal orders will continue to constrain the upside room for secondary aluminum alloy prices. However, ahead of the listing of cast aluminum alloy futures on the SHFE, some traders have already started or plan to purchase ADC12, a delivery brand, for futures-spot arbitrage, which is expected to enhance market activity and alleviate inventory pressure on enterprises.

In terms of supply, secondary aluminum enterprises that halted production during the Dragon Boat Festival holiday have largely resumed operations, driving a slight rebound in the industry's operating rate. However, as the traditional off-season in downstream sectors persists, there is still pressure on the operating rate to rise further. Nevertheless, given that enterprise operating rates have already declined significantly from April to May, it is expected that the decline in the operating rate of secondary aluminum alloy enterprises in June will be limited. The first listed contract for cast aluminum alloy futures is AD2511. Given the long time until delivery, secondary aluminum enterprises, as delivery brands, will not expand their production scale for the time being, and the supply landscape will not undergo significant changes due to the listing of futures in the short term.

Regarding the raw material aluminum scrap, in recent years, there has been significant capacity expansion in the domestic secondary aluminum industry, leading to a tight supply of aluminum scrap and persistent cost pressure on enterprises. Aluminum scrap prices have generally fluctuated at highs, providing cost support for ADC12 prices.

Therefore, in the short term, the fundamental support for the secondary aluminum alloy industry is relatively weak, and weak demand will continue to suppress spot prices of ADC12. However, in the medium and long term, new capacity additions in the secondary aluminum alloy industry are expected to continue to increase in 2025, raising supply pressure. Imports may decline, reducing the impact on the domestic market. Although the cost support from aluminum scrap for ADC12 prices remains strong, the increase in supply and weaker-than-expected demand may limit price gains. Going forward, it is necessary to focus on the supply situation of raw materials, changes in order volumes, as well as the actual impact and market feedback of the listing of cast aluminum alloy futures on domestic spot prices and market trading patterns.

Institutional Comments

Galaxy Futures believes that there are still many new capacity additions for cast aluminum alloy, with a relatively low operating rate and intense market competition. There are no significant bright spots on the demand side, and the price center may fall again.

Wu Mingjin, an analyst at Zhonghui Futures, believes that the listing of cast aluminum alloy as the first recycled metal variety enriches the futures commodity family and contributes to the development of new-type industrialization, assisting in the green and low-carbon transformation of the industry. The rise during the day was partly due to the low listing benchmark price and partly due to market enthusiasm. Currently, the aluminum industry is in a seasonal consumption off-season, and consumption in the end-use market for aluminum alloys is gradually weakening. In the short term, it is expected that there will be limited upside potential, and it may be more prudent to take a bearish stance above the 20,000 mark, while paying attention to the support of the listing benchmark price on the futures market.

China Securities Futures stated that the strategies for the first day of cast aluminum alloy futures can be summarized in three aspects: First, for short- to medium-term strategies, it is more appropriate to engage in high selling and low buying within the aforementioned range in the short term. Given that the listing benchmark price is significantly lower than the aforementioned range, bidding up is the main approach, but caution should also be exercised against a pullback after a sharp rise. Second, for over-the-counter option strategies, it is expected that cast aluminum will fluctuate at lows following electrolytic aluminum after listing, and with support from costs and low inventory below, holders of spot cargo may consider a cumulative selling option strategy to earn additional premiums and increase profits. Third, for arbitrage strategies, due to the possibility of seasonal price peaks in the first delivery month, it is expected that the cast aluminum alloy futures market will exhibit a backwardation structure after listing. Therefore, opportunities for calendar spread arbitrage are worth noting. At the same time, inter-commodity spread arbitrage can focus on the price spread between ADC12 and A00. As the off-season deepens, it is advisable to take a long position in the spread futures, that is, long cast aluminum alloy and short electrolytic aluminum.

Guotai Junan Futures analysis suggests that for cast aluminum alloy, the listing prices are relatively low, and there may be an increase of around 6-8% during the opening call auction on the first day. However, the fundamentals of cast aluminum alloy are weak, with bearish sentiment prevailing. It is expected that the listing will likely see a move downwards after a higher opening, with the main operating range in the short term being 19,000-19,600 yuan/mt. They indicated that during the initial listing period, the term structure may primarily reflect reality, exhibiting a Contango structure during the off-season. Considering historical seasonality, the inter-month structure may transition from Contango to Back in Q3. After the listing, attention can be paid to entering long positions in calendar spreads at low levels, with expected gains to be realized during the peak consumption season. If considering a risk-free calendar spread strategy, based on the listing prices of cast aluminum alloy and the margin charged by the exchange, combined with warrant pledging, the estimated cost of the inter-month calendar spread is around 85 yuan/mt. Therefore, if the inter-month price spread between the cast aluminum alloy futures contracts AD2512 and AD2511 is higher than 85 yuan/mt, it may be considered to enter a risk-free calendar spread. If considering the additional margin charged by the futures company and the associated capital cost, the risk-free calendar spread would need to reach around 100 yuan/mt.

Wuchan Zhongda Futures commented that the benchmark listing price for the first batch of listed contracts, such as AD2511, is 18,365 yuan/mt. Based on the current "cost support" fundamental landscape of ADC12 and the calculation of risk-free arbitrage, the listing price of 18,365 yuan/mt for the AD2511 contract is significantly lower than the forward spot price (the current mainstream transaction price for spot aluminum is approximately 19,400 yuan/mt, and with risk-free arbitrage of 46 yuan/mt per month through pledging, the November contract price is expected to be at 19,630 yuan/mt). In terms of unilateral strategies, given the currently low listing price of the contract, it is advisable to take long positions at low levels. In the long term, considering the surplus landscape in the secondary aluminum industry with a capacity utilisation rate of less than 50%, and the lack of significant bright spots in downstream demand, ADC12 prices will continue to face pressure in the medium term, and it may be advisable to take short positions at high levels.