SMM, June 6:

Metal Market:

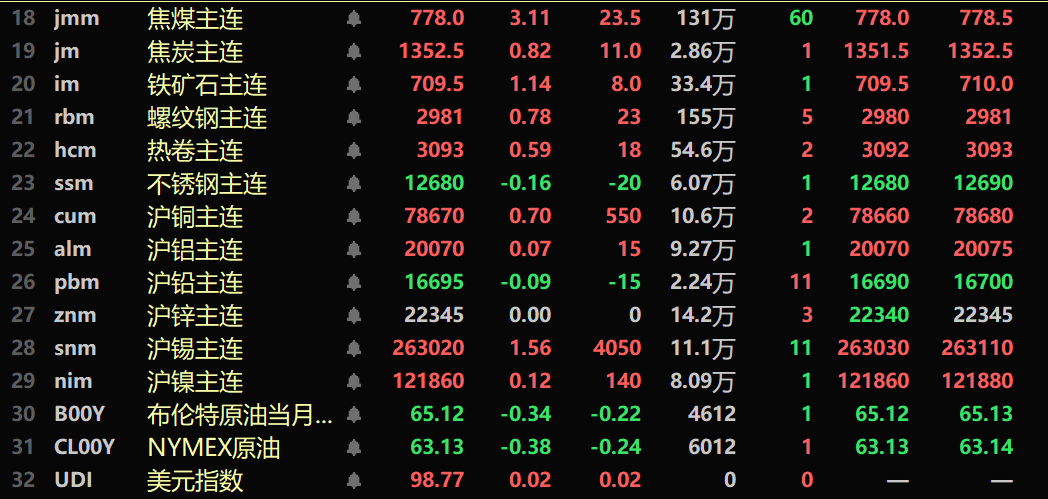

As of the midday close, domestic base metals generally rose. SHFE copper increased by 0.7%, SHFE zinc remained flat at 22,345 yuan/mt, SHFE aluminum rose slightly, SHFE lead fell slightly, SHFE tin rose by 1.56%, and SHFE nickel rose by 0.12%.

In addition, alumina fell by 1.47%, lithium carbonate rose by 1.09%, silicon metal rose by 2.45%, and polysilicon rose by 0.66%.

The ferrous metals series mostly rose, with iron ore up by 1.14%, rebar up by 0.78%, and HRC up by 0.59%. Stainless steel fell by 0.16%. In terms of coking coal and coke, coking coal rose by 3.11%, and coke rose by 0.82%.

In the overseas metal market, as of 11:42, LME metals showed mixed performance, with LME zinc up by 0.3%, LME copper falling slightly, LME aluminum rising slightly, LME lead up by 0.3%, LME tin down by 0.19%, and LME nickel down by 0.28%.

In the precious metals market, as of 11:42, COMEX gold rose by 0.45%, and COMEX silver rose by 1.01%. Domestically, SHFE gold fell by 0.11%, SHFE silver rose by 3.88%, hitting a new high since listing at 8,834 yuan/kg during the session.

As of the midday close, the most-traded contract of the European Containerized Freight Index fell by 1.93%, closing at 2,114.5.

As of 11:42 on June 6, midday futures market movements for some contracts:

》SMM Metal Spot Prices on June 6

Spot and Fundamentals

Aluminum: In terms of inventory, according to SMM's domestic aluminum ingot inventory data, domestic electrolytic aluminum ingot inventory across three regions stood at 371,000 mt on June 6, a destocking of 10,000 mt from the previous day. In the short term, the lower arrival of goods is conducive to maintaining premiums, but downstream acceptance of high premiums has decreased. Coupled with weakening demand during the off-season and a backdrop of weak supply and demand, holders are actively selling, and premiums and discounts are expected to pull back mainly. 》Click for details

Iron Ore: This week, imported iron ore prices first declined and then rose. During the Dragon Boat Festival holiday, the US White House announced an increase in tariffs on imported steel, aluminum, and their derivatives from 25% to 50%. This news exacerbated market concerns about the uncertainty of steel exports, leading to the spread of market pessimism. However, as positive signals were released during the phone call between the heads of state of China and the US on Thursday night... 》Click for details

Macro Front

Domestically:

[China's Warehousing Index for May was 50.5%, Operating in Expansion Territory for 7 Consecutive Months] The China Federation of Logistics and Purchasing released China's warehousing index for May today (the 6th). Data changes indicate that warehousing business activities are active, demand continues to grow, and the warehousing industry maintains a stable and improving operational trend. In May, China's warehousing index stood at 50.5%, a pullback of 0.2 percentage points MoM, operating in expansion territory for seven consecutive months.

[Cailian Press C50 Wind Vane Index Survey: New Social Financing in May May Increase YoY, M2 YoY Growth Rate Expected to Continue Rebounding] The latest results of Cailian Press's "C50 Wind Vane Index" show that the median forecast of market institutions for new RMB loans in May is RMB 0.6 trillion, a decrease of RMB 0.35 trillion YoY. Additionally, the median forecast for new social financing in May is RMB 2.32 trillion, an increase of RMB 0.26 trillion YoY. Meanwhile, the market expects that with improved liquidity and a low base effect, the M2 YoY growth rate in May may continue to rebound. In terms of prices, the CPI in May may remain relatively stable, while the PPI decline continues to widen. From a YoY perspective, the median forecast of market institutions for the CPI YoY growth rate in May is -0.2%, and for the PPI YoY growth rate in May is -3.3%. (Cailian Press)

[PBOC's Open Market Operations Net Withdraw RMB 156.1 Billion Today] The PBOC conducted RMB 135 billion in 7-day reverse repo operations today. With RMB 291.1 billion in 7-day reverse repos maturing today, a net withdrawal of RMB 156.1 billion was realized on the day. This week, the PBOC conducted RMB 930.9 billion in reverse repo operations. With RMB 1,602.6 billion in reverse repos maturing this week, a net withdrawal of RMB 671.7 billion was realized this week. Additionally, the PBOC conducted RMB 1 trillion in outright reverse repo operations today.

US dollar:

As of 11:42, the US dollar index rose 0.02% to 98.77. The US service sector contracted for the first time in nearly a year in May, and initial jobless claims rose again last week, indicating that the labour market is cooling. Following a series of data this week highlighting weakness in the US labour market, the market is now awaiting the release of US non-farm payrolls data at 20:30 Beijing time. Economists surveyed predict that the US will add 130,000 non-farm jobs in May, down from 177,000 in April, with the unemployment rate expected to remain stable at 4.2%. Two US Fed policymakers said on Thursday that they view the current rise in inflation as a more pressing risk than the slowdown in the labour market, a view suggesting they support maintaining monetary policy unchanged for a longer period.

Other currencies:

After the European Central Bank cut interest rates by 25 basis points, the euro-dollar exchange rate became volatile, touching a 1.5-month high at one point. Market participants interpreted comments by European Central Bank President Christine Lagarde as slightly hawkish, suggesting that the interest rate cut cycle may be nearing its end. Germany's 2-year government bond yield turned positive, and the yield spread between German and US 2-year government bonds narrowed to its lowest level since May 2. The spread between the US Fed's and the ECB's terminal interest rates also narrowed to its lowest level since May 7, with market expectations indicating a convergence in the policy paths of the two central banks. (Huitong Finance)

Data:

[Global manufacturing PMI below 50% for three consecutive months, global economy hovering at low levels]The China Federation of Logistics and Purchasing released the global manufacturing PMI for May today (the 6th). The global manufacturing PMI for May was 49.2%, up 0.1 percentage point MoM, remaining below 50% for three consecutive months. By region, the manufacturing PMI for the Americas in May was 48.4%, unchanged from the previous month and below 49% for three consecutive months, indicating that the manufacturing sector in the Americas continues to operate in contraction territory. Data from major countries showed that the US manufacturing PMI for May was 48.5%, down 0.2 percentage point MoM, declining MoM for four consecutive months. The data changes suggest that the US manufacturing sector continues to weaken under the influence of tariff hikes imposed by the US.

Today, data such as Germany's April seasonally adjusted industrial production MoM, Germany's April working-day adjusted industrial production YoY, Germany's April seasonally adjusted exports MoM, France's April trade balance, the Eurozone's Q1 seasonally adjusted GDP QoQ final value, the Eurozone's Q1 seasonally adjusted GDP YoY final value, the Eurozone's April retail sales MoM, the Eurozone's April retail sales YoY, Canada's May leading indicators MoM, the US's May seasonally adjusted non-farm payrolls change, the US's May average hourly earnings YoY, the US's May private sector non-farm payrolls change, the US's May labor force participation rate, the US's May seasonally adjusted manufacturing employment change, the US's May unemployment rate, Canada's May employment change, and Canada's May unemployment rate will be released. In addition, it is worth noting that Federal Reserve Governor Adriana Kugler will speak at the Economic Club of New York, and Philadelphia Fed President Patrick Harker, a 2026 FOMC voter, will speak on the economic outlook.

Crude oil:

As of 11:42, crude oil futures dropped slightly, with US crude oil down 0.38% and Brent crude oil down 0.34%. Oil prices are expected to record their first weekly gain in three weeks, following a phone call between the leaders of China and the US and their agreement to hold a new round of talks, which has raised market hopes for stronger growth and demand in the world's two largest economies. In addition, production cuts in Canada due to ongoing wildfires have also provided support for oil prices.

Saudi Arabia, the world's largest oil exporter, has reduced its crude oil prices for Asian buyers in July to the lowest level in nearly two months. This reduction by Saudi Arabia was smaller than expected after OPEC agreed to increase daily production by 411,000 barrels in July. Saudi Arabia has been advocating for a more significant production increase as part of a broader strategy to regain market share and discipline OPEC member countries that exceed their production quotas. (Webstock Inc.)

Spot Market Overview:

Midday reviews of spot prices for other metals will be updated later. Please refresh to view.