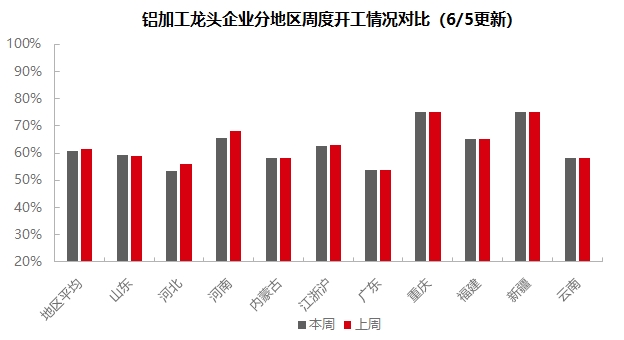

On June 5, 2025:

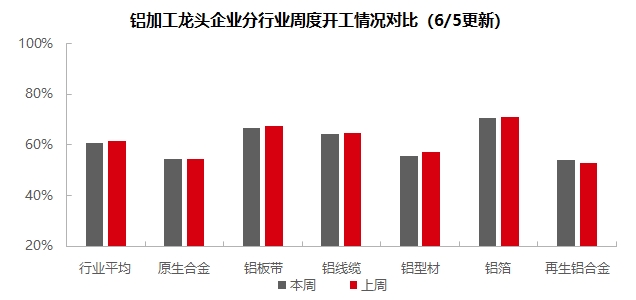

As June arrives, the downstream aluminum processing sector is deeply entrenched in the off-season atmosphere. The weekly operating rate fell by 0.4 percentage points WoW to 60.9%. By segment, the primary aluminum alloy industry saw relatively small overall changes in operating rates compared to May. Most enterprises in the industry reported moderate stability in orders on hand, with no pullback in operating rates observed in production. In the aluminum plate/sheet and strip segment, aluminum prices remained high during the week, with downstream customers showing strong wait-and-see sentiment. As the market transitioned from peak to off-season, overall demand weakened, leading to a decline in operating rates for some sample enterprises. In the aluminum wire and cable segment, as the concentrated delivery period has passed, enterprises' enthusiasm for procurement and production has waned, and market order performance has also weakened. Continuous attention is needed on the arrival of the next delivery cycle and order performance in market segments such as PV, wind power, automotive wiring harnesses, and infrastructure. This week, the aluminum extrusion segment showed a divergence in operating rates. New orders in various construction material fields were weak, leading to a decline in operating rates. Affected by the sluggish procurement sentiment of downstream component manufacturers, the operating rates of PV frame extrusion plants also declined. Despite the lukewarm performance of the NEV segment, relatively saturated orders in the 3C sector, power pipelines, and rail transit provided some support to operating rates. In the aluminum foil segment, the current industry processing fee has touched the cost floor. Under pressure from total volume assessments, enterprises were forced to adopt a "volume discount" strategy. Meanwhile, the continuously rising finished product inventories have become another constraint factor suppressing processing fees. Continuous attention is needed on destocking. In the secondary aluminum segment, although aluminum prices stabilized and rebounded during the week, downstream enterprises' purchase willingness remained cold, and demand remained sluggish. Both domestic market and export orders declined to varying degrees. SMM expects that the weekly operating rate of the downstream aluminum processing sector may decline slightly by 0.1 percentage points MoM to 60.8% next week.

Primary Alloy: This week, the operating rates of leading enterprises in the primary aluminum alloy industry continued to hold steady at last week's level. In the first week of June, the primary aluminum alloy industry saw relatively small overall changes in operating rates compared to May. Most enterprises in the industry reported moderate stability in orders on hand, with no significant changes observed, and no pullback in operating rates in production. As the export data and domestic demand performance of the downstream aluminum alloy wheel hub segment remain relatively stable, several primary alloy enterprises remain optimistic about subsequent operating performance. Whether to adjust production pace will depend on subsequent order conditions. Some enterprises also reported that, influenced by the expectation of reaching full production targets in H1, they still have plans to increase production in June. However, looking ahead, under the dual constraints of off-season factors and escalating Sino-US frictions, the overall operating rates of the primary aluminum alloy industry may continue to exhibit a generally stable with slight fall trend. Substantial trend reversals will depend on the implementation details of Sino-US consultations.

Aluminum plate/sheet and strip: This week, the operating rate of leading enterprises in the aluminum plate/sheet and strip sector decreased by 1 percentage point MoM from the period before the holiday to 66.6%. Aluminum prices remained high during the week, and downstream customers maintained a strong wait-and-see sentiment. Additionally, as the market transitioned from the off-season to the peak season, overall demand continued to weaken, prompting some sample enterprises to ease their production pace. In terms of end-use consumption, aluminum plate/sheet and strip products linked to automotive, home appliance, kitchen and bathroom, and other consumer terminals maintained normal production. However, demand in the construction sector continued to weaken, with production schedules for June orders declining MoM from May. Although orders in the 3C consumer electronics sector grew rapidly, they were insufficient to boost the overall industry's operating rate. With the official start of the June off-season, it is expected that the operating rate of aluminum plate/sheet and strip enterprises will remain in the doldrums in the subsequent period.

Aluminum wire and cable: This week, the operating rate of leading enterprises in the aluminum wire and cable sector stood at 64.2%, down 0.6% MoM. As June began, although the industry's concentrated delivery period had passed, leading enterprises maintained a reasonable production schedule based on their orders on hand, resulting in a slight decline in the operating rate. In terms of orders, the State Grid officially launched the third tender for transmission and transformation line installation materials in early June, involving 128,000 mt of aluminum-core conductor and ground wire orders, with a staggered delivery cycle from August 2025 to March 2026. Meanwhile, the first tender for distribution network agreement inventory in Henan Province was also underway, with scattered provincial grid orders still being released. As the concentrated delivery period has passed, enterprises' enthusiasm for procurement and production has declined, and market order performance has also weakened and become more fragmented. It is necessary to closely monitor the arrival of the next delivery cycle and the order performance in market segments such as PV, wind power, automotive wiring harnesses, and infrastructure. It is expected that the operating rate of aluminum wire and cable enterprises will remain in the doldrums in the short term.

Aluminum extrusion: This week, the national operating rate for extrusions decreased slightly by 1.5 percentage points MoM to 55.5%. In the building materials sector, the overall operating rate declined slightly WoW. According to the SMM survey, as June began, leading building materials enterprises in central China reported that their overall operating rates were lower than the same period last month. Apart from a small number of stable customers, new orders across various building materials sectors were weak. This week, orders for infrastructure, doors and windows, and dealers all declined to varying degrees. Enterprises in other regions, such as Shandong, Hebei, and parts of South China, reported that their building materials production remained largely unchanged from the previous week. This week, the operating rates of sample enterprises in the PV frame sector continued to diverge. Some leading enterprises in east China saw a slight decline in their operating rates WoW, mainly due to weak purchasing sentiment from downstream module manufacturers and enterprises' relatively pessimistic expectations for module production schedules in June. However, according to the SMM survey, some new production capacities of manufacturers in Anhui Province were steadily ramping up and were expected to reach full capacity in H2. Meanwhile, according to the SMM survey, some small and medium-sized enterprises in Anhui and Henan provinces reported that their PV production lines were gradually exiting the market, with only orders from long-established customers being maintained. Their operating rates for PV frames remained at a low level of 30%. This week, some deep-processing enterprises in east China reported an upward trend in the operating rates of their 3C production lines. These enterprises are optimistic about the high added value in the 3C sector and plan to vigorously promote the operation of these production lines. For automotive extrusion sample enterprises, the operating rates remained largely unchanged from last week, with new orders still sluggish. Enterprises hold differing expectations for June production. Some east China parts producers with more complex production processes reported that their June production is expected to increase, with new orders anticipated to be confirmed by mid-June. However, some enterprises in east and south China reported a strong off-season atmosphere in June, with a significant decline in orders on hand as of this week, which is expected to remain difficult to improve in the short term. For other industrial materials, some enterprises in Shandong and central China that produce power pipelines and railway transportation components (such as subway thresholds and subway car bodies) reported that relevant orders are being produced in an orderly manner, with relatively saturated orders on hand. SMM will continue to monitor the actual progress of order fulfillment in various sectors. SMM will continue to monitor the actual progress of order fulfillment in various sectors.

Aluminum Foil: This week, the operating rate of leading aluminum foil enterprises reached 71.6%. By product, battery foil and brazing foil production schedules are proceeding normally, while tobacco foil, pharmaceutical foil, and capacitor foil also showed stable performance. For double-zero packaging foil, the processing fee of leading enterprises has dropped to 5,800 yuan/mt, with a significant cumulative decline since the beginning of the year. Due to pressure from total volume assessments, enterprises are forced to adopt a "volume discount" strategy, indirectly confirming that the current processing fee has touched the cost floor, severely squeezing the industry's profit margins. Meanwhile, the continuously rising finished product inventories in the near term have become another constraint on processing fees. If the destocking effect in June falls short of expectations, processing fees may decline further, and some enterprises may face cash flow challenges. It is expected that the operating rates of aluminum foil enterprises will fluctuate downward subsequently.

Secondary Aluminum: This week, the operating rate of leading secondary aluminum enterprises fell by 0.5 percentage points WoW to 55.6%. Aluminum prices stabilized and rebounded during the week, but downstream enterprises' purchase willingness remained weak, with demand weakness persisting. Both domestic market and export orders declined to varying degrees. Secondary aluminum smelters generally faced difficulties in product shipments and inventory pressure, forcing enterprises to reduce their operating levels. As the Labour Day holiday approaches, some die-casting enterprises anticipate pre-holiday stockpiling, which is expected to drive an improvement in market transactions next week. However, low visibility of terminal orders restricts the intensity of stockpiling. In the short term, the industry's operating rate is expected to decline slightly.

》Click to view SMM Aluminum Industry Chain Database

(SMM Aluminum Team)