SMM June 5 News:

Metal Market:

As of the midday close, domestic base metals showed mixed performance. SHFE copper and SHFE zinc fell slightly, SHFE aluminum rose by 0.1%, SHFE lead increased by 0.51%, SHFE tin gained 1.49%, and SHFE nickel dropped by 0.38%.

In addition, alumina fell by 2.97%, lithium carbonate decreased by 0.33%, silicon metal dropped by 0.91%, and polysilicon fell by 2.25%.

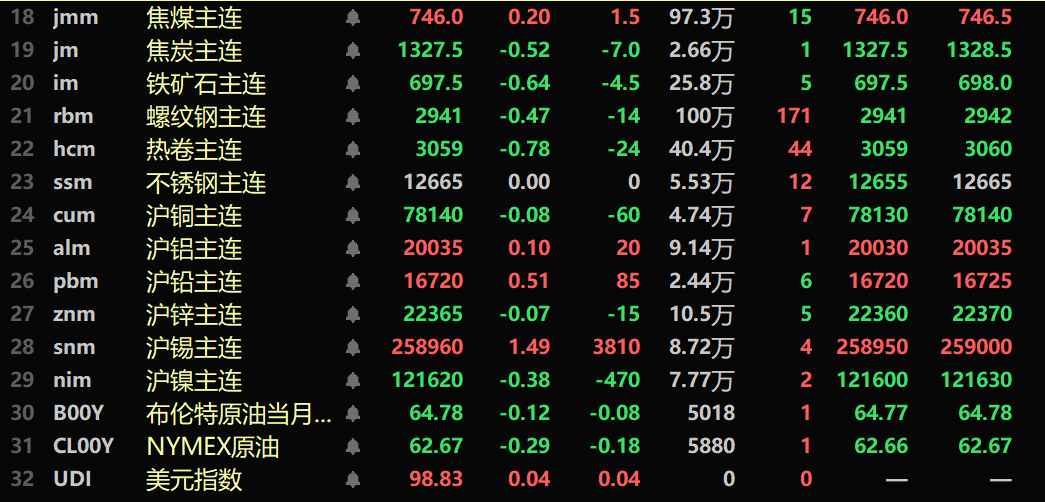

The ferrous metals series mostly fell, with iron ore down by 0.64%, rebar declining by 0.47%, and HRC falling by 0.78%. Stainless steel remained flat at 12,665 yuan/mt. For coking coal and coke: coking coal rose by 0.2%, and coke fell by 0.52%.

In the overseas metal market, as of 11:49, LME metals showed mixed performance. LME zinc and LME copper rose slightly, LME lead fell by 0.23%, LME aluminum increased by 0.1%, LME tin dropped by 0.26%, and LME nickel decreased by 0.03%.

In precious metals, as of 11:49, COMEX gold fell slightly, while COMEX silver rose by 0.24%. Domestically, SHFE gold increased by 0.42%, and SHFE silver rose by 0.07%.

As of the midday close, the most-traded contract for the European container shipping line fell by 0.95%, closing at 2,128.2.

As of 11:49 on June 5, the midday futures market conditions for some products were as follows:

》SMM Metal Spot Prices on June 5

Spot and Fundamentals

Lead: Today, the SMM 1# lead average price increased by 75 yuan/mt from yesterday to 16,500 yuan/mt. Secondary lead smelters' shipping sentiment improved, with the mainstream ex-factory prices of secondary refined lead showing a premium of 100-0 yuan/mt against the SMM 1# lead average price. The price difference between primary metal and scrap narrowed to 0 yuan/mt... 》Click for details

Macro Front

Domestic:

[National Energy Administration: National Power Supply Expected to be Generally Secure During Summer Peak This Year]Hao Ruifeng, Director of the Market Regulation Department of the National Energy Administration, stated at a State Council Information Office press conference that, based on the current situation, it is expected that the national power supply will be generally secure during the summer peak this year, although there may be tight power supply conditions in some regions during peak periods. Hao Ruifeng pointed out that the National Energy Administration aims to ensure flexible regular supply, implement measures for localized short-term tightness, and achieve effective responses in extreme situations, pressing all parties to fulfill their responsibilities. Through measures such as strengthening energy and power monitoring and early warning, fully leveraging power supply potential during peak periods, accelerating the construction and commissioning of supportive power sources, optimizing cross-provincial power interchanges, and enhancing demand-side response, the Administration will strive to ensure the safe and stable power supply during the summer peak.

[Song Hongkun, Deputy Director of the National Energy Administration: Wind, PV, and Nuclear Power Installations Surpassed Thermal Power Installations for the First Time by the End of April]Song Hongkun, Deputy Director of the National Energy Administration, stated at a State Council Information Office press conference today that as of the end of April this year, China's installed renewable energy power generation capacity reached 2.017 billion kW, up 58% YoY, with wind, PV, and nuclear power installations reaching 1.53 billion kW, surpassing thermal power installations for the first time.

[Ministry of Ecology and Environment: Coal consumption accounted for 53.2% of total energy consumption in 2024]The Ministry of Ecology and Environment officially released the "Report on the State of China's Ecology and Environment in 2024". Coal consumption accounted for 53.2% of total energy consumption, a decrease of 1.6 percentage points from 2023. The consumption of clean energy sources, including natural gas, hydropower, nuclear power, wind power, and solar power, accounted for 28.6% of total energy consumption, an increase of 2.2 percentage points from 2023. By the end of 2024, the cumulative trading volume of carbon emission allowances in the national carbon emissions trading market reached 630 million mt, with a cumulative turnover of 43.033 billion yuan.

[Caixin China General Services PMI rose to 51.1 in May]The Caixin China General Services Business Activity Index (Services PMI) for May, released today, stood at 51.1, up 0.4 percentage points from April, indicating an acceleration in the expansion of services sector operations.

[PBOC net withdrew 139.5 billion yuan from the open market today]The PBOC conducted 126.5 billion yuan of 7-day reverse repo operations today. With 266 billion yuan of 7-day reverse repos maturing today, a net withdrawal of 139.5 billion yuan was realized on the day.

US dollar:

As of 11:49, the US dollar index rose 0.04% to 98.83. US economic data was weaker than expected, while market participants were also weighing lingering global economic and political uncertainties. The US ADP National Employment Report showed that private sector employment increased by only 37,000 jobs in May, the fewest in more than two years. Investors are awaiting Friday's non-farm payrolls report for further clues on the labour market. The US services sector contracted for the first time in nearly a year in May, with firms' input prices rising to the highest level in two and a half years. The Fed's Beige Book stated that US economic activity had declined in the weeks since the Fed's policymakers last met to set interest rates, with higher tariff rates putting upward pressure on costs and prices. US President Trump again urged Fed Chairman Powell to cut interest rates on Wednesday, noting that the latest ADP employment report showed a slowdown in job growth.

Other currencies:

Expectations for a rate hike by the Bank of Japan (BOJ) continued to rise, but yen bulls held their positions for the time being. The latest data showed that nominal wages in Japan rose 2.3% YoY in April, the fastest pace in four months, but real wages fell for the fourth consecutive month, down 1.8%, highlighting that wage growth is still struggling to keep up with inflationary pressures. This "nominal increase, actual decline" structure provides justification for the Bank of Japan to continue tightening its policies. "Despite relatively rapid nominal wage growth, households' real purchasing power continues to decline amid high inflation, making it more likely for the central bank to continue adopting a gradual interest rate hike path," said Shinichi Sato, an analyst at Toyo Keizai Research Institute. (Huitong Finance)

Data Releases:

Today, the following data will be released: the global ANZ commodity price index annual rate for May, Australia's goods and services trade balance for April, Australia's export monthly rate for April, Australia's import monthly rate for April, China's Caixin Services PMI for May, Switzerland's unadjusted unemployment rate for May, Switzerland's seasonally adjusted unemployment rate for May, the global leading indicator for turning points in the industrial production cycle for May, the number of job cuts announced by US companies in May, the European Central Bank's (ECB) main refinancing rate for June, the ECB's deposit facility rate for June, the ECB's marginal lending facility rate for June, the US trade balance for April, the number of initial jobless claims in the US for the week ending May 31, the number of continuing jobless claims in the US for the week ending May 31, Canada's trade balance for April, Canada's IVEY seasonally adjusted PMI for May, Canada's IVEY unadjusted PMI for May, and the global supply chain pressure index for May. Additionally, notable events include: the US Fed releasing the Beige Book on economic conditions; the ECB announcing its interest rate decision; and ECB President Christine Lagarde holding a press conference on monetary policy.

Crude Oil Market:

As of 11:49, crude oil futures have all dropped slightly, with US crude oil down 0.29% and Brent crude oil down 0.12%. This follows an increase in US gasoline and diesel inventories, as well as Saudi Arabia lowering its prices for Asian crude oil buyers in July.

Saudi Arabia, the world's largest oil exporter, lowered its prices for Asian crude oil buyers in July on Wednesday to the lowest level in two months, which the market views as an attempt by Saudi Arabia to regain market share. Saudi Arabia is a major oil producer within the OPEC oil production group, which includes member countries of the Organization of the Petroleum Exporting Countries (OPEC) and allies such as Russia. This move comes after OPEC decided to increase oil production by 411,000 barrels per day in July over the weekend. (Webstock Inc.)

Spot Market Overview:

Midday reviews of other metal spot markets will be updated later. Please refresh to view.