SMM, June 5:

Metal Market:

Overnight, domestic market base metals showed mixed performance, with SHFE tin rising by 1.51%. SHFE copper fell slightly. SHFE nickel dropped by 0.29%. SHFE lead increased by 0.54%. SHFE aluminum rose by 0.47%, and SHFE zinc remained flat at 22,380 yuan/mt. In addition, the most-traded alumina futures rose slightly.

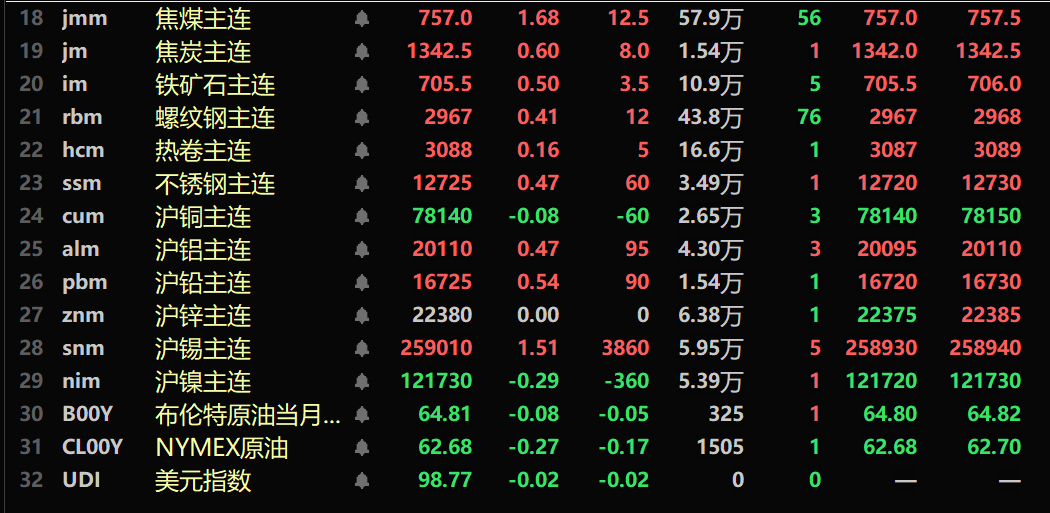

Overnight, the ferrous metals series all rose, with iron ore increasing by 0.5%, stainless steel rising by 0.47%, rebar up by 0.41%, and HRC gaining 0.16%. In terms of coking coal and coke: coking coal fell by 1.68%, while coke rose by 0.6%.

Overnight, overseas market base metals showed mixed performance, with LME copper rising by 0.16%, LME aluminum increasing by 0.95%, LME lead and LME zinc falling slightly, LME tin gaining 1.65%, and LME nickel dropping by 0.7%.

Overnight, precious metals: COMEX gold rose by 0.6%; COMEX silver increased by 0.06%. Overnight, SHFE gold rose by 0.45%, and SHFE silver remained flat at 8,447 yuan/kg.

As of 8:15 on June 5, overnight closing prices

》Click to view SMM Futures Data Dashboard

Macro Front

Domestic:

[MIIT Deploys to Promote the Development of the AI Industry and Empower New-type Industrialization] Li Lecheng, Secretary of the Party Leadership Group and Minister of the Ministry of Industry and Information Technology, chaired a meeting on June 3 to study and promote the ideas and measures for the development of the AI industry and empowering new-type industrialization. The meeting emphasized the need for systematic planning and coordinated promotion to comprehensively implement tasks in strategy, planning, policies, and standards, creating a favorable ecological environment for the development of the AI industry and empowering new-type industrialization, fully stimulating innovation vitality. It is necessary to consolidate the industrial foundation. Strengthen computing power supply, coordinate the layout of general-purpose large models and industry-specific large models, focus on hardware and software adaptation, accelerate the establishment of high-quality industry datasets, and enhance the intelligence level of key products and equipment. It is necessary to shape application advantages. Promote the deployment of large models in key industries of the manufacturing sector, accelerate the refinement of application scenario requirements, accelerate the intelligent upgrading of the entire manufacturing process, and transform production management modes. Cultivate a group of AI-enabled application service providers and accelerate the deployment, application, and iterative upgrading of industry-specific large models. It is necessary to strengthen standard leadership. Coordinate the promotion of AI standardization work, leverage the roles of an effective market and a proactive government, advance standard formulation in a graded, classified, and systematic manner, and effectively leverage the foundational, leading, and supportive roles of standards. It is necessary to expand the industrial ecosystem. Focus on cultivating leading AI enterprises and support the specialized, refined, distinctive, and innovative development of small and medium-sized AI enterprises. Improve the AI open-source mechanism, accelerate the construction of high-level AI open-source communities, and create an open and shared open-source ecosystem. Enhance fiscal and tax policy support to guide increased investment from social capital. Continuously expand international cooperation in the artificial intelligence industry. It is essential to balance development and security. Strengthen governance safeguards for security, enhance risk assessment and response, advance breakthroughs in deep synthesis detection technologies, accelerate the formulation of management and service measures for AI ethics, and guide the healthy and orderly development of the industry. (Cailian Press)

[National Energy Administration: Organize the First Batch of Pilot Work for New-Type Power System Construction, Encourage Pilot Projects for Next-Generation Coal Power]The National Energy Administration has organized the first batch of pilot work for new-type power system construction. Focusing on cutting-edge directions related to new-type power systems, single-direction pilots will be conducted based on typical projects, while multi-direction comprehensive pilots will be carried out in typical cities to explore new technologies and models for building new-type power systems, aiming to achieve breakthroughs. Priority will be given to key areas, initially focusing on seven directions: grid-forming technology, system-friendly new energy power stations, smart microgrids, synergy between computing power and electricity, virtual power plants, large-scale high-proportion new energy transmission, and next-generation coal power. The approach will be tailored to local conditions, selecting suitable directions for pilot projects based on regional realities and reasonably determining their scale and scope.》Click for details

[CPCA: Preliminary Estimate Shows National Passenger NEV Wholesale Sales at 1.24 Million Units in May, Up 38% YoY]Based on preliminary monthly CPCA data, the national passenger NEV wholesale sales in May are estimated at 1.24 million units, up 38% YoY and 9% MoM. The cumulative wholesale sales from January to May are estimated at 5.22 million units, up 41% YoY.

On the US dollar:

Overnight, the US dollar index fell 0.48% to 98.79. Supported by a weaker dollar and soft US data, the market grappled with increasing economic uncertainties. The Institute for Supply Management (ISM) reported that its non-manufacturing PMI dropped to 49.9 last month, the lowest since June 2024, while ADP data showed the smallest increase in US private-sector jobs in over two years. All eyes are on Friday’s US nonfarm payrolls report for clues on the US Fed’s next move.

On other currencies:

In May 2025, the final eurozone composite PMI was revised up to 50.2, higher than the preliminary estimate of 49.5 but slightly below April’s 50.4. Although this marks the fifth consecutive month of expansion, overall growth remained marginal and the weakest since February. Manufacturing was the main driver of output growth, offsetting the first decline in services activity since November 2024. Among the four largest economies in the Eurozone, Italy and Spain achieved robust expansion, France approached stability, while Germany remained in contraction. Inflows of new business continued to decline, and job creation remained mild. The volume of outstanding work decreased at a mild pace. On the price front, input cost inflation slowed to a six-month low, while output charges rose only slightly, marking the weakest growth since October 2024. Meanwhile, business confidence improved for the first time since January 2025. (Huitong Finance)

Data:

Today, data including the global ANZ commodity price index annual rate for May, Australia's goods and services trade balance for April, Australia's export monthly rate for April, Australia's import monthly rate for April, China's Caixin Services PMI for May, Switzerland's unadjusted unemployment rate for May, Switzerland's seasonally adjusted unemployment rate for May, the global leading indicator for turning points in the industrial production cycle for May, the number of job cuts announced by US companies in May (Challenger report), the European Central Bank's (ECB) main refinancing rate for June, the ECB's deposit facility rate for June, the ECB's marginal lending facility rate for June, the US trade balance for April, the number of initial jobless claims in the US for the week ending May 31, the number of continuing jobless claims in the US for the week ending May 31, Canada's trade balance for April, Canada's IVEY seasonally adjusted PMI for May, Canada's IVEY unadjusted PMI for May, and the global supply chain pressure index for May will be released. Additionally, notable events include: the US Fed releasing the Beige Book on economic conditions; the ECB announcing its interest rate decision; and ECB President Christine Lagarde holding a press conference on monetary policy.

Crude Oil:

Both WTI and Brent crude oil futures fell, with WTI down 1.06% and Brent down 1.1%. Oil prices came under pressure due to unexpectedly large increases in US gasoline and diesel inventories, OPEC's plan to boost production leading to an expansion in fuel supply, and trade tensions casting a shadow over the energy demand outlook.

A report released by the US Energy Information Administration (EIA) showed that US gasoline inventories rose by 5.2 million barrels last week, compared to analysts' expectations of a 600,000-barrel increase. Distillate inventories increased by 4.2 million barrels, versus the expected 1 million-barrel rise. Crude oil inventories, however, fell by 4.3 million barrels, compared to analysts' forecasts of a 1 million-barrel decline.

OPEC oil-producing countries plan to increase production by 411,000 barrels per day in July, which also weighed on the market. Russia's oil and gas revenues fell by 35% in May, which may make Moscow more resistant to further OPEC production increases, as these moves would put pressure on crude oil prices. Additionally, some production operations in Canada that were shut down due to wildfires resumed on Wednesday. Wildfires have caused the country's production to decrease by approximately 344,000 barrels per day. (Webstock Inc.)