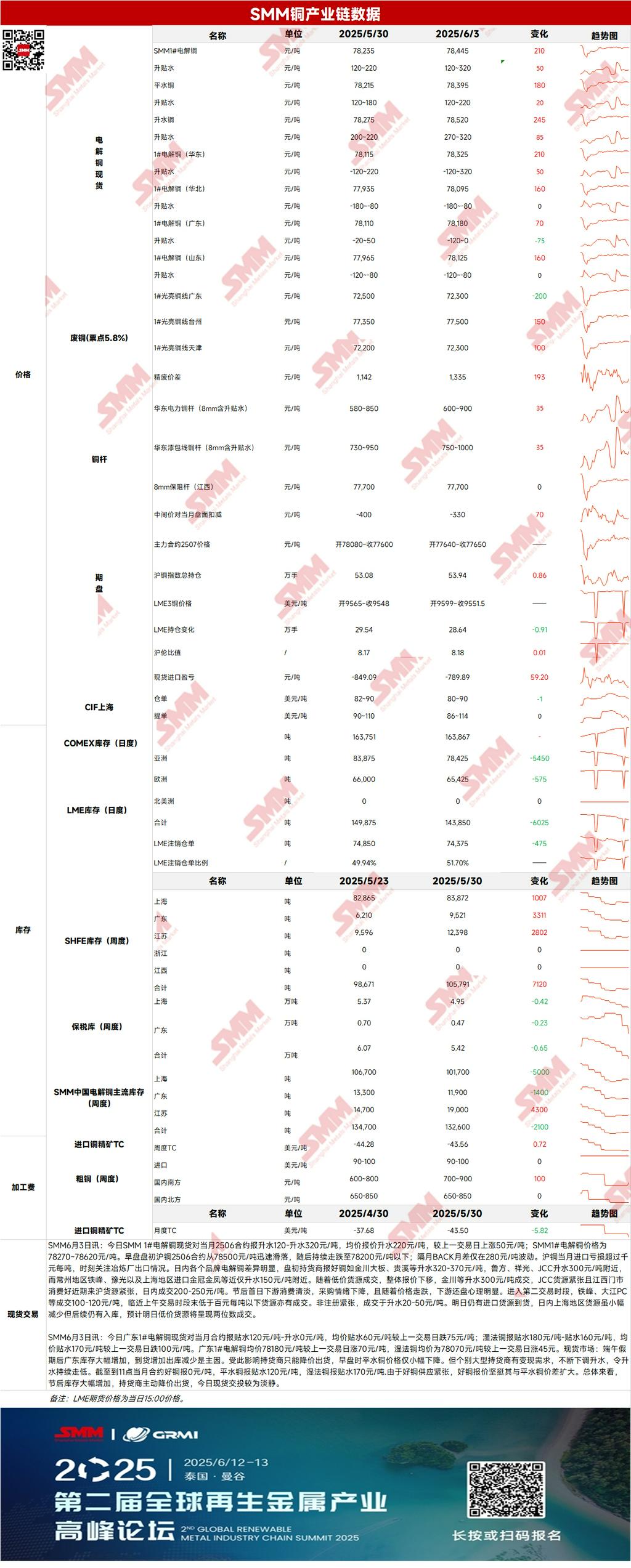

Futures Market: Overnight, LME copper opened at $9,566.5/mt, dipping to a low of $9,557.5/mt shortly after the open before fluctuating upward to a high of $9,648/mt during the session. It ended the day with narrow fluctuations, closing at $9,638.5/mt, up 0.24%. Trading volume reached 16,000 lots, and open interest stood at 287,000 lots. Overnight, the most-traded SHFE copper 2507 contract opened at and dipped to a low of 77,910 yuan/mt, surging straight to a high of 78,400 yuan/mt shortly after the open. It then maintained narrow fluctuations, eventually closing at 78,180 yuan/mt, up 0.5%. Trading volume reached 52,000 lots, and open interest stood at 187,000 lots.

[SMM Copper Morning Meeting Summary] News: (1) Peruvian mining officials stated on Tuesday that the country's copper production is expected to increase slightly to 2.8 million mt this year, with mining investments projected to reach at least $4.8 billion. Peru, the world's third-largest copper producer, produced approximately 2.7 million mt of copper in 2024, attracting $4.96 billion in investments in the key mining sector.

(2) According to Ivanhoe Mines: Kolwezi, Democratic Republic of the Congo – Ivanhoe Mines (TSX: IVN; OTCQX: IVPAF) announced on June 3 that following the suspension of underground mining operations at the Kamoa-Kakula Mine on May 20, 2025, senior management continues to work closely with a team of world-class geotechnical experts to safely and prudently restart mining operations. It is expected that underground mining operations in the Kamoa-Kakula West Zone will resume in late June, subject to the progress of dewatering efforts. The Kamoa-Kakula West Zone was not flooded and has a dewatering capacity of 1,000 liters per second.

Spot Market: (1) Shanghai: On June 3, spot copper cathode was quoted at a premium of 120-320 yuan/mt against the front-month 2506 contract, with an average premium of 220 yuan/mt, up 50 yuan/mt from the previous trading day. The SMM #1 copper cathode price was 78,270-78,620 yuan/mt. Early in the morning session, the SHFE copper 2506 contract slid rapidly from 78,500 yuan/mt, continuing to fall below 78,200 yuan/mt. The BACK spread between consecutive months fluctuated only by 280 yuan/mt. The import loss for SHFE copper in the front month exceeded 1,000 yuan/mt. Keep a close eye on smelter exports. There are still import arrivals scheduled for tomorrow. Although spot supplies in the Shanghai region decreased slightly today, there will be additional inflows subsequently. It is expected that low-priced spot supplies will see double-digit trading volumes tomorrow.

(2) Guangdong: On June 3, spot #1 copper cathode in Guangdong was quoted at a discount of 120 yuan/mt to a premium of 0 yuan/mt against the front-month contract, with an average discount of 60 yuan/mt, down 75 yuan/mt from the previous trading day. SX-EW copper was quoted at a discount of 180 yuan/mt to 160 yuan/mt, with an average discount of 170 yuan/mt, down 100 yuan/mt from the previous trading day. The average price of #1 copper cathode in Guangdong was 78,180 yuan/mt, up 70 yuan/mt from the previous trading day, while the average price of SX-EW copper was 78,070 yuan/mt, up 45 yuan/mt from the previous trading day. Overall, inventory levels surged after the holiday, prompting suppliers to actively lower prices to sell. Spot trades were relatively quiet today.

(3) Imported copper: On June 3, warrant prices ranged from US$82/mt to US$90/mt, with QP June, and the average price fell by US$3/mt from the previous trading day. B/L prices ranged from US$90/mt to US$110/mt, with QP June, and the average price fell by US$5/mt from the previous trading day. EQ copper (CIF B/L) prices ranged from US$50/mt to US$60/mt, with QP June, and the average price fell by US$12/mt from the previous trading day. Quotations referenced cargo arriving in early June. Overall, EQ copper prices fell sharply, and the market expects buying activity to pick up after the holiday. If the SHFE/LME price ratio gradually improves, Yangshan copper premiums will find support at low levels.

(4) Secondary copper: On June 3, the price of secondary copper raw materials fell by 200 yuan/mt MoM. Guangdong bare bright copper prices ranged from 72,200 yuan/mt to 72,400 yuan/mt, down 200 yuan/mt from the previous trading day. The price difference between copper cathode and copper scrap was 1,335 yuan/mt, up 193 yuan/mt MoM. The price difference between copper cathode rod and secondary copper rod was 1,080 yuan/mt. According to an SMM survey, copper prices fell sharply during the midday session. It was expected that secondary copper rod enterprises would face suppliers refusing to budge on prices or halting shipments. With copper prices trading sideways for an extended period, many secondary copper rod enterprises believe that the temporary easing of US-China trade tensions does not represent long-term stability. Policy uncertainties have led secondary copper rod enterprises to maintain a bearish outlook on copper prices in the near term.

(5) Inventory: On June 3, LME copper cathode inventories fell by 4,600 mt to 143,850 mt. On June 3, SHFE warrant inventories fell by 2,724 mt to 31,404 mt.

Price: On the macro front, US data released on Tuesday showed that job openings increased in April, but layoffs also rose. Amid growing tariff concerns, the labour market is cooling. Starting Wednesday, US tariffs on imported steel and aluminum will double to 50%. Trump hopes countries will submit their best offers in trade negotiations. Overall, the US dollar remains under pressure, which is bullish for copper prices. On the fundamental front, supply side, although cargo availability in Shanghai declined slightly today, there are still inbound shipments expected, and imported cargo is still scheduled to arrive tomorrow. There are significant differences in copper cathode premiums among various brands today, with large fluctuations in premiums for different brands. On the demand side, downstream consumption was sluggish on the first day after the holiday, and purchasing sentiment declined. As prices fell, downstream buyers became more price-sensitive. As of Monday, June 3, SMM copper inventories in major Chinese markets increased by 14,300 mt from before the holiday to 153,000 mt, up 32,900 mt from the previous low. Compared with inventory changes last Thursday, inventories increased in most regions across the country, with only a slight decline in Shanghai. On the price front, copper prices are expected to face limited upside today.

[The information provided is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make decisions cautiously and should not rely on this information as a substitute for independent judgment. Any decisions made by clients are not related to SMM.]