At the beginning of April, SHFE tin prices fell sharply under pressure due to the escalation of trade conflicts. However, as tariffs were suspended, tin prices rebounded, recovering previous losses and returning to levels before the supply disruptions of tin ore in the DRC. Nevertheless, the market reacted strongly to rumors last week about production resumptions and fee payments in the Wa region, causing tin prices to break through support levels and continue to weaken at the beginning of this week, with the most-traded contract falling below the 250,000 mt threshold. Currently, these market rumors remain unverified. According to SMM, few enterprises are paying fees to obtain mining licenses, with many adopting a wait-and-see attitude, and most major mining traders have not paid management fees. Moreover, the current inspections at the China-Myanmar border are stringent, and the entry procedures for most large-scale equipment and relevant mining personnel are complex. Therefore, the current pace of production resumptions in the Wa region may fall short of market expectations. So, does the current tin price still have the momentum to continue declining?

Tight Actual Supply of Tin Ore, with Increasing Expectations for Future Increases

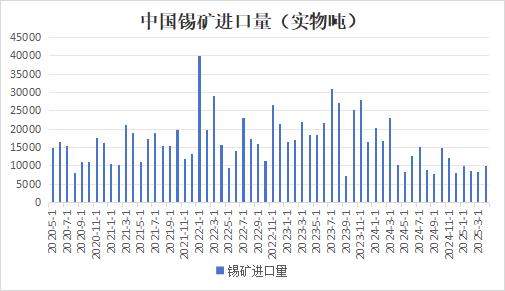

In recent years, speculation on SHFE tin has mainly revolved around supply, as tin is a relatively scarce metal with limited content in the Earth's crust and a high degree of supply concentration, primarily distributed in China, Indonesia, Myanmar, Australia, and other regions. After Myanmar suspended tin ore mining on August 1, 2023, global tin resources have been in a relatively tight supply situation. Consequently, the market is highly sensitive to supply-side information, with any slight changes triggering significant market fluctuations. In the early stages of Myanmar's mining ban, China's tin ore imports remained at a relatively high level due to the availability of ore inventory for export. However, as inventory was depleted, China's tin ore imports plummeted from Q2 last year, and the issue of tight domestic tin ore supply has become increasingly prominent.

During this period, Chinese enterprises actively sought alternative resources from other countries. However, due to limited global new tin ore discoveries in recent years, the tight resource situation has not been alleviated. Among them, the Bisie mine, owned by Alphamin in the DRC, is the largest mine in Africa and the third largest globally. The mine has two projects: the Mpama North project operates steadily, while the Mpama South project commenced production on May 17 last year, making it the largest among the newly commissioned projects last year. Tin ore from the DRC has also become an important source of tin ore imports for China, currently accounting for about 30%. Production at the Alphamin mine was suspended for over a month in March due to local armed conflicts but gradually resumed in early April. The production interruption at the Alphamin mine, which only recovered about 1,290 mt of tin metal, may result in a supply gap of approximately 2,000-3,000 mt. Currently, Alphamin has revised its tin production guidance for the 2025 fiscal year downward from 20,000 mt to 17,500 mt.

Since the beginning of this year, the resumption of tin ore production in Myanmar has gradually been put on the agenda. On February 26, the Wa State Industrial and Mineral Resources Administration issued the document "Procedures for Applying for Mining, Beneficiation Plant, and Prospecting Licenses," which explicitly stipulated the process for applying for licenses in mining areas. On the morning of April 23, 2025, the Wa State Industrial and Mineral Resources Administration held a special symposium on the resumption of production at the Mansang mine. The meeting announced relevant documents and clarified the work procedures. However, after the symposium, the authorities had not yet issued a clear signal for a full resumption of production. On May 27, market news emerged that the first batch of tin ore from Myanmar's Wa State had reportedly obtained export licenses, but the authenticity of the rumors was questionable. Even if production resumption were confirmed, the first batch of tin ore would not enter the market until at least the end of June.

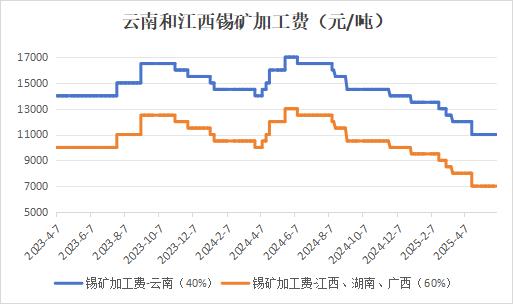

Currently, tin ore supply is tight, and domestic tin concentrate treatment charges (TCs) remain at historically low levels. As of May 30, the tin concentrate TC for 40% grade ore in Yunnan was 11,000 yuan/mt, and for 60% grade ore in Jiangxi, Guangxi, and Hunan was also 11,000 yuan/mt, approaching the cost line of smelters and severely squeezing profit margins.

The shortage of raw material supply has affected the production of smelters. According to SMM data based on market-adjusted processing figures, in May 2025, China's refined tin production decreased by 2.37% MoM and 11.24% YoY. The continuous tightening of the tin concentrate and scrap tin supply chains has imposed rigid constraints on capacity, leading to a slight decline in the overall operating rate of domestic smelters. As of May 30, the operating rates of refined tin smelters in Yunnan and Jiangxi, two major tin-producing provinces, remained at low levels, with a combined operating rate of 54.58%. Regionally, in Yunnan, the shortage of raw materials and cost pressures are intertwined. Raw material inventories at Yunnan smelters are generally below 30 days, with some enterprises facing inventory backlogs due to high-priced stockpiling in the early period. However, weak downstream demand has made it difficult to sell goods, resulting in sluggish spot premium transactions. Some smelters in core production areas such as Gejiu have entered seasonal maintenance or production cuts due to raw material shortages and cost pressures. In Jiangxi, since the beginning of the year, the local scrap tin recycling volume has consistently been below 70% of the annual average, mainly due to the US imposing high tariffs on Chinese electronics, leading to a contraction in solder export orders and a reduction in scrap sources. Some enterprises have been forced to implement long-term production cuts due to insufficient scrap, with some capacity potentially exiting the market permanently. In Inner Mongolia, production slightly rebounded in May due to production issues at captive mines, but it has not yet returned to previous levels. Production areas such as Anhui have continued to experience operating rates below expectations due to shortages of scrap and tin concentrates. Based on SMM estimates, refined tin production is expected to decrease by 4.58% MoM in June, with some smelters in Yunnan and Jiangxi planning to halt production for maintenance.

Overall, tin ore supply in June is unlikely to see significant recovery. However, the period of the tightest global tin supply is about to pass, and the market will enter a verification phase for the improvement of the supply-demand gap. Close attention should be paid to the return of tin ore from Africa and the resumption progress of tin ore production in Myanmar.

There is a lack of significant incremental demand in the downstream sector.

Global semiconductor sales exhibit cyclical changes. The current semiconductor cycle bottomed out in February 2023, with YoY growth in sales turning positive in November 2023. Since then, the growth rate has been climbing, but it gradually slowed down after October 2024. Currently, the absolute amount of global semiconductor sales remains at a high level. Sales began to pull back slightly from December 2024 and saw a slight MoM rebound in March 2025. This global semiconductor cycle is driven by AI computing power construction, primarily in advanced manufacturing processes. Therefore, the core beneficiaries are concentrated overseas, while domestic capacity is mainly in mature manufacturing processes, offering limited impetus. The downstream semiconductor industries in China are more concentrated in areas such as consumer electronics and automotive.

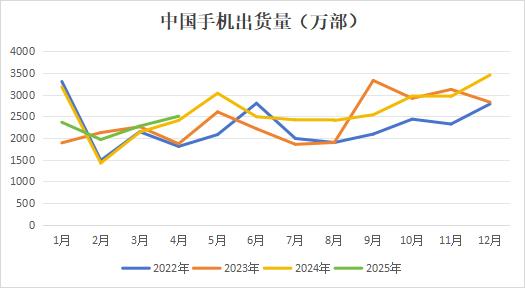

From January to April 2025, domestic mobile phone shipments reached 94.708 million units, up 3.5% YoY. Overall, China's policy subsidies have further boosted market consumption, and the Chinese smartphone industry has shown steady growth from January to April 2025. The recent 618 shopping festival has already kicked off and is expected to support stable end-use consumption electronics. However, the market is expected to gradually enter the off-season for demand in July and August. Enterprises may slow down their stockpiling pace, and it is anticipated that downstream demand for raw materials such as tin will also drop back slightly. Whether there will be an outperformance in demand this year remains to be seen, depending on whether AI blockbuster products emerge in the consumer electronics sector.

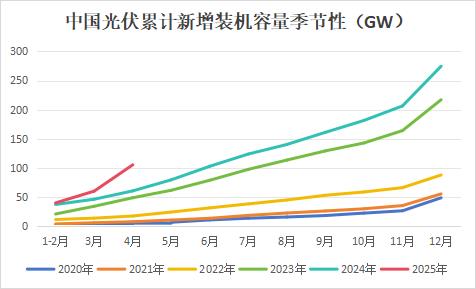

In recent years, the new demand for tin solder has mainly been reflected in PV solder, currently accounting for over 10%. According to data released by the National Energy Administration, the installed power generation capacity for solar energy from January to April 2025 was 990 million kW, up 47.7% YoY. The significant growth in new PV installed capacity is primarily driven by the installation rush driven by policy timelines. In January 2025, the National Energy Administration issued the "Administrative Measures for the Development and Construction of Distributed PV Power Generation," clarifying that April 30, 2025, is the demarcation point for the implementation of new and old policies. Existing projects that completed their filings before this date will still enjoy the original subsidy and grid connection policies, while new projects will fully implement market-based rules thereafter.

On February 9, 2025, the National Development and Reform Commission (NDRC) and the National Energy Administration jointly issued the "Notice on Deepening the Market-Oriented Reform of New Energy On-Grid Tariffs to Promote High-Quality Development of New Energy." Starting from May 31, 2025, incremental distributed PV projects will fully enter the market. All new projects will, in principle, have their entire electricity output traded in the power market, with electricity prices formed through market bidding, and subsidies will completely exit the historical stage. Meanwhile, a "price settlement mechanism for the sustainable development of new energy," namely, a "refund for excess, supplement for shortfall" differential settlement mechanism, has been established to stabilize revenue expectations.

To capitalize on the two major policy periods of "430" and "531," downstream enterprises initiated an installation rush, driving a significant YoY increase in domestic newly installed PV capacity in April. However, projects connected to the grid after May 31, 2025, are required to fully comply with the new regulations. It is expected that the growth rate of PV installation capacity will subsequently slow down, which will also drag down the demand for tin. Meanwhile, market consumption in traditional sectors such as tinplate and PVC heat stabilizers remains stable. Downstream enterprises are highly sensitive to price changes. Recently, with the decline in tin prices, market sentiment for stockpiling has improved, and downstream procurement demand has rebounded. However, finished product inventories in some markets remain at relatively high levels, ultimately limiting the boost to raw material procurement by downstream enterprises driven by growth in end-user market demand.

Overall, the increase in tin concentrates in June is expected to be relatively limited, so the supply will remain slightly tight in the short term. However, the supply of raw materials is expected to gradually improve, and the market will subsequently enter a verification period for the improvement of the supply-demand gap. Close attention should be paid to the return of tin ore from Africa and the production resumption progress of tin mines in Myanmar. On the demand side, the market is about to enter the off-season, with weak expectations for demand growth, making it difficult to effectively boost tin prices. Therefore, in the short term, under the expectation of increased supply, there may be downward pressure on the central tendency of the market, but constrained by the current situation where the shortage of tin ore has not significantly eased, market trends may fluctuate. However, from a long-term perspective, the AI industry cycle has not yet ended. If there is a surge in demand from AI end-users, it is expected to significantly drive up tin demand. At that time, the growth rate of supply may lag behind the resilience of demand, and the downside room for tin prices in the medium and long term will be limited. Nevertheless, there is still uncertainty in current trade policies, and caution should be exercised against significant disruptions to tin prices caused by macro factors. (Wenhua Comprehensive)

![The Most-Traded SHFE Tin Contract Opened Lower and Then Traded Stronger, Spot Market Recovers Amid Downtrend [SMM Tin Midday Review]](https://imgqn.smm.cn/usercenter/WWXJU20251217171753.jpg)

![The most-traded SHFE tin contract fluctuated rangebound during the night session, with downstream enterprises mostly following up with small-lot transactions. [SMM Tin Morning Brief]](https://imgqn.smm.cn/usercenter/bYFQn20251217171752.jpg)