On May 29, the 2025 SMM (2nd) Rare Earth Industry Forum, hosted by SMM Information & Technology Co., Ltd. (SMM), successfully concluded in Ningbo, Zhejiang Province!

The event was filled with highlights and valuable insights! The forum brought together representatives from relevant government departments, industry leaders, renowned academic experts, and seasoned investors to conduct comprehensive analyses and in-depth discussions on hot topics such as the future trends of the rare earth industry, innovation pathways for cutting-edge technologies, the evolution logic of the global market landscape, and strategies for optimizing the policy environment, all centered around the theme of rare earth industry innovation from a global perspective.

Participants focused on core issues such as the efficient utilization of rare earth resources and collaborative innovation across the industry chain. Through various formats including keynote speeches, closed-door meetings, and networking sessions, they jointly dissected the pain points of industrial development and explored solutions to bottlenecks such as optimizing capacity structure and upgrading green processes. The conference aimed to foster industry consensus, assist participants in accurately capturing growth opportunities in emerging sectors like new energy vehicles (NEVs) and robotics, and build an industry ecosystem driven by the synergy of "policy - technology - market." It sought to enable the industry to confidently address the challenges of global supply chain transformation and jointly propel the rare earth industry towards accelerated green, intelligent, and high-end development, shaping a new paradigm for high-quality development of the rare earth industry with international competitiveness.

》View the text coverage of this summit

Opening Remarks

SMM Executive Vice President Bai Zhou

Award Ceremony

Presentation of Awards for High-Quality Price Submitters of SMM Rare Earth Prices in 2025

》Click to view the list of enterprises

May 29

Guest Speaker Session

Speech Topic: Interpretation of China's Rare Earth Industry Data and Future Development Trends for 2024-2025

Guest Speaker: Jiawen Yang, Analyst, SMM Rare Earth Division

Analysis of Demand for Rare Earth Resources in 2024-2025E

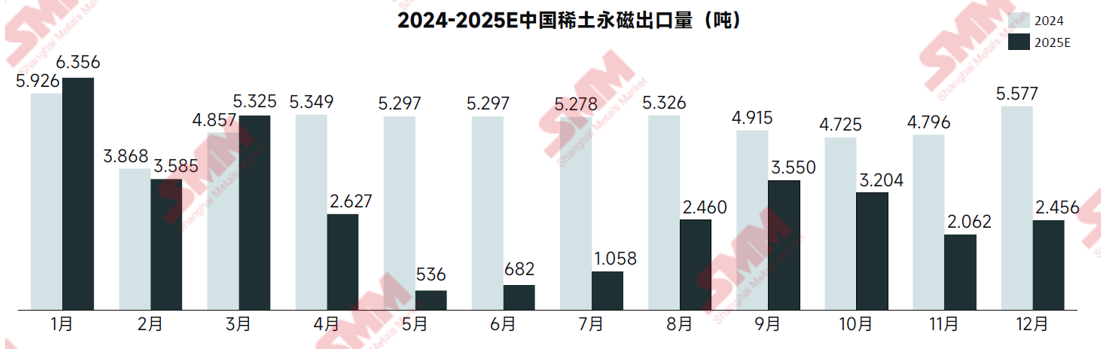

China's Rare Earth Exports

►SMM Analysis

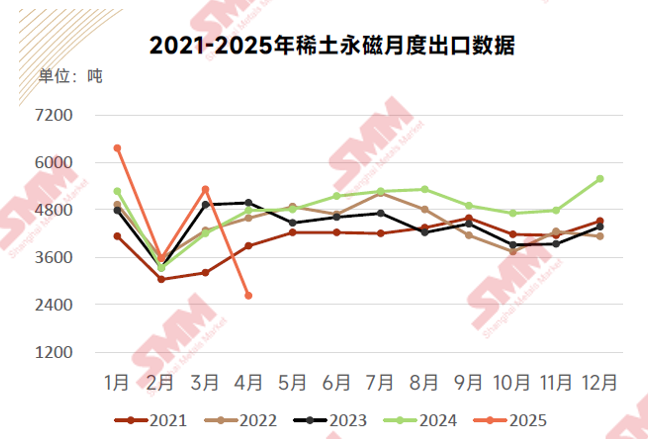

From January to April 2025, China's cumulative rare earth exports reached 18,962.3 mt, up 5.1% YoY. Currently, large magnetic material enterprises have gradually obtained export licenses, and it is expected that more export licenses for rare earths will be issued as time progresses.

On May 12, China and the United States reached an agreement, with the US side agreeing to suspend the implementation of a 24% tariff for an initial 90-day period, while reserving the right to impose the remaining 10% tariff on Chinese goods specified in Executive Order 14257 in accordance with regulations, and canceling the tariff hikes on these goods from April 8-9.

Downstream Demand for Pr-Nd Oxide

►SMM Analysis

In 2025, due to export restrictions on NdFeB magnetic materials, the overall downstream demand for Pr-Nd oxide throughout the year will show a downward trend, with May-June being the trough period for exports. However, the demand for Pr-Nd oxide from domestic end-user industries remains high, with the annual demand for Pr-Nd still showing a 5.4% increase compared to last year.

Currently, the end-use sector with the highest domestic demand for Pr-Nd oxide remains the NEV industry. The rising global EV penetration rate is driving demand for permanent magnet motors. The amount of NdFeB used per vehicle is approximately 2-5 kg, directly boosting Pr-Nd consumption.

Analysis of Rare Earth Resource Supply in 2024-2025E

It is expected that rare earth mining quotas will remain flat YoY in 2025

►SMM Analysis

Based on current market conditions, SMM expects rare earth mining quotas to reach 270,000 mt in 2025, remaining flat YoY. This includes 266,000 mt of rock-type rare earth ore and 19,000 mt of ion-adsorption type rare earth ore. Smelting and separation quotas will reach 340,000 mt, up 34% YoY.

From the perspective of smelting and separation, the "Administrative Measures for the Total Volume Control of Rare Earth Mining and Smelting and Separation (Provisional) (Public Consultation Draft)" clearly states that organizations and individuals without rare earth quotas are prohibited from engaging in rare earth mining and smelting and separation production activities. This means that the smelting and separation of imported ore will be included in the quota management scope.

Rare earth metal ore imports are expected to decline significantly YoY in 2025

►SMM Analysis

From January to April 2025, China's rare earth metal ore imports were 17,614 mt, down 5% YoY. In April, imports were 3,763 mt, up 18% MoM but down 24% YoY. In mid-to-late April, MP announced the cessation of rare earth ore exports to China, though 3,744 mt of rare earth metal ore had already entered China that month.

Almost all of China's imported rare earth metal ore comes from MP's mine in the US. Due to the local development of the US's own rare earth industry chain, rare earth metal ore imports from the US decreased to 55,000 mt in 2024. Based on the current expansion situation in the US, it is expected that these imports will continue to decline to 43,000 mt in 2025.

Unlisted rare earth oxide imports are expected to resume growth in 2025

►SMM Analysis

From January to April 2025, China's unlisted rare earth oxide imports were approximately 12,849 mt, down 30% YoY. In April, unlisted rare earth oxide imports were approximately 6,536 mt, up approximately 4% YoY and approximately 204% MoM.

In 2025, 70% of unlisted rare earth oxide imports will come from Myanmar. Due to local political and weather factors, the import situation of these rare earth mineral resources is unstable, and related news may also cause domestic oxide price fluctuations.

Mixed rare earth carbonate imports are expected to increase significantly YoY in 2025

Speech Topic: Analysis of the Rare Earth Industry Situation

Guest Speaker: Chen Zhanheng, Deputy Secretary General of the China Rare Earth Industry Association

Speech Topic: In-situ Short-process Regeneration Technology and Application of Sintered NdFeB Magnetic Sludge

Guest Speaker: Yue Ming, Professor at Beijing University of Technology

Yue Ming introduced: Sintered NdFeB permanent magnets are the strongest and most widely used type of permanent magnet material to date, playing an irreplaceable role in both defense and civilian high-tech fields. In recent years, the rapid development of emerging industries such as NEVs, unmanned aerial vehicles, and humanoid robots has actively driven the rapid growth and widespread application of sintered NdFeB. The rapid increase in demand for sintered NdFeB has, on the one hand, exerted pressure on the supply of rare earth mineral resources, and on the other hand, contributed to the accumulation of renewable rare earth resources.

To date, China and major developed countries worldwide have established strategic development plans for rare earth resources and gradually increased their investment in the R&D and industrialisation of technologies for the recycling of renewable rare earth resources. Among the various types of renewable rare earth resources, sintered NdFeB magnetic sludge has attracted significant attention. This typical large-scale renewable resource is characterized by its diverse types, complex composition systems, and the presence of toxic and hazardous components. Consequently, despite years of R&D efforts both domestically and overseas, outstanding issues such as low resource utilization rates, heavy environmental burdens, and high energy consumption remain unresolved. In response, research has proposed an in-situ short-process recycling technology for sintered NdFeB magnetic sludge based on classification-purification-deoxidation, significantly reducing recycling costs and environmental burdens. The promotion and application of this new technology are expected to facilitate the sound development of China's rare earth renewable resource industry and promote the strategy of a rare earth circular economy.

Speech Topic: Recent Developments in the Overseas Rare Earth Industry

Guest Speaker: Yan Wang, Deputy Director of the Information Center/Professor, Baotou Rare Earth Research Institute

Yan Wang stated that after Trump's return to the White House, his declarations of "buying Greenland," "merging the US and Canada," as well as the tariff wars, and the signing of a key minerals cooperation agreement between Ukraine and the US, which includes rare earths, have elevated the popularity of rare earths to unprecedented levels. Geopolitical conflicts have brought about rapid changes and uncertainties in the international rare earth industry. Guided by policies and supported by governments, the pace of constructing overseas rare earth industry chains is also accelerating: countries have increased the intensity of rare earth mineral exploration and mining to ensure future supply needs. Simultaneously, they have expedited the enhancement of rare earth separation capacity and further extended their layouts to the middle and lower reaches of the industry. This includes Lynas' expansion in Australia and its industrial planning in the US, the commissioning of MP Materials' separation line in the US and the operation of its rare earth metal and NdFeB lines, Neo Performance Materials' separation production and multi-point development of sintered and bonded magnets, and Solvay's plan to resume separation line production and its ambition to enter the NdFeB industry. These developments indicate the formation of a diversified supply landscape for rare earths worldwide and also remind China's rare earth industry of how to respond to the emergence of a diversified supply landscape. His report provides a brief introduction to the major international rare earth-related policies in recent years and the latest progress in overseas rare earth mining and separation, and discusses with the participants the potential impacts of the new overseas rare earth situation on China's rare earth industry.

Presentation Topic: Research Progress in Hot-Pressed and Hot-Deformed Rare Earth Permanent Magnet Materials

Guest Speaker: Xu Tang, Ningbo Institute of Materials Technology & Engineering, Chinese Academy of Sciences

Presentation Topic: Latest Technology and Application Market Outlook for Cerium-Containing Permanent Magnets

Guest Speaker: Minggang Zhu, Professor, China Iron & Steel Research Institute Group Co., Ltd.

Presentation Topic: Outlook and Technical Discussion on the EVTOL Propeller Motor Industry

Guest Speaker: Hongfei Cao, Chairman, Shanghai EVK Motor Technology Co., Ltd.

Presentation Topic: Industry Trends and Industry Chain Analysis of Humanoid Robots

Guest Speaker: Jinke Li, Executive Secretary General, China Mobile Robot Industry Alliance

Presentation Topic: Rare Earth & Wind Power: Contributing to Carbon Neutrality

Guest Speaker: Yazhou Gao, Director of Motor Technology Department, R&D Center, Goldwind Science&Technology Co., Ltd.

Development Trends in the Wind Power Industry

"Wind Power Industry Trends": The World's Wind Power Still Relies on China, Marching Boldly into the Carbon Neutrality Era

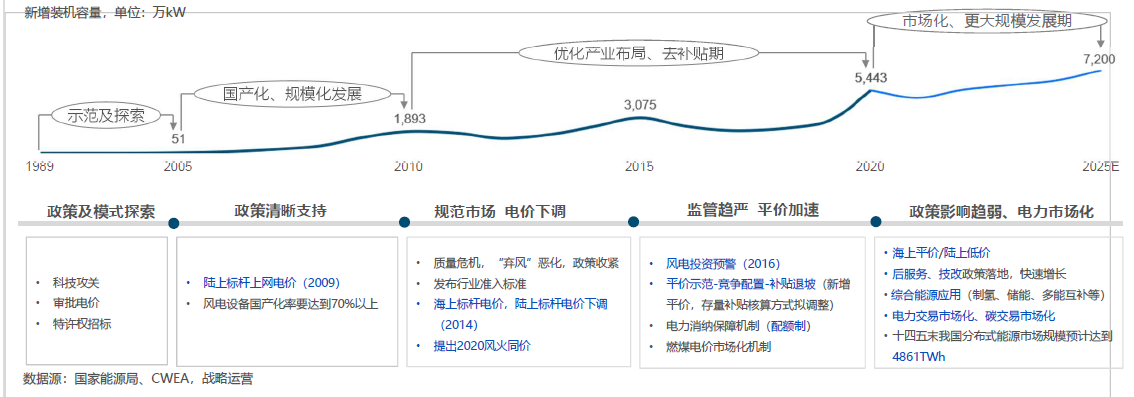

• With clear "dual carbon" goals, the wind power market is embracing a historic opportunity period. Cumulative new installations during the "14th Five-Year Plan" period will reach 250-300 million kW, an 80% increase compared to the "13th Five-Year Plan" period, with an average annual installation of 50-60 GW.

• By 2030, it will reach at least 800 million kW, and by 2060, at least 3 billion kW, indicating that wind power will maintain rapid and sustained development over the next 40 years!

"Wind Power Industry Trends": China's Wind and Solar Power Installations Surpass Thermal Power

In Q1 2025, China's combined new installations of wind and solar power reached 74.33 million kW, with cumulative installations reaching 1.482 billion kW (including 536 million kW of wind power and 946 million kW of solar power), surpassing thermal power installations (1.451 billion kW) for the first time. In the future, as new installations of wind and solar power continue to grow rapidly, it will become the norm for wind and solar power installations to exceed thermal power installations.

In Q1, the combined power generation of wind and solar power reached 536.4 billion kWh, accounting for 22.5% of the total electricity consumption in society, with non-fossil energy power generation accounting for 39.8%.

In Q1, the combined power generation of wind and solar power increased by 111 billion kWh compared to the same period last year, significantly exceeding the increase in total electricity consumption in society (58.2 billion kWh).

"Wind Power Industry Trends": Wind Power is Playing a Pivotal Role in the Social Economy

Annual output value is approximately 600 billion yuan; the number of employees is approximately 2.5 million.

Complete industry chain: covering wind resource assessment, wind farm development and construction, equipment manufacturing, technical services, testing and certification, investment and financing services, etc.

Giving back to related industries: Boosting the progress and breakthroughs of industries such as materials technology, testing and detection, and heavy-cargo transportation.

[Trends in the Wind Power Industry] China has become the world's largest manufacturing base for wind power equipment

China accounts for 50% of the global market share in the production of wind turbine parts and complete units, and 70% of the global market output for key parts and castings and forgings (e.g., generators, wheel hubs, frames, blades, gearboxes, bearings, etc.).

[Trends in the Wind Power Industry] Innovation in materials, technology, standards, and models becoming normalized

With the further reduction in the price of wind turbines, the industry is building a new technological system in the four areas of "wind" - "turbine" - "farm" - "grid," with technological advancements in new theories, new materials, new processes, new core components, and new architectures.

[Trends in the Wind Power Industry] Major trends in turbines: Large rotors, large capacity

•Major trends - large rotors and large capacity: With the continuous expansion of the scope of wind energy resource development and utilization in China, the development of low-wind-speed resources in the southeastern region of China has become an important trend. The technological development trend of turbines is also gradually showing a trend towards large rotors and large capacity in line with this demand.

》Rare Earths & Wind Power: Contributing to Carbon Neutrality [SMM Rare Earths Forum]

Speech Topic: Application and Industrial Production of Rare Earth Fluorides

Guest Speaker: Liang Xingfang, Vice President of Shandong Rare Earth Research Institute

Part 1: Characteristics and Main Applications of Rare Earth Fluorides

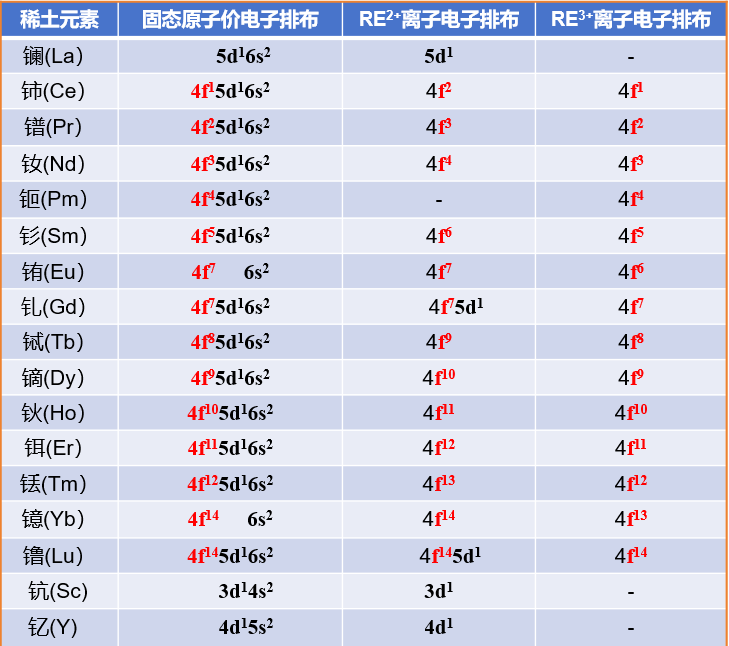

Structural Characteristics of Rare Earth Elements

1. Scandium, yttrium, and the lanthanides have the same outermost electron structure, resulting in similar chemical properties.

2. The number of electrons in the 4f layer ranges from 0 to 14 from lanthanum to lutetium.

3. The 4f orbital is shielded by outer layers, leading to energy transition differences and structural differences when electrons are lost during reactions, resulting in different characteristics.

4. Fluorine is one of the elements with the strongest oxidizing properties.

Rare earth fluorides possess the stability of strong ionic bonds

Rare earth fluorides are compounds containing rare earth elements and fluorine

1. Binary rare earth fluorides: Direct combination of rare earth elements with fluorine;

2. Complex rare earth fluorides: Doped with other elements to possess specific functions;

3. Nanoscale rare earth fluorides: Possess special size and surface effects.

Binary rare earth fluorides

High melting point; low vapor pressure; chemically stable, insoluble in water; outstanding optical properties, capable of reducing excited-state energy loss and significantly improving upconversion luminescence efficiency.

Rare earth fluorides are important materials with unique magnetic, optical, and electrical properties

1. Optical materials: Laser crystal materials, optical functional materials, fluorescent materials, and optical fiber materials;

2. Catalytic materials: Petroleum cracking and environmental protection catalytic materials;

3. Additive materials for polishing materials, ceramic materials, lubricants, and anti-corrosion materials;

4. Raw and auxiliary materials for the preparation of rare earth metals or alloys.

Raw and auxiliary materials for the production of rare earth metals and alloys through fused salt electrolysis and calcium thermal reduction methods.

The application in high-end industries and the demand from traditional industries have promoted the development of the rare earth fluoride industry.

It also elaborates on the characteristics and main applications of binary rare earth fluorides.

Main applications of rare earth fluorides in the rare earth industry

1. Raw and auxiliary materials for the production of rare earth metals and alloys

Auxiliary materials for fused salt electrolysis process: electrolyte REF3+LiF

Raw materials for calcium thermal reduction process: REF3+Ca

China's NdFeB production in 2024 was approximately 300,000 mt

To produce raw materials such as Pr-Nd alloy, Nd, Ce, Gd-Fe alloy, and Dy-Fe alloy, over 5,000 mt of rare earth fluorides are required.

Speech topic: Current Development Status and Prospects of China's NdFeB Magnetic Materials Industry

Guest speaker: Zhanpeng Su, Analyst, SMM Rare Earth Division

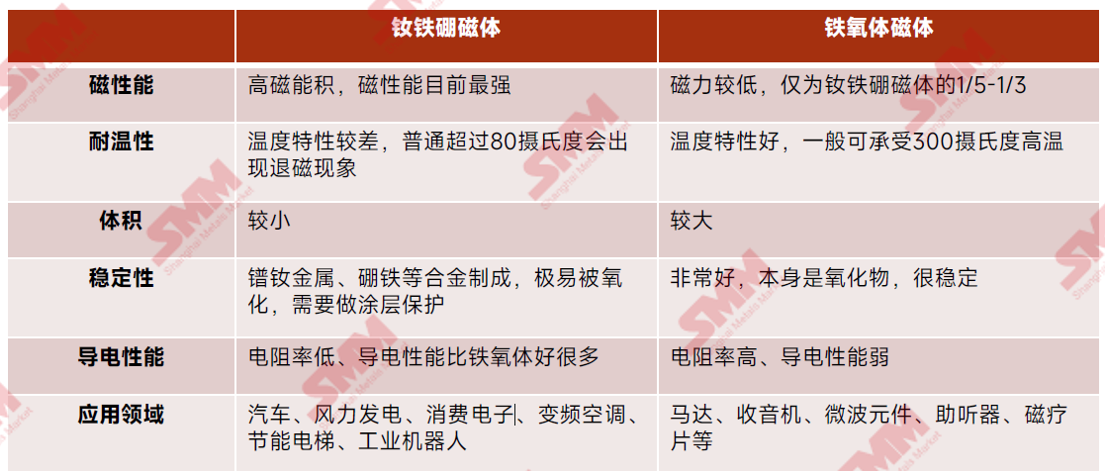

NdFeB permanent magnets dominate the permanent magnet materials market, with high-performance NdFeB leading the industry's development.

Overview of magnetic materials:Currently, magnetic materials are mainly divided into two categories: permanent magnet materials and soft magnetic materials. Permanent magnet materials possess persistent magnetism and are the most widely used magnetic materials. Among them, NdFeB alloys and ferrite permanent magnet materials hold significant positions in the technological field. On the other hand, although soft magnetic materials can be magnetized under the influence of an external magnetic field, their magnetism is unstable and easily lost due to external factors.

Compared to ferrites, NdFeB exhibits higher magnetic energy product and coercivity, enabling it to provide stronger magnetic performance in a smaller volume. Meanwhile, NdFeB permanent magnets, with their high energy density and stability, are irreplaceable in high-end industrial, new energy, and consumer electronics applications, while ferrites, due to their performance limitations, are mostly used in low-power, low-cost, low and mid-end applications.

Overview of the end-use market for NdFeB permanent magnets

The end-use market for NdFeB permanent magnets is mainly concentrated in six major fields: consumer electronics, NEVs, clean energy, new-type fields, energy-efficient elevators, and energy-efficient home appliances. Among them, emerging markets such as NEVs, energy-efficient home appliances, wind power generation, and industrial robots account for the majority of the market share.

In 2025, the increasing penetration rate of NEVs, the rise of emerging economies such as humanoid robots and the low-altitude economy, and the national subsidy policies in the home appliances and consumer electronics sectors will continue to inject new vitality into the future market of NdFeB. However, due to adjustments in the real estate market and technological breakthroughs in wind power raw materials, the demand for NdFeB in energy-efficient elevators and wind power generation has decreased.

Analysis and Forecast of NdFeB End-Use Demand

Rare Earth Permanent Magnet Exports Shrank 45% YoY in April 2025 Due to Export Controls

In April 2025, rare earth permanent magnet exports were affected by export controls, shrinking 45% YoY and 51% MoM. However, cumulative exports from January to April increased 2% YoY.

The newly implemented export control measures in April had a certain impact on export trade, necessitating improvements in recent export conditions. With the smooth resumption of exports of magnetic materials not containing medium-heavy rare earth and the sequential approval of licenses for those containing medium-heavy rare earth, rare earth permanent magnet exports are expected to recover, though it will be difficult to restore the original export volume in the short term.

It is forecasted that China's NEV production will reach 17.89 million units in 2025, up approximately 29% YoY.

According to data from the China Association of Automobile Manufacturers (CAAM), in 2024, NEV production and sales were 12.888 million units and 12.866 million units, respectively, up 34.4% and 35.5% YoY. China's NEV market continued to grow in 2024, with new vehicle sales accounting for 40.9% of total new vehicle sales. NdFeB demand was 57,000 mt, up 38% YoY.

In 2025, NEV policies will feature "central coordination + local refinement," promoting market penetration through consumption subsidies, technological support, and pilot programs in public sectors. NEV production will continue to show a rapid growth trend. China's NEV production is expected to reach 17.89 million units in 2025, up approximately 29% YoY, with market penetration expected to exceed 55%. Total NdFeB demand will reach 75,000 mt.

It is forecasted that China's new wind power installations will reach 87 GW in 2025, up 8% YoY.

According to statistics from the National Energy Administration, in 2024, China's new wind power installations were 80.454 GW, up 6% YoY, with NdFeB demand at 9,735 mt, a 21% decrease in demand growth YoY. Due to cost constraints, the penetration rate of direct-drive motors has declined year by year, leading to a decrease in NdFeB demand for China's wind power installations in 2024.

As a key end-use sector for rare earth applications, although the growth rate of rare earth demand in the wind power industry has slowed recently, it remains a major driver of sustained rare earth demand growth in the long term. It is forecasted that China's new wind power installations will reach 87 GW in 2025, up 9% YoY, with NdFeB demand reaching 8,341 mt.

It is forecasted that China's air conditioner production will reach 320 million units in 2025, up 18% YoY.

According to data from the National Bureau of Statistics (NBS), in 2024, China's air conditioner production reached 270 million units, up 10% YoY, with NdFeB demand at 21,000 mt, a 26% increase in demand growth YoY. Since September 2024, following the government's introduction of the "trade-in" subsidy policy, and the overlapping events such as "Double 11" and year-end promotions in the market, the home appliance market has shown an upward trend.

In 2025, driven by the recovery of market demand, technological innovation, and policy support, the home appliance industry has demonstrated a positive development momentum. The national trade-in subsidy has continued to increase significantly, driving a notable rise in the production and sales volume of the air conditioning industry. It is expected that in 2025, air conditioning production will increase to 330 million units, up 25% YoY, which will bring about a demand of 26,000 mt for NdFeB.

Highlights of the Conference

At this point,the 2025 SMM (2nd) Rare Earth Industry Forumhas come to a successful conclusion!

Thank you for your attention and support for this summit. We look forward to seeing you again next year~

》Click to view the special report on the 2025 SMM (2nd) Rare Earth Industry Forum