SMM News on May 29: After the opening of the morning session on May 29, lithium carbonate futures prices continued to decline, with the main lithium carbonate contract even dropping to 58,460 yuan/mt at one point during the session, breaching the 60,000 yuan/mt threshold again after the previous trading day and hitting a new all-time low since its listing. In terms of contracts for the same product, multiple contracts such as lithium carbonate 2510, 2511, and 2506 all fell below the 60,000 yuan/mt threshold.

In terms of spot quotes, according to SMM's spot quotes, the lowest spot quote for battery-grade lithium carbonate officially fell below the 60,000 yuan/mt threshold today. As of the latest quote on May 29,battery-grade lithium carbonatespot quotes fell to the range of 59,500-62,300 yuan/mt, with an average price of 60,900 yuan/mt, a decrease of 3,900 yuan/mt from 64,800 yuan/mt on May 15, representing a decline of 6.02%.

》Click to view SMM's spot quotes for new energy products

Regarding the reasons for the continuous decline in lithium carbonate futures and spot prices, SMM believes it is mainly related to the ongoing supply surplus in the current lithium carbonate market. Against this backdrop of surplus, there is a lack of upward momentum for short-term lithium carbonate price increases. From the perspective of supply and demand, on the supply side, according to SMM, upstream lithium chemical producers frequently reported news of maintenance and production cuts last week. In response to these market developments, some enterprises have indeed implemented maintenance and shutdown plans, while the maintenance schedules of others remain to be further determined. Overall, although the reduction in output due to smelter maintenance has exerted some pressure on the total output of lithium carbonate, the overall supply of lithium carbonate remains at a relatively high level.

In contrast to the high supply levels, the demand side for lithium carbonate has shown relatively stable performance. Although there was a certain increase in downstream demand in May, the growth was relatively limited. Moreover, due to the significant proportion of customer-supplied and long-term agreement volumes currently, with the continuous decline in lithium carbonate prices, downstream material plants are generally adopting a cautious wait-and-see attitude, making it difficult for spot orders to support market confidence.

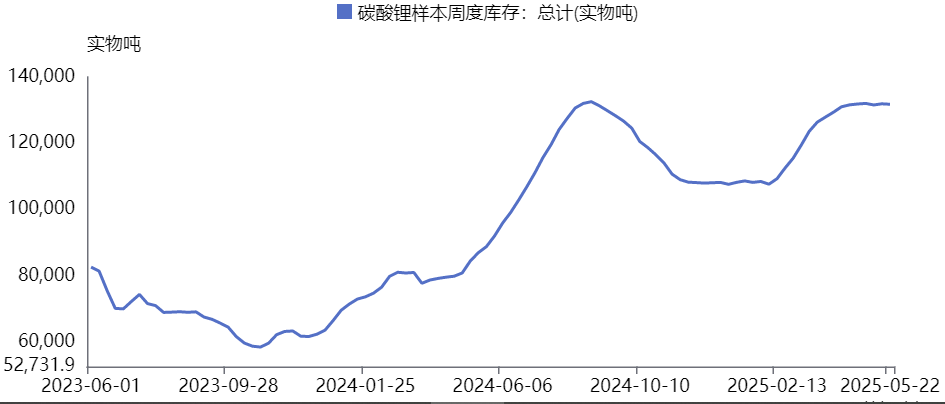

In terms of inventory, domestic weekly lithium carbonate sample inventory has continued to climb since February. As of May 22, the weekly lithium carbonate sample inventory had reached 131,779 mt, hitting a new high since August 8, 2024. The sustained high inventory levels have also put pressure on lithium carbonate prices.

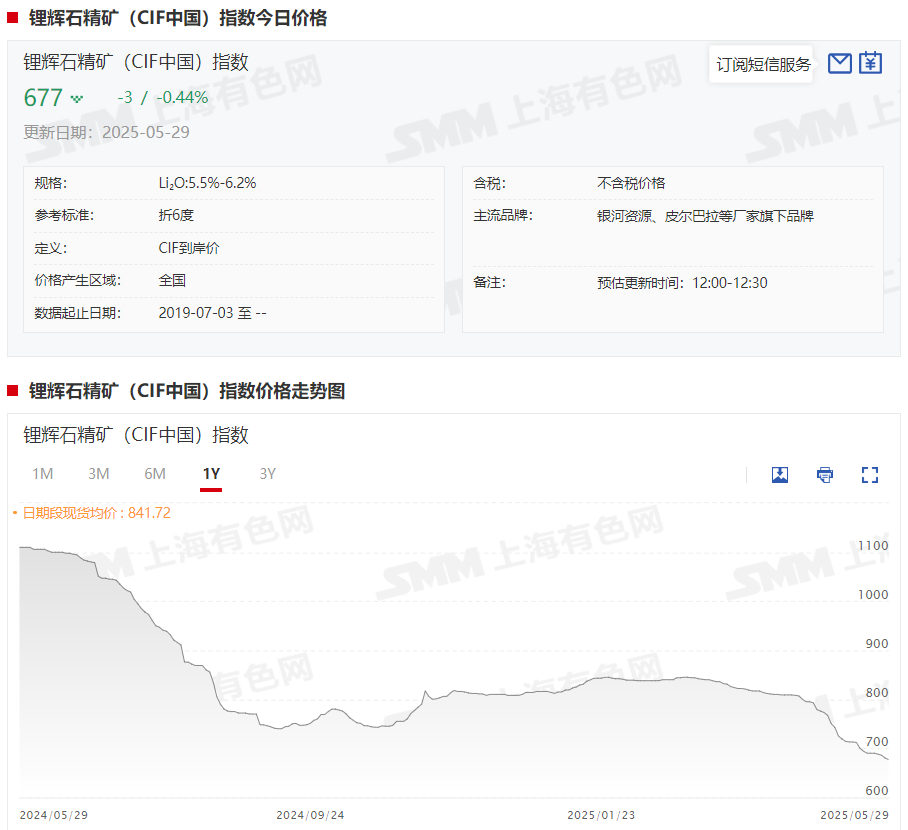

On the cost side, lithium ore prices have continued to decline recently. As of May 29, the spot quote for spodumene concentrates (CIF China) had fallen to $677/mt, a decrease of $168/mt from the low of $845/mt on March 5, representing a decline of 19.88%. Currently, no mines have announced production cuts or shutdowns. The decline in lithium ore prices has weakened the cost support for lithium carbonate, further pushing down lithium carbonate prices.

》Click to view SMM's spot quotes for new energy products

Therefore, overall, amid the backdrop of a supply surplus, SMM expects the lithium carbonate market to remain weak in the short term, with prices likely to continue facing downward pressure.

Yu Shuo, an analyst at Chuangyuan Futures, estimated that with the release of capacity in regions such as Africa and Brazil, coupled with significant cost reductions in Australian ore in Q1, the costs of major operating mines in Australia have now all fallen below $600/mt. He stated that during the current decline in lithium carbonate prices, there has been no reduction in ore production, and miners have shown a strong willingness to sell. Meanwhile, there has been a substantial inventory buildup of domestic lithium ore, leading to a smooth decline in ore prices, which has driven down the price of lithium carbonate.

Yang Fei, a senior researcher in the Non-Ferrous Metals and New Materials Group at CITIC Futures, also noted that recently, after lithium ore prices fell below $700/mt, the rate of decline has slowed somewhat. However, the current ore prices have not yet reached the cost levels of the mines, and no production cuts have been observed. He indicated that in the future, ore prices may continue to test the cost support near $600/mt, which will further push down the price of lithium carbonate.

Chuangyuan Futures analyst Yu Shuo predicts that in the short term, lithium carbonate prices may exhibit a volatile downward trend. If spodumene prices fall below $600/mt, it could trigger a halt in Australian ore production, forming a temporary bottom. Attention should be paid to signals of production cuts from the ore sector. However, production cuts from the ore sector are only a signal of a halt in the decline. The long-term market pattern of oversupply will limit the rebound potential of lithium carbonate prices. Only a joint production cut by miners or unexpectedly strong policy stimulus could potentially trigger a significant temporary rebound in lithium carbonate futures.

Institutional Commentary

Industrial Futures stated that currently, the operating enthusiasm for spodumene production lines is low, while salt lake capacity continues to increase. The extent of supply tightening is relatively limited, and the efficiency of demand transmission is declining at each level. Although NEV retail sales have benefited from policy stimulus, inventory accumulation and poor sales of battery cells in the intermediate links, as well as limited increases in production schedules for cathode material enterprises, have resulted in weak purchase willingness for raw materials by downstream buyers. In-plant inventory at smelters has reached a new high, and the loose fundamental situation continues to exert downward pressure on lithium prices.

Dongwu Futures stated that currently, lithium carbonate supply remains high, with inventory approaching the peak level of 2024. Meanwhile, ore prices have softened, and quotes for Australian concentrates have been lowered, weakening the expected cost support. Looking ahead, the oversupply pattern of lithium carbonate remains unchanged, and the market will continue to operate weakly.

Yide Futures stated that on the supply side, the CIF quotes for Australian ore continue to fall to $630/mt, while African ore prices have dropped to $614/mt. Port inventory of lithium ore has increased, and the planned production of lithium carbonate nationwide has declined MoM, with the latest weekly production data showing a decrease. Spodumene smelting has reduced, while lepidolite and salt lake production have increased. On the demand side, the production schedules for cathode materials have increased MoM for both ternary and LFP. From the current production schedule, the supply and demand fundamentals still maintain a surplus pattern. In terms of inventory, the latest weekly inventory decreased by 141 mt. A breakdown shows that the increase was concentrated in smelters, while downstream and trader inventories were drawn down. In the short term, with the combination of front-loaded consumption and collapsing costs, the futures market continues to search for a bottom. From a long-term industry perspective, the market requires a more thorough exit of resources from the market. In terms of investment strategy, domestic smelting production cuts have increased, but there has been no action on the resource side. The weakness in fundamentals remains unchanged, and the futures market continues to break through support levels and fall in search of a bottom. Long-term attention should be paid to whether there will be production cuts on the resource side amid low prices.

Guoyuan Futures stated that the most-traded lithium carbonate futures contract continued its weak trend in May. At the beginning of the month, downstream orders for May fell short of expectations, with limited WoW growth in production schedules. Coupled with the release of incremental supply following the implementation of lithium resource projects in Q1, the surplus pattern of lithium carbonate persisted, and lithium prices fell sharply. In mid-month, amid fluctuations in Sino-US tariff policies, market sentiment improved, driving a slight rebound in lithium carbonate prices. However, due to the unreversed surplus pattern in the fundamentals of lithium carbonate, after the short-term rebound, lithium prices returned to an in-the-doldrums trend. Overall, it is expected that the supply increment of lithium carbonate will be significant in June, and the cost range will shift downward. On the demand side, the decline in battery cell demand is dragging down the trend, with a clear downward trajectory in cathode production schedules. In terms of inventory, there is limited room for lithium carbonate production cuts, and it is expected that lithium carbonate inventory levels will fluctuate at highs. Overall, with supply remaining high and demand contracting, it is expected that lithium carbonate prices will maintain a fluctuating bottom-building trend in June.