On May 29, at the 2025 SMM (2nd) Rare Earth Industry Forum hosted by SMM Information & Technology Co., Ltd. (SMM), Yang Jiawen, an analyst from SMM's Rare Earth Division, shared insights on the topic of "Interpretation and Outlook of China's Rare Earth Industry Data for 2024-2025."

Analysis of Rare Earth Resource Demand in 2024-2025E

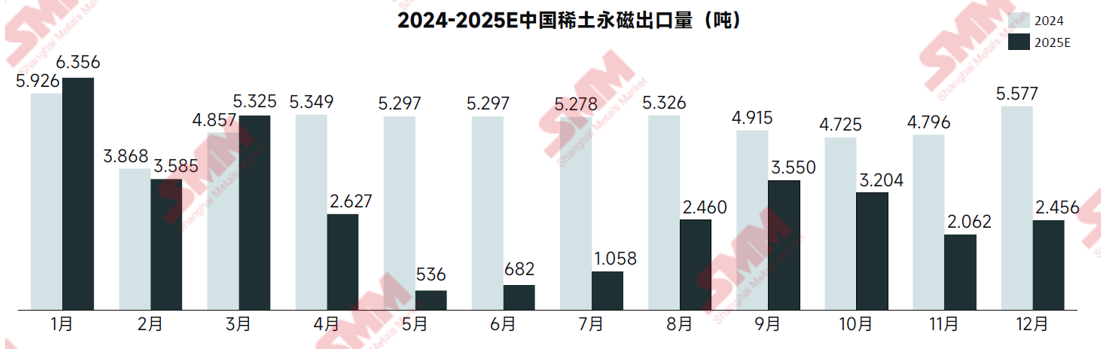

China's Rare Earth Exports

►SMM Analysis

From January to April 2025, China's cumulative rare earth exports reached 18,962.3 mt, up 5.1% YoY. Currently, large magnetic material enterprises have gradually obtained export licenses, and it is expected that the release of rare earth export licenses will further accelerate over time.

On May 12, China and the United States reached an agreement, with the US agreeing to suspend the implementation of a 24% tariff for an initial 90-day period, while reserving the right to impose the remaining 10% tariff on Chinese goods specified in Executive Order 14257 in accordance with regulations, and canceling the tariff hikes on these goods from April 8-9.

Downstream Demand for Pr-Nd Oxide

►SMM Analysis

In 2025, due to restrictions on NdFeB magnetic material exports, the overall downstream demand for Pr-Nd oxide throughout the year will show a downward trend, with May-June being the low point for exports. However, domestic end-user industries still maintain a relatively high demand for Pr-Nd oxide, with annual Pr-Nd demand expected to increase by 5.4% YoY.

Currently, the largest end-use sector for domestic Pr-Nd oxide demand remains the NEV industry. The rising global EV penetration rate is driving demand for permanent magnet motors. The amount of NdFeB used per vehicle is approximately 2-5 kg, directly boosting Pr-Nd consumption.

Analysis of Rare Earth Resource Supply in 2024-2025E

It is expected that rare earth mining quotas will remain flat YoY in 2025

►SMM Analysis

Based on an analysis of current market conditions, SMM expects that rare earth mining quotas in 2025 will reach 270,000 mt, remaining flat YoY. This includes 266,000 mt of rock-type rare earth ore and 19,000 mt of ion-adsorption type rare earth ore. Smelting and separation quotas will reach 340,000 mt, up 34% YoY.

From the perspective of smelting and separation, the "Interim Measures for the Administration of Total Volume Control of Rare Earth Mining and Smelting and Separation (Draft for Public Comment)" clearly states that organizations and individuals without rare earth quotas are prohibited from engaging in rare earth mining and smelting and separation production activities. This means that the smelting and separation of imported ore will be included in the quota management scope.

Rare Earth Metal Ore Imports in 2025 May Decline Significantly YoY

►SMM Analysis

From January to April 2025, China's rare earth metal ore imports amounted to 17,614 mt, down 5% YoY. In April, imports reached 3,763 mt, up 18% MoM but down 24% YoY. In mid-to-late April, MP announced that it would halt rare earth ore exports to China, yet 3,744 mt of rare earth metal ore had already entered China that month.

Almost all of China's imported rare earth metal ore originates from MP's mine in the US. As the US develops its own rare earth industry chain, rare earth metal ore imports from the US declined to 55,000 mt in 2024. Based on the current expansion plans in the US, this volume is expected to further decrease to 43,000 mt in 2025.

Unlisted rare earth oxide imports in China resume growth in 2025

►SMM Analysis

From January to April 2025, China's unlisted rare earth oxide imports reached approximately 12,849 mt, marking a 30% YoY decline. In April alone, imports were about 6,536 mt, up roughly 4% YoY and approximately 204% MoM.

In 2025, 70% of China's unlisted rare earth oxide imports originated from Myanmar. Due to local political and weather factors, the stability of these rare earth mineral resource imports is uncertain, and related news can cause fluctuations in domestic oxide prices.

China's mixed rare earth carbonate imports see significant YoY growth in 2025

►SMM Analysis

From January to April 2025, China imported 3,412 mt of mixed rare earth carbonate, a 30% YoY increase. In April, imports were 1,144 mt, down 26% MoM but up 173% YoY. Due to policy advancements in Malaysia and the launch of new rare earth mining projects, mixed rare earth carbonate imports are expected to increase significantly YoY in 2025.

It is reported that the Malaysian authorities aim for the rare earth industry to contribute approximately US$2.2 billion to the country's GDP by 2025 and attract investments from China and the US to jointly establish an integrated rare earth industry chain.

China's thorium ore sand imports see a significant YoY increase in 2025

►SMM Analysis

From January to April 2025, cumulative imports of thorium ore sand and its concentrates reached 48,501 mt, up only 1% YoY. Imports in the same period amounted to 21,366 mt, a 146% YoY increase, primarily sourced from South Africa.

It is understood that due to the reduction in MP's mine output in the US, some companies have opted to import more monazite to fill the gap in light rare earth ore supply. It is projected that China's total thorium ore sand imports will reach 90,171 mt in 2025, an 86% YoY increase.

Pr-Nd supply slightly decreases in 2025, with a notable increase in the proportion of recycled output

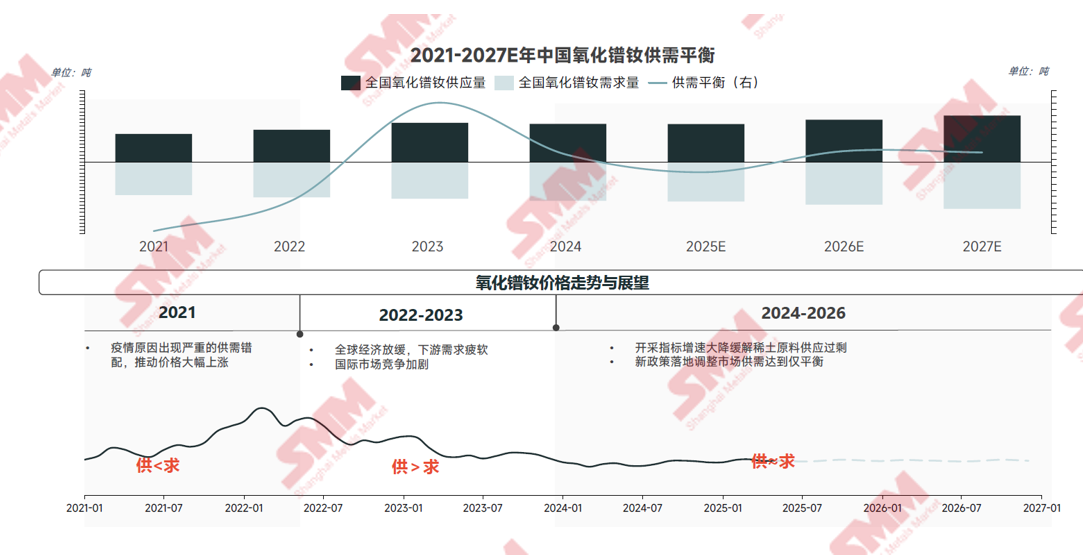

Supply-demand balance and prices of Pr-Nd oxide from 2024 to 2025E

The supply-demand pattern of Pr-Nd oxide is expected to remain relatively balanced from 2025 to 2027

This analysis combines data on China's national Pr-Nd oxide supply, national Pr-Nd oxide demand, and the supply-demand balance of Pr-Nd oxide in China from 2021 to 2027E.

In 2025, the overall supply of Pr-Nd oxide is expected to be tight, with a supply gap of approximately 3,000 mt.

In 2025, the overall supply of Pr-Nd oxide is expected to be tight. From January to February, during the Chinese New Year period, the operating rate of end-use industries is low, and downstream demand is relatively weak during this time.

Price Review and Forecast of Pr-Nd Oxide and Pr-Nd Alloy from 2025 to 2026

►SMM Analysis

Considering the above, in 2025, the final year of the "14th Five-Year Plan," the development of various downstream sectors in the rare earth industry is expected to accelerate, with humanoid robots and aircraft expected to become new growth points for downstream demand. Rare earth mining quotas are also expected to increase slightly to meet the growing downstream demand for rare earths.

Guided by national policies, the domestic supply of rare earth raw materials is expected to become more standardized and stable, and the supply-demand pattern of the entire rare earth industry is expected to become more balanced. It is anticipated that rare earth prices will generally fluctuate upward in 2025.

》Click to view the special report on the 2025 SMM (2nd) Rare Earth Industry Forum