The record of investor relations activities announced by Yunnan Copper on May 25 showed the following:

I. Brief Introduction to the Restructuring Plan

On May 24, the company disclosed relevant announcements, including the "Proposal for the Issuance of Shares to Purchase Assets and Raise Supporting Funds, as Well as Related Party Transactions." The company intends to purchase a 40% stake in Liangshan Mining held by Yunnan Copper Group through the issuance of shares. It also plans to raise supporting funds by issuing shares to Chalco Group and China Copper (with Chalco Group subscribing for no more than 1 billion yuan and China Copper subscribing for no more than 500 million yuan), which are intended to be used for the construction of the Hongnipo copper mine mining and beneficiation project of the target company and to supplement the working capital of the publicly listed firm. In addition, the company's controlling shareholder, Yunnan Copper Group, based on its confidence in the future development prospects of the publicly listed firm and its high recognition of the company's value, voluntarily extends the lock-up period for the newly issued shares of the publicly listed firm acquired through this transaction, beyond the lock-up period stipulated in relevant laws and regulations such as the "Administrative Measures for Restructuring": the shares shall not be transferred within 60 months from the date of the completion of the share issuance.

The target company of this transaction, Liangshan Mining, is mainly engaged in the mining, beneficiation, and smelting of metal ores such as copper. Before this transaction, the company already held a 20% stake in Liangshan Mining. After acquiring an additional 40% stake in Liangshan Mining through this transaction, Liangshan Mining will become a controlling subsidiary of the publicly listed firm, fully leveraging the business synergies between the company and the target company. Through this transaction, the company conducts industry consolidation, effectively strengthening its resource reserves and capacity layout, further promoting the development of its main business, enhancing the scale and quality of the publicly listed firm's business, and improving its sustainable operating capabilities and core competitiveness. After the completion of this transaction, the company will obtain controlling rights in Liangshan Mining and raise supporting funds, with its assets, revenue, and profit scales expected to increase.

At the same time, there are uncertainties regarding whether this transaction can obtain the aforementioned approvals, reviews, or registration agreements, as well as the final timing of such approvals. Investors are reminded to pay attention to investment risks.

II. Q&A Session

1. Please introduce the purpose of the company's proposed issuance of shares to purchase a 40% stake in Liangshan Mining held by Yunnan Copper Group.

Yunnan Copper introduced: Liangshan Mining is engaged in the mining, beneficiation, and smelting of metal ores such as copper, which constitutes horizontal competition with Yunnan Copper. By acquiring the 40% stake in Liangshan Mining held by its controlling shareholder, Yunnan Copper Group, the company can further resolve horizontal competition and ensure the faithful implementation of relevant commitments. Meanwhile, Liangshan Mining has obvious resource advantages, a solid profit foundation, and a return on net assets higher than the industry average. After the completion of the Hongnipo copper mine, its scale will reach that of a medium-to-large copper mine, further enhancing its profitability. After the injection of Liangshan Mining into Yunnan Copper, it can effectively increase the copper resource entitlement of the publicly listed firm, enhance the overall asset and profit scale as well as the industry position of the publicly listed firm, facilitate the publicly listed firm to fully leverage business synergies, strengthen the reserve of high-quality resources and capacity layout, enhance comprehensive strength and core competitiveness, and promote the high-quality development of the publicly listed firm. In addition, this acquisition is a specific measure taken by the company to implement the relevant opinions of the SASAC of the State Council on improving and strengthening the market value management of listed firms controlled by central state-owned enterprises, and to carry out M&A and restructuring activities that are conducive to enhancing the investment value of listed firms, which is beneficial for safeguarding the rights and interests of the listed firm and all its shareholders.

2. Please ask the company to introduce the basic situation of Liangshan Mining.

Introduction by Yunnan Copper: The main business of Liangshan Mining is the mining, beneficiation, and smelting of metal ores such as copper. It is a copper resource production and smelting enterprise that spans the copper mining, beneficiation, and smelting industries and covers copper, iron, and sulphuric acid products.

Liangshan Mining possesses high-quality copper resources such as the Lala Copper Mine and the Hongnipo Copper Mine. Currently, it can produce approximately 13,000 mt of copper concentrates, 119,000 mt of copper anodes, and 400,000 mt of industrial sulphuric acid annually.

3. What are the main profit models of Liangshan Mining?

Introduction by Yunnan Copper: Liangshan Mining primarily achieves profitability by mining and beneficiating its own metal ore resources such as copper, as well as by smelting self-produced and externally purchased copper concentrates to form products such as copper anodes, iron ore concentrates, and industrial sulphuric acid for sale.

4. What competitive advantages does Liangshan Mining have in terms of costs and overall production and operation?

Introduction by Yunnan Copper: Liangshan Mining boasts rich experience in mine and smelting management, as well as advanced production technologies and process equipment conditions for the mining, beneficiation, and smelting of metals such as copper. The copper mining costs of the mines owned by Liangshan Mining are relatively low, giving it good cost competitiveness. The selling prices of sulphuric acid in south-west China, where Liangshan Mining is located, are also relatively favourable. Meanwhile, it can also be observed that as of the end of March 2025, the high-quality copper ore resources held by Liangshan Mining, including the Hongnipo Copper Mine, Lala Copper Mine, and Hailin Copper Mine, had a retained copper metal content of 779,700 mt, with an average copper grade of 1.16%, which is higher than the current average copper grade of 0.38% of Yunnan Copper. Among them, the Lala Copper Mine has been in operation for many years, with stable copper concentrate output. The Hongnipo Copper Mine is currently under construction, with a total identified resource reserve of 41.606 million mt of ore, an average copper grade of 1.42%, and a copper metal content of 592,900 mt. Upon completion of the project, it will effectively increase the self-sufficiency rate of resources in the smelting process. In addition, Liangshan Mining won the exploration and prospecting rights for the Hailin Copper Mine in Huili City, Sichuan Province, through auction in 2024, with a mining area of 48.34 square kilometers, further enhancing the resource reserve potential of Liangshan Mining.

5. How is the construction progress of the Hongnipo Project of Liangshan Mining?

Yunnan Copper introduced: The Hongnipo copper mine is currently under construction. The total identified ore reserves amount to 41.606 million mt, with an average copper grade of 1.42% and a copper metal content of 592,900 mt. The company will closely monitor the project's progress and fulfill its information disclosure obligations in strict compliance with relevant regulations such as the "SZSE Listing Rules". Please stay tuned for the company's announcements.

According to the announcement of the "Plan for Yunnan Copper Co., Ltd. to Issue Shares to Purchase Assets and Raise Supporting Funds, as well as Related Party Transactions (Summary)" previously released by the company, the impact of this transaction on the publicly listed firm is as follows:

(I) Impact on the Main Business of the Publicly Listed Firm Before this transaction, the main business of the publicly listed firm covered copper exploration, mining, beneficiation, smelting, extraction and processing of precious metals and rare scattered metals, sulfur chemical engineering, and trading. It is an important production site for copper, gold, silver, and sulfur chemical engineering in China, and has established a relatively complete industry chain in the copper and related non-ferrous metals sectors, making it a copper enterprise with profound industry experience. The target company of this transaction, Liangshan Mining, is mainly engaged in the mining, beneficiation, and smelting of metal ores such as copper. Before this transaction, the publicly listed firm already held a 20% stake in Liangshan Mining. After acquiring an additional 40% stake in Liangshan Mining through this transaction, Liangshan Mining will become a controlled subsidiary of the publicly listed firm, fully leveraging the business synergies between the publicly listed firm and the target company. Through this transaction, the publicly listed firm will achieve effective enhancement in resource reserves and capacity layout, further promoting the development of its main business, improving the scale and quality of its business, and enhancing its sustainable operating capabilities and core competitiveness.

(II) Impact on the Shareholding Structure of the Publicly Listed Firm Before and after this transaction, there will be no changes to the controlling shareholder or actual controller of the publicly listed firm; this transaction will not result in a change of control over the publicly listed firm. As of the signing date of this plan summary, the audit and evaluation work for the target assets involved in this transaction have not been completed, and the transaction price has not yet been determined. Therefore, the specific changes in the shareholding structure of the publicly listed firm before and after this transaction cannot be accurately calculated at this time. The company will conduct a detailed calculation of the shareholding structure of the publicly listed firm after the completion of the transaction once the pricing of the target assets is determined, and disclose it in the restructuring report.

(III) Impact on the Main Financial Indicators of the Publicly Listed Firm After the completion of this transaction, the publicly listed firm will acquire controlling interest in Liangshan Mining and raise supporting funds, which is expected to increase the scale of its assets, revenue, and profits. As of the signing date of this plan summary, the audit and valuation of the underlying assets involved in this transaction have not yet been completed. Therefore, the specific changes in the key financial indicators of the publicly listed firm before and after this transaction cannot be accurately calculated. The company will conduct detailed calculations of the key financial indicators of the publicly listed firm after the completion of the transaction, once the relevant financial data for this transaction have been finalized, and disclose them in the restructuring report.

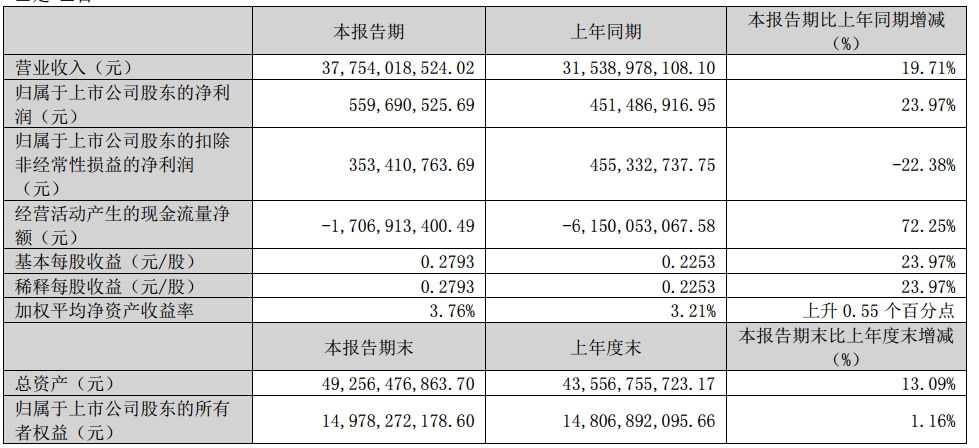

Yunnan Copper's Q1 report shows that in the first quarter of this year, the company achieved operating revenue of RMB 37.75 billion, up 19.7% YoY; and net profit attributable to the parent company of RMB 560 million, up 24% YoY. The company's report for the first quarter of 2025 indicates that its main businesses include the production and sales of copper, the refining of gold and silver, and the production of sulphuric acid. Yunnan Copper's Q1 report shows that in the first quarter of 2025, the company produced 348,900 mt of copper cathode, up 48.15% YoY; 5.8 mt of gold, up 95.63% YoY; 128.48 mt of silver, up 54.31% YoY; 1.3872 million mt of sulphuric acid, up 23.61% YoY; and 13,900 mt of copper in copper concentrates, down 15% YoY.

According to the record of Yunnan Copper's investor relations activities on March 26, 2025, as announced by Yunnan Copper (Series 1: Interpretation Meeting for the 2024 Annual Report): In 2024, Yunnan Copper adhered to the guidance of Party building, continued to strive, and forged ahead, fully implementing the decisions and deployments of the company's Party committee and board of directors. It overcame unfavourable factors such as a significant decline in TC and the shutdown of the old facilities at Southwest Copper, maintaining a stable operating situation. The company produced 1.206 million mt of copper cathode, 12.71 mt of gold, 348.99 mt of silver, and 4.8286 million mt of sulphuric acid throughout the year. As of year-end 2024, its total assets amounted to RMB 43.557 billion, with an asset-liability ratio of 57.66%. It achieved operating revenue of RMB 178.012 billion, total profit of RMB 2.316 billion, net profit attributable to the publicly listed firm of RMB 1.265 billion, and a basic earnings per share of RMB 0.6312. The company intends to distribute a cash dividend of RMB 2.4 (tax included) for every 10 shares to all shareholders, without converting capital reserves into share capital.

In its 2024 annual report, Yunnan Copper introduced its main businesses, which encompass the exploration, mining, and smelting of copper, the extraction and processing of precious metals and rare scattered metals, sulphur chemical engineering, and trading. It is an important production site for copper, gold, silver, and sulphur chemical engineering in China, having established a relatively complete industry chain in the copper and related non-ferrous metal fields, and is a copper enterprise with profound industry experience. The company's main products include copper cathode, gold, silver, industrial sulphuric acid, molybdenum, platinum, palladium, selenium, tellurium, rhenium, etc., with an annual production capacity of 1.4 million mt of copper cathode. The company's main products are manufactured in accordance with the standards set by the International Organization for Standardization (ISO) and operate effectively under the international ISO9001 quality management system, ensuring strict quality control over the products. The company's main product, copper cathode, is widely used in electrical, light industry, machinery manufacturing, construction, national defense, and other fields; gold and silver are used in finance, jewelry, electronic materials, etc.; industrial sulfuric acid is used as a raw material for chemical products and in other sectors of the national economy. The company's "Tiefeng" brand copper cathode is registered at the Shanghai Futures Exchange and the London Metal Exchange; "Tiefeng" brand gold is registered at the Shanghai Gold Exchange and the Shanghai Futures Exchange; and "Tiefeng" brand silver is registered at the Shanghai Gold Exchange, the Shanghai Futures Exchange, and the London Bullion Market Association.

When analyzing the company's core competitiveness, Yunnan Copper Science & Technology Development Co., Ltd. mentioned that its abundant resource reserves are one of its core strengths: the company attaches great importance to the replacement of mine resources, increasing capital investment to carry out comprehensive geological studies of various mining areas, as well as exploration and prospecting work in the deep and peripheral areas of mines. The company's main mines, including the Pulang Copper Mine, Dahongshan Copper Mine, and Yangla Copper Mine, are primarily located in the Sanjiang Metallogenic Belt, which boasts favorable metallogenic geological conditions and potential for further prospecting. In 2024, the company invested 65 million yuan in exploration activities, conducting multiple mineral exploration projects and exploration and prospecting work in the deep and peripheral areas of mines. It added 91,800 mt of inferred and above copper metal resources, achieving its annual target and realizing four consecutive years of annual reserve growth exceeding the output and consumption of mines. By the end of 2024, the company had 964 million mt of copper ore reserves and 3.6509 million mt of copper metal reserves, with an average copper grade of 0.38%. Among them, Diqing Nonferrous Metals had 846 million mt of copper ore reserves and 2.8037 million mt of copper metal reserves, with an average copper grade of 0.33%.

Regarding the company's future development outlook, it stated in its 2024 annual report: Yunnan Copper Science & Technology Development Co., Ltd. adheres to the guidance of Xi Jinping Thought on Socialism with Chinese Characteristics for a New Era, thoroughly studies and implements the spirit of the 20th CPC National Congress and the second and third plenary sessions of the 20th CPC Central Committee, upholds the Party's leadership, strengthens Party building, focuses on "digital and intelligent transformation, expanding resources, refining mines, optimizing smelting, solidifying recycling (of copper), and meticulously managing rare and scattered (metals)", adheres to goal-oriented, problem-oriented, and result-oriented approaches, and meticulously implements various tasks in production, operation, reform, and development to make new contributions to building a world-class copper company. In 2025, the company will closely focus on key tasks, prioritize profits, base itself on production volume, emphasize cost control, and prioritize safety. It will ensure effective implementation and the comprehensive achievement of annual goals and tasks, high-quality completion of the objectives and tasks outlined in the 14th Five-Year Plan, and lay a solid foundation for a good start to the 15th Five-Year Plan.

The 2025 financial budget plan released by Yunnan Copper on March 26 shows the following production plans for the company's main products in 2025: The company expects to produce 54,600 mt of copper in copper concentrates, 1.52 million mt of copper cathode, 16 mt of gold, 680 mt of silver, and 5.364 million mt of sulphuric acid throughout the year. The investment plan for 2025 is 1.617 billion yuan, covering fixed asset investments, digital projects, and geological exploration projects.

Guosen Securities' research report on Yunnan Copper points out: In terms of production, the company's copper concentrate production in 2024, based on consolidated financial statements, was 54,800 mt, a decrease of 10,000 mt YoY, due to a decline in output from the Pulang copper mine, the company's main mine. The attributable output was 57,800 mt, a decrease of 11.6% YoY. The consolidated copper cathode production in 2024 was 1.206 million mt, a decrease of 12.6% YoY, mainly due to a 235,000 mt reduction in output from Xinan Copper's relocation. Southeast Copper's electrolysis quality and efficiency improvement project was completed, with copper cathode production reaching a record high of 470,000 mt. The smelting business is under short-term pressure but is expected to improve in the long term. This year, the long-term contract TC for copper concentrates is only $21.25/mt, the lowest in history, and spot TCs have frequently dropped below zero, putting significant pressure on copper smelters. However, from a long-term perspective, most of China's large listed copper smelters are state-owned enterprises with strong risk resistance capabilities. Their smelting technology is globally leading, and their smelting costs are on the left side of the global cost curve, allowing them to maintain certain profits even under extremely low TCs. In the long term, they will benefit from the exit of global copper smelting capacity. Relevant national departments have issued documents to strictly control the new capacity of copper smelting, indicating a positive long-term outlook for the industry. Leveraging the high-growth cycle of the copper industry in recent years, the company has improved its asset quality. As the only listed copper platform under the Chalco Group, the injection of high-quality assets from its major shareholder is expected. Although the copper smelting business is under short-term pressure, the national policy to strictly control new capacity and the company's benefits from the exit of global copper smelting capacity indicate a positive long-term outlook for the industry. Maintain an "Outperform" rating. Risk warnings: Risk of copper price decline, risk of decline in copper concentrate TCs.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)