Zijin Mining announced in the evening of May 23 that multiple mine tremors had occurred in succession at the Kakula ore block of the Kamoa-Kakula copper mine operated by the company in recent days, with multiple roof falls and rib spalling incidents reported in the eastern section of the mine. The cause of the tremors remains unknown. Following a decision by the management of Kamoa Copper, underground operations in the affected area have been suspended, and relevant personnel and some equipment have been evacuated from the underground working face. As of now, no casualties have been reported. The company attaches great importance to this mine tremor incident and has organized an internal expert team to rush to the site. Together with the management and technical team of Kamoa Copper, and with the assistance of external third-party expert teams if necessary, the focus will be on re-evaluating and reassessing the early-stage mining methods, backfilling plans, hydrological control measures, and full life cycle production schedules. A comprehensive and systematic investigation into the causes of the mine tremors will be conducted, and a management and technical improvement plan will be developed and implemented.

According to Zijin Mining's announcement, due to the impact of the mine tremors, the Phase I and Phase II beneficiation plants of the Kamoa-Kakula copper mine will temporarily operate at a reduced capacity, processing ore from surface ore stockpiles. As of April 30, 2025, approximately 3.8 million mt of ore had been stockpiled on the surface, with an average copper grade of approximately 3.2%. The Phase III beneficiation plant of the Kamoa-Kakula copper mine and the underground mining activities within the Kamoa ore block have not been affected.

The Kamoa-Kakula copper mine achieved a copper production of 437,000 mt in 2024, with a planned copper production of 520,000 mt to 580,000 mt for 2025.The company holds a 44.45% equity interest in the project (including the equity interest corresponding to the company's stake in Ivanhoe Mines).It is expected that the recent mine tremors will adversely affect the realization of the Kamoa-Kakula copper mine's annual planned production.The specific extent of the impact will be further evaluated based on the investigation results, and the company will provide timely updates in its periodic reports or interim announcements. Kamoa Copper is a joint venture of the company. In 2024, the Kamoa-Kakula copper mine contributed 1.72 billion yuan to the company's net profit attributable to shareholders, accounting for approximately 5.37% of the company's net profit attributable to shareholders for the year.

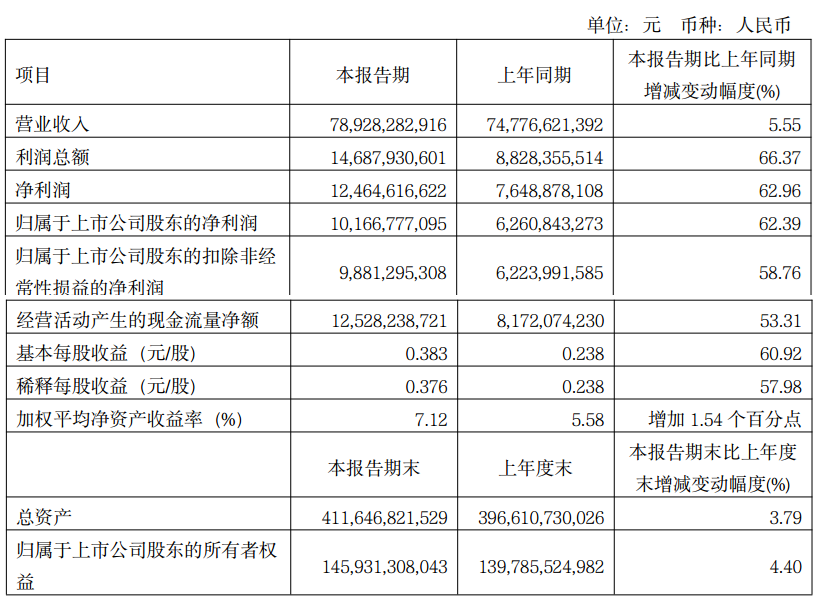

Zijin Mining previously disclosed its Q1 2025 report, showing that the company achieved a total operating revenue of 78.928 billion yuan, up 5.55% YoY, and a net profit attributable to shareholders of 10.167 billion yuan, up 62.39% YoY. Regarding the reasons for the increase in net profit, Zijin Mining stated that, compared with the same period last year, the company's major accounting data and financial indicators all increased by more than 50%, primarily due to the steady improvement in the company's production and operation management capabilities, which led to an increase in the production of major mineral products. Meanwhile, the company further enhanced its ability to assess the metal market, fully benefiting from the gains brought about by rising metal prices.

According to Zijin Mining's Q1 report on key production and operation data: From January to March 2025, the company's gold production from mines increased by 13% YoY, copper production from mines increased by 9% YoY, and zinc production from mines decreased by 10% YoY. It achieved operating revenue of 78.928 billion yuan, up 6% YoY, and net profit attributable to shareholders of 10.167 billion yuan, up 62% YoY. The gross profit margin of mining enterprises was 59.94%, representing a year-on-year increase of 5.44 percentage points. Compared with Q4 2024 on a QoQ basis, in Q1 2025, gold production from mines increased by 2% QoQ, copper production from mines increased by 3% QoQ, and zinc production from mines decreased by 9% QoQ. It achieved operating revenue of 78.928 billion yuan, up 8% QoQ, and net profit attributable to shareholders of 10.167 billion yuan, up 32% QoQ. The gross profit margin of mining enterprises in Q1 2025 was 59.94%, representing a quarter-on-quarter increase of 1.23 percentage points. During the reporting period, the company's unit sales cost of mineral products increased, which was attributed to a decline in grade, an increase in transportation distance, and a rise in the stripping ratio of some open-pit mines.

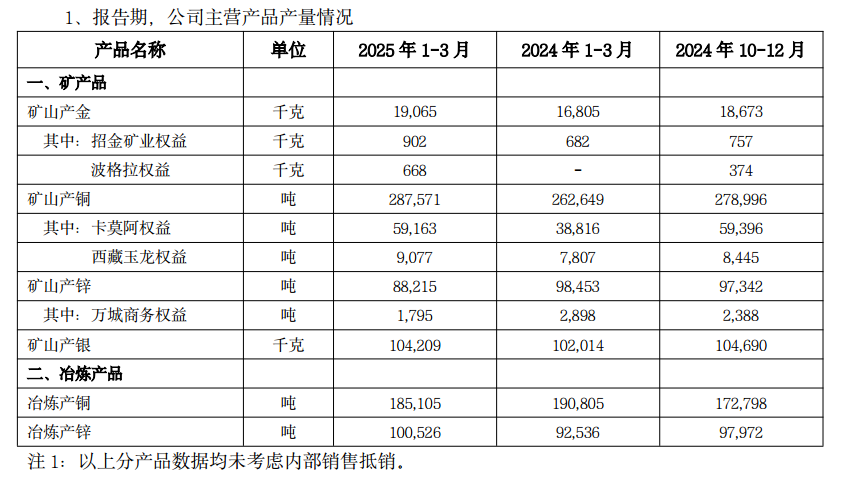

The following table presents the key production and financial indicators by product for the period from January to March 2025, the same period last year, and Q4 2024.

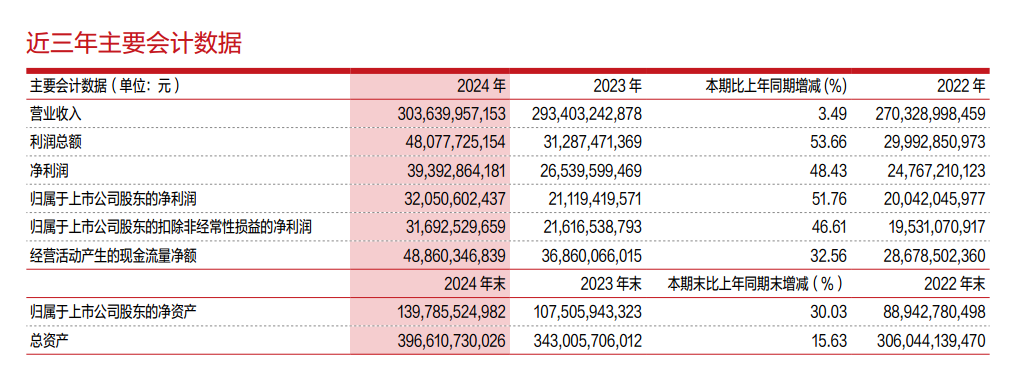

Zijin Mining's 2024 annual report shows that in 2024, the company's revenue was 303.640 billion yuan, up 3% YoY, and net profit attributable to shareholders of publicly listed firms was 32.051 billion yuan, up 51.76% YoY.

Zijin Mining's 2024 annual report indicates that in 2024, the company's resource volume and production of its main mineral products increased year after year, with both volume and price rising. Copper production from mines exceeded the 1 million mt milestone and continued to grow, while gold production from mines increased rapidly. The company achieved annual production of 1.07 million mt of copper, 73 mt of gold, 450,000 mt of zinc (lead), and 436 mt of silver from mines. Among these, the YoY growth rates of copper and gold production from mines were 6% and 8%, respectively. Despite the general cost pressure in the global mining industry, Zijin Mining reshaped its comparative advantage of low cost and high efficiency, effectively curbing the upward trend in costs. The sales costs of copper concentrates and gold concentrates decreased by 4.3% and 0.43% QoQ, respectively, remaining at a low level in the global mining industry. Key economic indicators reached new highs, demonstrating strong profitability. During the reporting period, the company achieved earnings before interest, taxes, depreciation, and amortization (EBITDA) of 63.2 billion yuan, total profit of 48.1 billion yuan, and net profit attributable to shareholders of 32.1 billion yuan, representing significant YoY increases of 36%, 54%, and 52%, respectively. The net cash flow generated from operating activities was 48.9 billion yuan, up 33% YoY, indicating robust and ample cash flow. At the end of the period, total assets were 396.6 billion yuan, including 139.8 billion yuan of net assets attributable to shareholders, representing increases of 16% and 30%, respectively, compared to the beginning of the period. The asset-liability ratio decreased to 55%, indicating a more optimized asset structure.

In its 2024 annual report, Zijin Mining outlined its production plans for key mineral products in 2025:1.15 million mt of copper, 85 mt of gold, 440,000 mt of zinc (lead), 40,000 mt of lithium carbonate equivalent, 450 mt of silver, and 10,000 mt of molybdenum from mines. Given the complex and ever-changing market environment, this plan serves as a guiding indicator and is subject to uncertainties. It does not constitute a commitment to achieving the production targets. The company reserves the right to make corresponding adjustments to this plan based on changing circumstances. Investors are advised to pay attention to the risks.

Pacific Securities released a research report on April 17, recommending a "Buy" rating for Zijin Mining. The main reasons for the rating include: 1) The Akyem gold mine is one of the largest gold mines in Ghana and is currently operating stably; 2) With the continuous rise in gold prices, the project's resource and reserve potential for further exploration is promising; 3) The continuous increase in resources and reserves lays a solid foundation for long-term development. Risk warnings: Demand falls short of expectations; Supply exceeds expectations; The US Fed's tightening measures exceed expectations.

Kaiyuan Securities released a research report on April 15, recommending a "Buy" rating for Zijin Mining. The main reasons for the rating include: 1) Stable performance of the mineral products business, with an upward trend in the price center of copper and gold; 2) Implementation of a share repurchase plan to improve long-term incentive mechanisms. Risk warnings: Risk of fluctuations in raw material prices; Risk of policy changes; Risk of project progress falling short of expectations.

![This Week, Platinum and Palladium Experienced Significant Pullbacks, End-Use Demand Recovered, and Spot Market Trading Was Normal [SMM Platinum and Palladium Weekly Review]](https://imgqn.smm.cn/usercenter/obeMy20251217171735.jpg)

![Silver Prices Continue to Pull Back, Suppliers Remain Reluctant to Sell, Spot Market Premiums Hard to Decline [SMM Daily Review]](https://imgqn.smm.cn/usercenter/LVqfJ20251217171736.jpg)