SMM May 16 News:

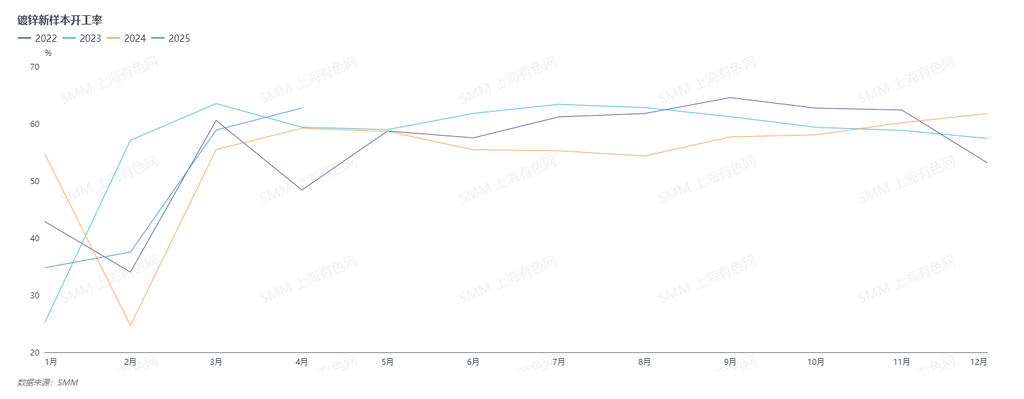

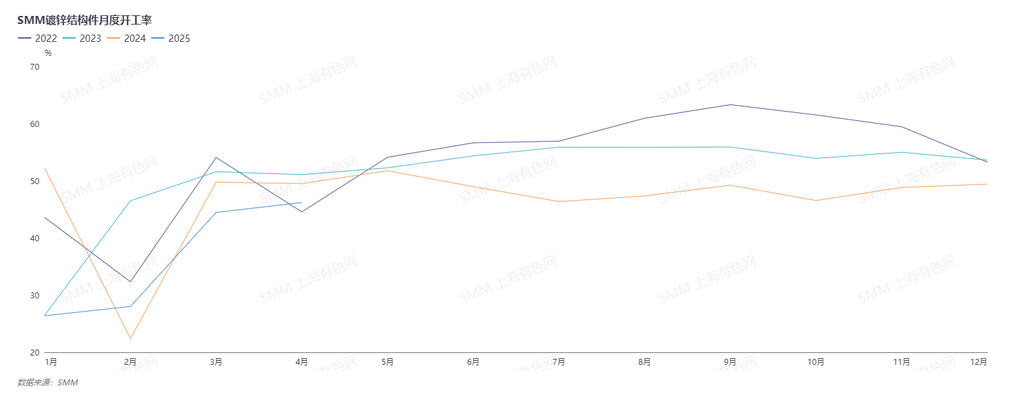

April, traditionally a peak season, saw robust overall demand for galvanizing. Due to issues such as tariffs, there was a certain degree of early release of future demand, and the overall operating rate was good. How did the north China, east China, and south China regions perform? Can the robust trend continue in May?

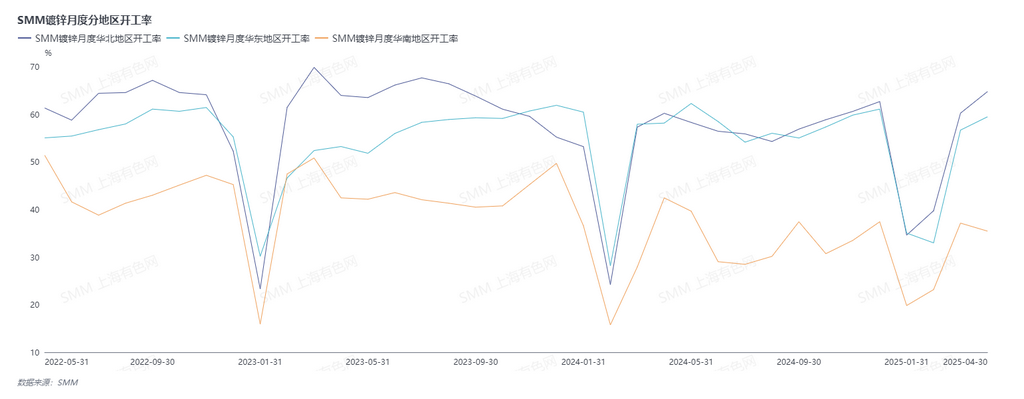

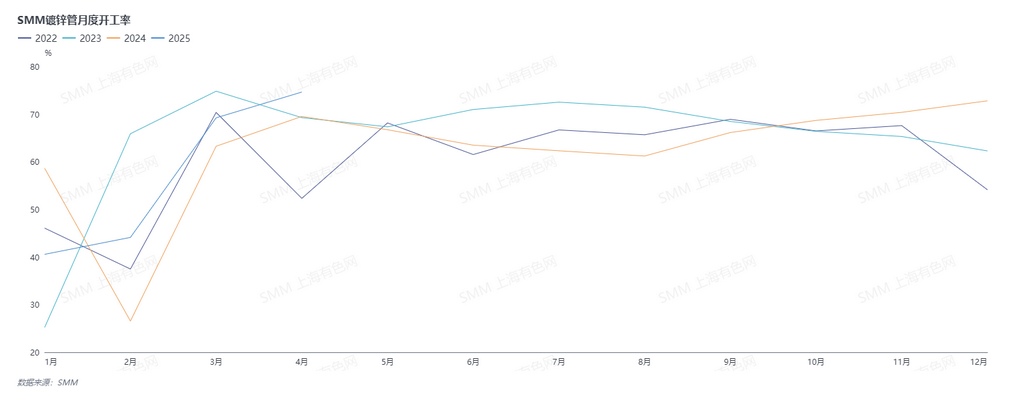

In April, the operating rate in north China continued to rise. Enterprises in north China mainly focus on galvanized pipes, with the operating rate for galvanized pipes also reaching a three-year high. The main reasons were the relatively stable ferrous metals prices in April, which showed a steady increase, and the phenomenon of traders rushing to buy amid continuous price rise and holding back amid price downturn. The overall sales volume of galvanized pipes was moderate, and many enterprises continued to operate with a low inventory turnover model, maintaining weekly days of inventories at only around 7-8 days. The order turnover was good, leading to an increase in enterprise operations. However, entering May, affected by macro factors, ferrous metals prices dropped back slightly, and there was still no significant improvement in real estate projects. Enterprises were concerned about subsequent demand, and orders for round pipes related to real estate pulled back. Moreover, the price war for galvanized pipes intensified, with a significant decline in enterprise profits, leading to a reduction in production schedules for enterprises in May.

In April, the operating rate in east China also increased. East China mainly focuses on galvanized structural parts, with new orders gradually being released for steel tower orders, and new tenders emerging continuously. Steel tower orders remained robust. Guardrail orders were also robust, while export orders pulled back due to the impact of tariffs. Entering May, with the mutual reduction of Sino-US tariffs, some enterprises expected an improvement in subsequent export orders. However, as May entered the traditional off-season, enterprises were not optimistic about subsequent demand, and production schedules were reduced.

In April, operations in south China decreased, with overall weak demand. Coupled with the fact that south China is not a major consumer area for galvanizing, the demand pullback was more pronounced, and operations were poor.

Looking ahead to May, although the mutual reduction of Sino-US tariffs has boosted market confidence, the arrival of the traditional off-season means that export orders will have limited impact on boosting overall demand. Enterprises are not optimistic about demand in May, and overall production schedules have been reduced.

(The above information is based on market collection and comprehensive evaluation by the SMM research team. The information provided in this article is for reference only. This article does not constitute direct advice for investment research decisions. Clients should make cautious decisions and should not use this as a replacement for independent judgment. Any decisions made by clients are unrelated to SMM.)