SMM, May 6:

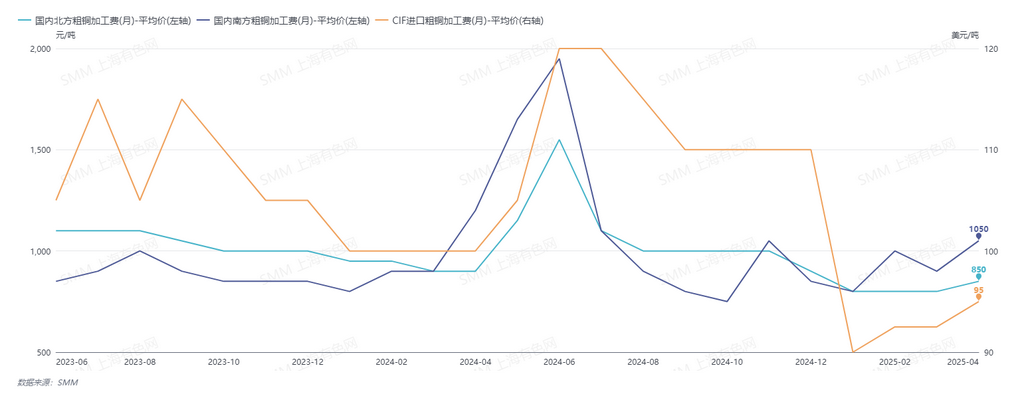

In April 2025, domestic blister copper RCs in south China were quoted at 950-1,150 yuan/mt, with an average of 1,050 yuan/mt, up 150 yuan/mt MoM. Domestic blister copper RCs in north China were quoted at 700-1,000 yuan/mt, with an average of 850 yuan/mt, up 50 yuan/mt MoM. CIF blister copper RCs were quoted at 90-100 US dollars/mt, with an average of 95 US dollars/mt, up 2.5 US dollars/mt MoM.

In April, following a sharp decline in copper prices after the Qingming Festival, suppliers of secondary copper raw materials chose to hold back cargoes. Meanwhile, a decrease in US copper scrap imports rapidly tightened the copper scrap market, prompting many copper anode producers using scrap to rely on consuming raw material inventories to fulfill long-term contract deliveries. However, as most upstream and downstream companies had already signed monthly RC agreements for April by the end of March, coupled with persistently high copper scrap prices during the month, producers had virtually no profit margins, resulting in almost no spot transactions in the market. Therefore, the RCs in April did not reflect the tight market conditions.

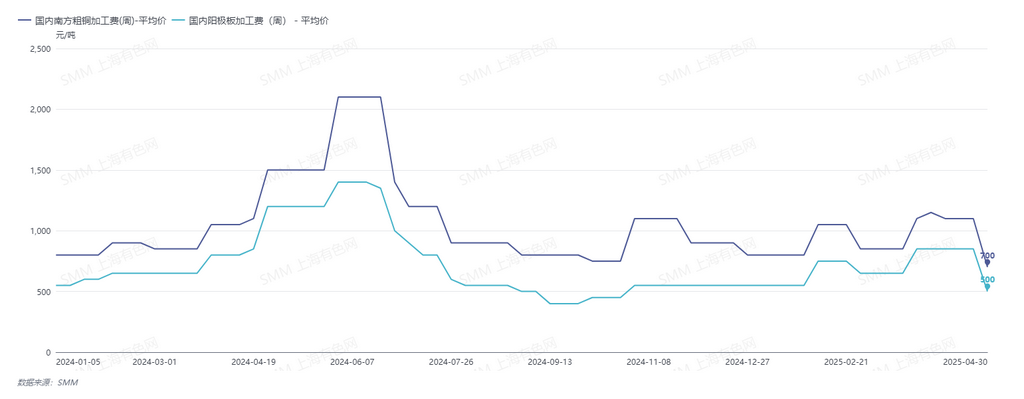

SMM's weekly domestic blister copper RCs in south China were quoted at 600-800 yuan/mt, with an average of 700 yuan/mt, down 400 yuan/mt WoW. Weekly domestic blister copper RCs in north China were quoted at 700-900 yuan/mt, with an average of 900 yuan/mt, unchanged WoW. Weekly CIF blister copper RCs were quoted at 90-100 US dollars/mt, with an average of 95 US dollars/mt, unchanged WoW. Domestic copper anode RCs were quoted at 450-550 yuan/mt, with an average of 500 yuan/mt, down 350 yuan/mt WoW.

After the market had shifted to a tightening pattern, blister copper and copper anode RCs plummeted in May. However, the future spot supply situation still depends on the trend of copper prices. If copper prices rebound further, the supply of secondary copper raw materials will continue to recover, and market production will increase accordingly. Conversely, if producers' profits remain unfavorable, the market will primarily rely on long-term contract supplies. Meanwhile, the volume of imported copper scrap may continue to decline. Additionally, two copper anode producers using ore are scheduled to undergo maintenance in May. However, imported copper anode shipments delayed in Q1 due to shipping delays will gradually arrive at ports, potentially providing some supplementary supply. From the demand side, some smelters will undergo maintenance in May, reducing their procurement of blister copper and copper anode as cold materials, while other smelters will resume normal demand after completing maintenance. Overall, if copper prices do not rise significantly, the market is expected to face a tight supply and demand situation in May.