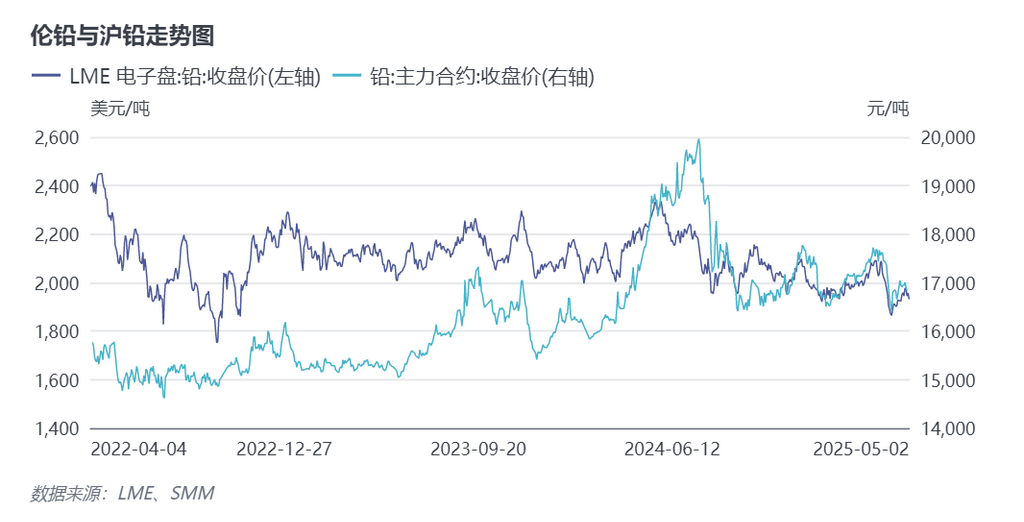

SMM, May 5: Due to the Labour Day holiday, the Shanghai Futures Exchange (SHFE) suspended night session trading from April 30. From May 1 to 5, which was the holiday period, SHFE lead trading was halted, and the domestic spot lead market also entered a trading suspension. The London Metal Exchange (LME) in overseas markets, however, continued trading as usual. During this period, non-ferrous metals generally declined on April 30 due to pressure from a strengthening US dollar. LME lead initially jumped and then pulled back throughout the day, reaching a high of $1,983/mt in the morning before giving up all its earlier gains in the afternoon. Over the next two days (May 1-2), LME lead gradually fluctuated downward, hitting a low of $1,930/mt. As of May 2, LME lead closed at $1,931.5/mt, down 1.3%.

During the Labour Day holiday, significant macro events and changes in economic data included:

(1) Regarding Sino-US tariffs, on May 2, Sino-US negotiations released positive signals, with the Chinese side stating that the US had repeatedly taken the initiative to convey information, expressing a desire to negotiate with China, and that China was currently assessing this. On May 3, the US officially implemented a 25% tariff on auto parts, but introduced two new tariff exemptions for auto parts and officially canceled the "low-value package tariff exemption" for China.

(2) Regarding expectations for US Fed interest rate cuts, according to the latest data, the US Q1 GDP turned negative on a QoQ basis, while April non-farm payrolls data came in better than expected, leading to a downward revision in expectations for US Fed interest rate cuts. The GDP and non-farm payrolls data indicate that the current resilience of the US economy and employment remains strong, with no signs of a recession. As a result, market expectations for the number of US Fed interest rate cuts this year have been revised down from four to three, and the timing of the first rate cut has been postponed from June to July.

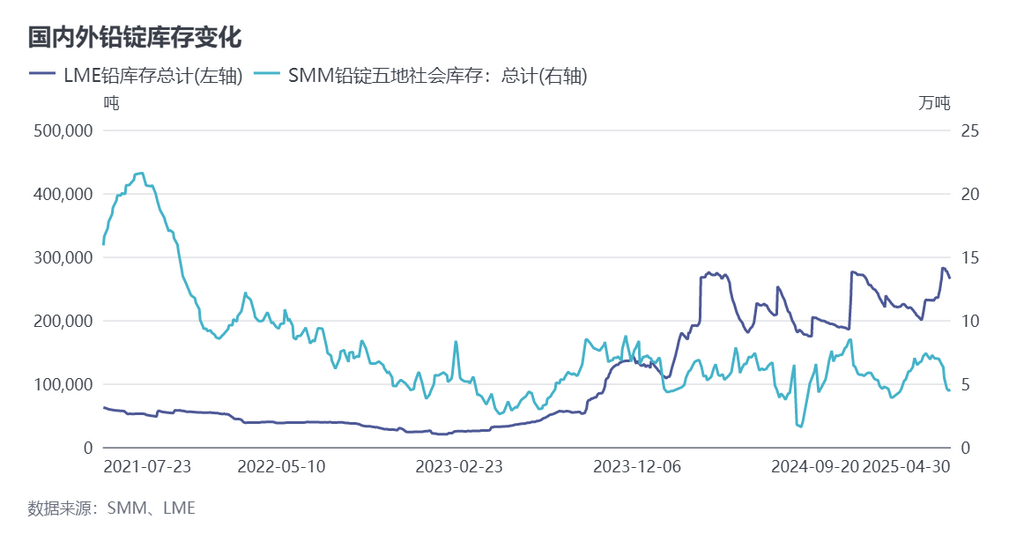

In terms of inventory changes in lead ingots, the trends in domestic and overseas lead ingot inventories diverged. During the Labour Day holiday, overseas lead ingot inventories continued their downward trend. As of May 2, total LME lead inventories stood at 264,125 mt, a decrease of 1,475 mt from before the holiday. Domestic lead ingot inventories had already shown a buildup trend on the eve of the Labour Day holiday. As of April 3, SHFE lead ingot weekly inventories were 46,786 mt, an increase of 1,132 mt from the previous week.

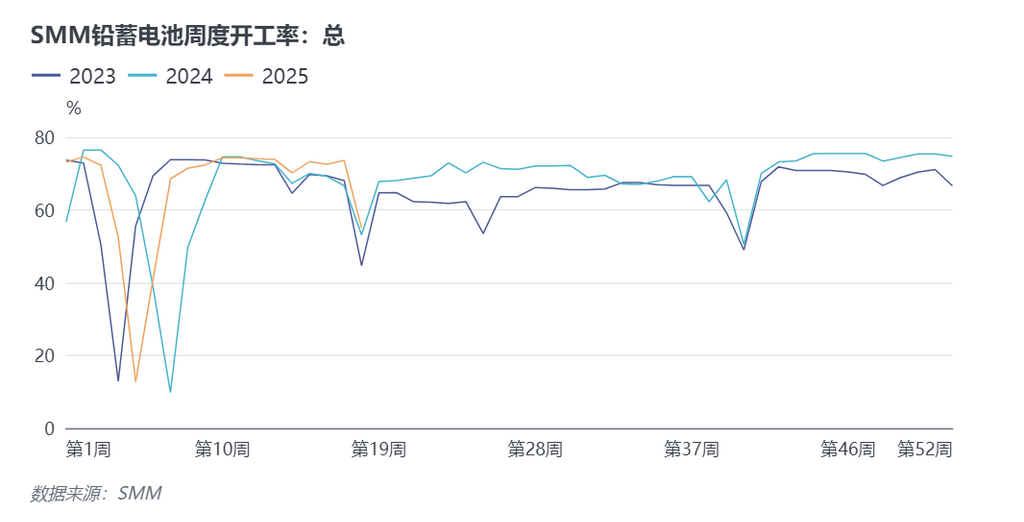

Forecast for post-holiday market changes: During the Labour Day holiday, upstream and downstream enterprises in China's lead industry chain had different holiday schedules, particularly downstream lead-acid battery enterprises, many of which took holidays ranging from 1-3 days to 4-7 days. This temporary absence of lead consumption has significantly increased the pressure on post-holiday lead ingot inventory buildup, potentially dragging down lead prices. As of May 2, the weekly operating rate of SMM lead-acid battery enterprises plummeted by 18.5 percentage points to 55.06%.

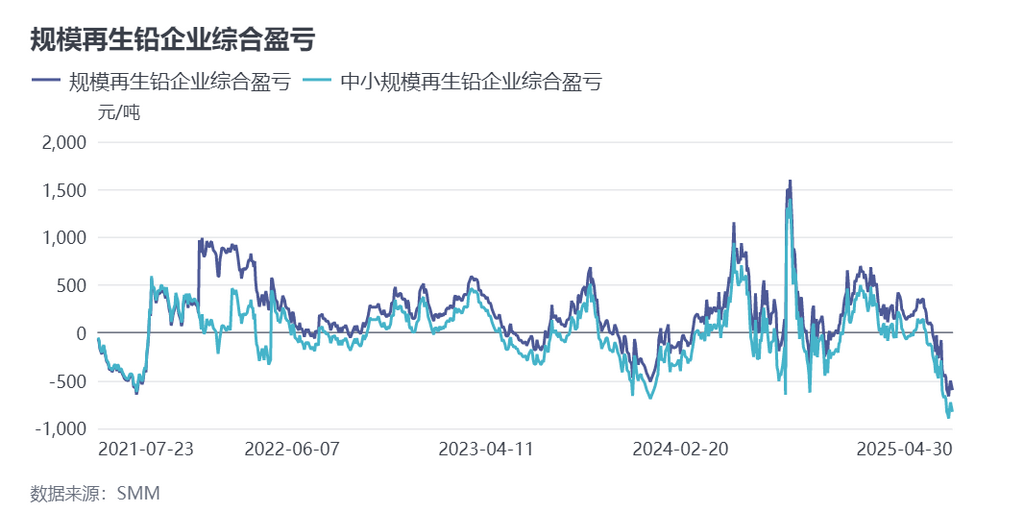

In terms of supply, production at primary lead smelters remained relatively stable, with some smelters resuming operations after maintenance, leading to a slight 1.2 percentage point increase in the weekly operating rate. This not only added pressure to lead ingot inventory buildup during the Labour Day holiday but also contributed to an increase in overall supply in May. In contrast, the number of secondary lead smelters cutting or halting production increased. According to SMM, the lead-acid battery market was in its traditional consumption off-season from April to May, which was a major factor dragging down lead consumption and also led to a reduction in scrap battery scrap volumes. The supply of scrap batteries in the pre-holiday market was tight, with secondary lead enterprises maintaining low raw material inventory levels. Due to supply-demand mismatches, scrap battery prices were more likely to rise than fall, causing secondary lead enterprises to generally operate at a loss. According to SMM, secondary lead enterprises incurred losses as high as 500-600 yuan/mt, leading to a decline in production enthusiasm among smelters and a series of production cuts or halts before the holiday. If the losses of secondary lead enterprises cannot be improved after the Labour Day holiday, it is not ruled out that the scope of production cuts by secondary lead enterprises will further expand, potentially becoming one of the conditions for balancing the consumption gap.

Overall, the risk of post-holiday lead ingot inventory buildup will lead to a weakening trend in lead prices. However, factors such as tight supply of raw materials like scrap and losses in secondary lead production will provide support. Before the lead ingot import window opens, these factors will become one of the main drivers for lead prices to rebound after hitting a low.

As the Labour Day holiday draws to a close and the UK bank holiday ends, both the SHFE and LME will resume normal trading from tomorrow (May 6). We need to focus on the lead ingot inventory buildup during the holiday and the production trends of smelters after the holiday.