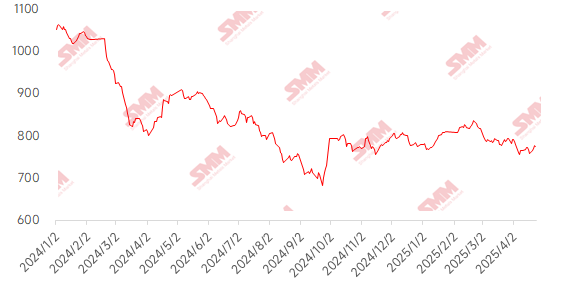

Iron ore prices continued to rise slightly this week. The fundamentals of iron ore remained strong. Overseas shipments declined slightly, while port arrivals dropped significantly by 5%, remaining at low levels. Daily pig iron production increased by 16,700 mt WoW. With the approaching Labour Day holiday, some steel mills began pre-holiday restocking, leading to robust iron ore demand and an increase in port pick-up volume. Additionally, mid-week, US President Trump publicly stated that current tariffs on China were too high and expected a significant reduction, easing tensions and boosting market sentiment, which caused a sharp rise in iron ore futures that day. In the spot market, the price of PB fines at Shandong ports rose by 5 yuan/mt WoW.

Chart: SMM 62% Imported Ore MMi Index

Data Source: SMM

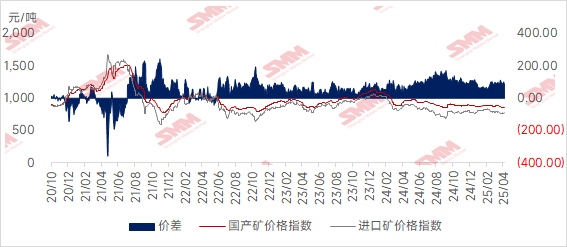

Domestic ore prices edged up this week, and are expected to continue to rise next week. Prices in Tangshan, Qian'an, and Qianxi in Hebei increased by 1-5 yuan/mt, while prices in west Liaoning, Chaoyang, Beipiao, and Jianping rose by 1-5 yuan/mt. Prices in east China increased by 10-15 yuan/mt.

Iron ore concentrate prices in the Tangshan region remained relatively stable, with 66% grade dry basis tax-included delivery-to-factory prices at 940-950 yuan/mt. Local mines and beneficiation plants stood firm on quotes due to high spot costs. Limited resources from low-titanium ore in east Liaoning, low-grade high-titanium ore in west Liaoning, Chengde, and Qinglong flowing into Tangshan also supported prices. With the approaching Labour Day holiday, steel mills are expected to restock, which may drive local market demand in the short term.

Domestic ore prices in west Liaoning remained steady, with 66% grade wet basis tax-excluded ex-factory prices at 700-710 yuan/mt. Raw ore resources are scarce locally, and beneficiation plants face high production costs. Producers, considering their profits, maintained a strong sentiment to stand firm on quotes. Additionally, large mines have limited supplies, mostly delivered directly to steel mills, resulting in tight spot resources in the market. In-production beneficiation plants have low inventory and are in no rush to sell, supporting their quotes.

In east China, mines and beneficiation plants mostly operated as planned, producing and selling without inventory pressure. Previously suspended mines gradually resumed normal production, slightly easing the tight supply of iron ore concentrates in the short term.

Looking ahead to next week:

For imported ore: The iron ore market is expected to maintain a fluctuating upward trend, supported by the following factors: 1) resilient demand, with daily pig iron production remaining high; 2) pre-Labour Day restocking demand from steel mills, further boosting ore consumption; and 3) rising market expectations for macro policies from the upcoming Politburo meeting. However, uncertainties in US-China tariff policies and marginally weakening end-use demand will limit the upside room for prices. Iron ore prices are expected to continue rising next week, but the increase will be limited.

For domestic ore: Overall, the tight supply of domestic iron ore concentrates continues to support prices. With the approaching Labour Day holiday, steel mills have restocking needs, and high pig iron production from blast furnaces will sustain market enthusiasm. Domestic iron ore prices are expected to have some upward room next week.

Click to view the SMM Metal Industry Chain Database

![Before the holiday, the black chain is unlikely to see a trend-driven market [SMM Steel Industry Chain Weekly Report].](https://imgqn.smm.cn/usercenter/zUFfM20251217171748.jpg)

![[SMM Chromium Daily Review] Inquiries and Transactions Weakened, Chromium Market Showed Mediocre Performance Before the Holiday](https://imgqn.smm.cn/usercenter/ENDOs20251217171718.jpg)